Find the help you need for any problem

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

Types of Personal Loans: A Complete Guide to Options and Use Cases

You know that feeling when you need money for something real — a wedding, a surprise repair, digging out of credit card debt — but loan talk makes your eyes glaze over. A personal loan is simple: a lump sum, repaid in fixed chunks over a few years. The confusion starts with the word “types.” It can mean three different things: whether you put up collateral, what the money is for, or the kind of borrower you are (credit, income, your financial fingerprint). Most loans check boxes in all three categories at once. This guide cuts through the labels, walks you through the real differences, and helps you land on the loan that won’t leave you wondering what you signed up for.

In this article:

- How personal loans are categorized

- Secured vs unsecured personal loans

- Common types of personal loans by use case

- Personal loans by borrower type

- Personal loans by structure and features

- Less common personal loan types

- How to choose the right type of personal loan

- Risks and considerations across loan types

- Where Pennie Financial fits

- Final takeaway

- Frequently Asked Questions

How personal loans are categorized

Think of any personal loan as sitting at the intersection of three different sorting systems. The first drawer sorts by structure: does the lender require a safety net (secured) or take you at your word (unsecured)?

The second drawer sorts by purpose. Lenders commonly recognize debt consolidation, medical bills, home repairs, and major purchases as the main categories, though many loans aren’t picky about how you spend the money.

The third drawer sorts by who’s borrowing — your credit score range, income type, and how thick your file is. That’s where you’ll find labels like “bad credit loans” or “income‑based loans.”\

Here’s the short version: every loan lives in all three drawers at once. Figure out where a loan falls on each scale, and you’ll stop confusing products that are really the same animal dressed up in different marketing clothes.

Secured vs unsecured personal loans

Picture two doors. Behind the first, you hand the lender the keys to something you own — a savings account, a car, anything valuable. That’s a secured loan. If you stop paying, they take your keys and walk away with your stuff. Behind the second door, you offer nothing but your name and your credit history.

That’s unsecured. They lend you money on a handshake and a prayer, trusting you’ll keep your word.

The risk flips completely depending on which door you pick. With a secured loan, your downside isn’t a ding on your credit — it’s losing whatever you put up. Miss payments, and that savings account gets emptied. That car gets hauled away. An unsecured loan won’t cost you property, but it will wreck your credit score and send collectors knocking. The lender’s risk is higher, so they charge for it. For a deeper look at how unsecured lending works, check out our guide on unsecured personal loans, rates, requirements, and risks.

Who should walk through which door? If your credit is solid and you’d rather not gamble your possessions, unsecured is your default move. If your score is patchy or you’re after the lowest possible rate, secured makes sense — provided you’re comfortable putting something on the line. The trade‑off is always the same: a cheaper rate in exchange for sleeping with one eye open. If you want a full side-by-side breakdown, read our article on secured vs unsecured personal loans and which is better.

Common types of personal loans by use case

Lenders often label loans by what you plan to do with the money. The structure underneath is usually the same, but the name gives you a hint about which lender to talk to and what terms to expect.

Debt consolidation loans

Roll several high‑interest debts into one fixed monthly payment. The appeal: trade a pile of due dates and double‑digit APRs for a single, lower‑rate loan that actually ends. Someone with three credit cards at 22% APR wraps $15,000 into a three‑year personal loan at 12%, saving thousands in interest if they stick to the schedule. For a broader look at your options, check out our guide on the best ways to consolidate credit card debt.

Not sure whether debt consolidation or a standard personal loan is the right move? Read our article on debt consolidation vs personal loans.

Medical loans

Cover out‑of‑pocket health costs — surgery, dental work, fertility treatment — without letting a hospital bill rot on a high‑interest credit card. Facing $8,000 in unexpected dental work, a borrower takes a 48‑month loan to spread the cost rather than paying 25% APR on a credit card.

Home improvement loans

Finance a new roof, HVAC system, or kitchen upgrade without tying the debt to your house. Slower than swiping a card, but cheaper than carrying a balance for months. A homeowner needs $20,000 for an emergency furnace replacement before winter. A personal loan closes in a week, while a HELOC would take longer and require an appraisal.

Emergency loans

Fast cash for surprises that can’t wait — a blown transmission, a sudden trip, an urgent bill. The product is a standard personal loan, just funded at warp speed. A transmission repair quote lands at $3,500 on a Friday afternoon; a same‑day online loan puts money in the borrower’s account before the mechanic releases the car.

Major purchase loans

One big expense, paid in predictable chunks. Weddings, moving costs, adoption fees, that piece of equipment you need for a new gig. A couple takes a 36‑month loan to cover wedding costs, paying it down as they save instead of drowning in credit card interest.

Personal loans by borrower type

The other way lenders segment is by who the borrower is. This is where loans are often marketed by credit tier or income situation.

Here’s how the different borrower segments stack up in terms of rate:

- Bad credit loans target borrowers with credit scores below roughly 580. Approval criteria emphasize income stability and existing debt load rather than score. Rates are typically higher to compensate for elevated default risk. For everything you need to know before applying, read our full guide on bad credit loans.

- Fair credit loans target the 580 to 669 band. Approval is more accessible than prime products, rates land in the middle of the market, and terms are typically shorter. If that sounds like your situation, check out our guide on the best personal loans for fair credit.

- Income-based loans weigh current cash flow heavily relative to credit score. These are particularly relevant for borrowers with thin credit files but strong, stable income. For a full breakdown of how these work, read our guide on income-based loans.

- Loans for limited credit history are designed for borrowers who haven’t used credit before or whose files have too few accounts to score reliably. Some lenders will look at rent payment history, utility payments, or bank account flow to assess reliability.

Compared side by side, the rate ladder usually looks like this: loans for prime credit borrowers price lowest, fair credit next, income-based and limited-file products higher, and bad-credit products highest. The difference between the top and bottom of this range is often double-digit percentage points in APR — which means the cost of waiting a few months to improve a credit profile can be substantial.

Personal loans by structure and features

Beyond secured vs unsecured, loans also vary by how the interest rate and repayment work. Here are the main structures you’ll encounter:

- Fixed-rate loans lock in a single APR for the life of the loan. The monthly payment doesn't change. Most personal loans in the U.S. market are fixed-rate, which makes them predictable for budgeting.

- Variable-rate loans have an APR that moves with a reference rate. Payments can rise or fall over time. Variable-rate structures are less common in standard personal loans and more common in lines of credit. They can start lower than fixed-rate offers but carry rate-risk for the borrower.

- Installment loans — the default structure for a personal loan — disburse a single lump sum, then you repay in equal monthly installments until the balance is zero. Each payment covers interest plus a portion of the principal, and the loan ends on a known date. Predictability is the main appeal.

Less common personal loan types

Co‑signed loans bring in a second person who agrees to pay if you won’t. The co‑signer’s credit gets checked right alongside yours. That can open doors you couldn’t open alone and bring down the rate, but it puts someone else’s credit on the line for your choices.

Joint loans give both borrowers equal access to the money and equal responsibility from the first day. Both names go on the application, both can draw funds, both get reported to the bureaus.

A personal line of credit works more like a credit card than a loan. You get a limit, you draw what you need, you repay, and you draw again. Interest runs only on what you actually use. Great for projects with uncertain totals or income that comes in chunks. Lousy for a fixed‑cost purchase where you just want a set payment and an end date.

How to choose the right type of personal loan

The best loan type for you depends on what you need the money for, what your credit looks like, and how you plan to repay. A quick breakdown based on your situation:

- Fixed amount or ongoing need? Installment loan or line of credit.

- Strong credit history? Unsecured, fixed‑rate.

- Thin credit but steady income? Income‑based or secured.

- Consolidating debt? Debt consolidation loan.

- Pledge an asset? Only if you’re comfortable risking it.

Risks and considerations across loan types

A lower monthly payment often means a longer term, which can add years of interest. The cheapest loan on paper isn’t always the cheapest over time. Always look at total interest. If you’re considering consolidation specifically, take a look at our article on whether debt consolidation is actually a good idea.

The fastest yes usually comes with the highest rate. Loans for bad credit approve quickly but cost significantly more than prime products. The right loan is the hardest one you can realistically qualify for.

Every new loan adds an account to your credit file and affects your debt‑to‑income ratio for years. Secured loans put your property at risk. Co‑signed loans tie someone else’s credit to your behavior. Choosing the wrong loan type can significantly increase total borrowing cost.

Where Pennie Financial Fits

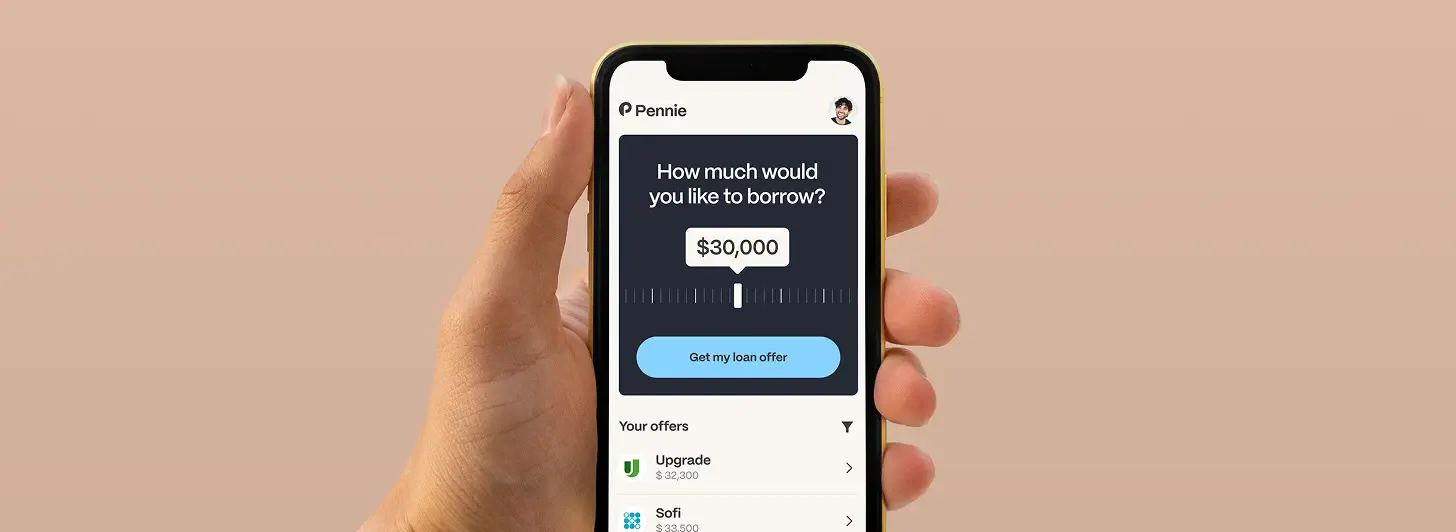

Pennie Financial connects borrowers with lending partners across the categories described above — secured and unsecured products, use-case-specific lenders, and partners that serve different financial situations. The platform surfaces multiple options based on your profile, so comparing structures and rates across a few lenders is one step instead of several separate applications. Browse personal loan options and see what fits your situation. If you want to understand the process before you start, take a look at how Pennie works — it walks through each stage from application to funding.

Final takeaway

There isn’t a single best type of personal loan. There’s a best type for the situation: a specific amount, a specific use, a specific credit profile, and a specific repayment plan. The borrower who benefits most from a debt consolidation product often wouldn't benefit from a line of credit, and vice versa.

Understanding the categories makes it easier to cut through marketing language and pick the structure that actually fits what you're trying to do. The goal isn’t to choose the cheapest loan on paper — it’s to match loan type to purpose so that the total cost and the monthly friction both stay manageable.

Frequently Asked Questions

What are the main types of personal loans?

The most common way to group them is by structure (secured vs unsecured), by purpose (debt consolidation, medical, home improvement, emergency, major purchase), and by borrower profile (prime, fair, bad credit, income-based, limited history).

What is the difference between secured and unsecured loans?

A secured loan is backed by collateral the lender can take if you default — usually savings, a CD, or a vehicle. An unsecured loan is backed only by your credit and promise to repay.

What type of personal loan is easiest to get?

Secured loans and bad-credit-focused loans are generally the easiest to qualify for. Both compensate for lender risk — secured loans through collateral, bad-credit loans through a higher rate.

Which personal loan type has the lowest interest rates?

Unsecured loans for prime-credit borrowers typically carry the lowest rates. Secured loans backed by cash (a CD or savings account) also price very competitively, since the lender’s risk is minimal.

Are there personal loans for bad credit?

Yes, though rates may be higher and loan amounts are often smaller depending on the situation. Some lenders specialize in borrowers with scores below 580 and emphasize income stability in underwriting.

What type of loan is best for debt consolidation?

Most borrowers consolidating credit card balances use a fixed-rate unsecured personal loan with a term chosen to match their ability to pay it off.

Can you use any personal loan for any purpose?

Most personal loans can be used for any legal purpose, but many lenders ask you to state a purpose on the application and some restrict certain uses.

Get loan offers in as little as 60 seconds

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years