Find the help you need for any problem

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

Debt Consolidation vs Personal Loan: Key Differences and How to Choose

Life is practical, and money is part of that reality. That's where financial tools like personal loans — and strategies such as debt consolidation — come into play. The two terms clearly sound different and mean different things. While many people have at least a rough idea of what a personal loan is, far fewer could explain what debt consolidation actually means. Since money is a part of life, it makes sense to know what these terms mean and how they differ.

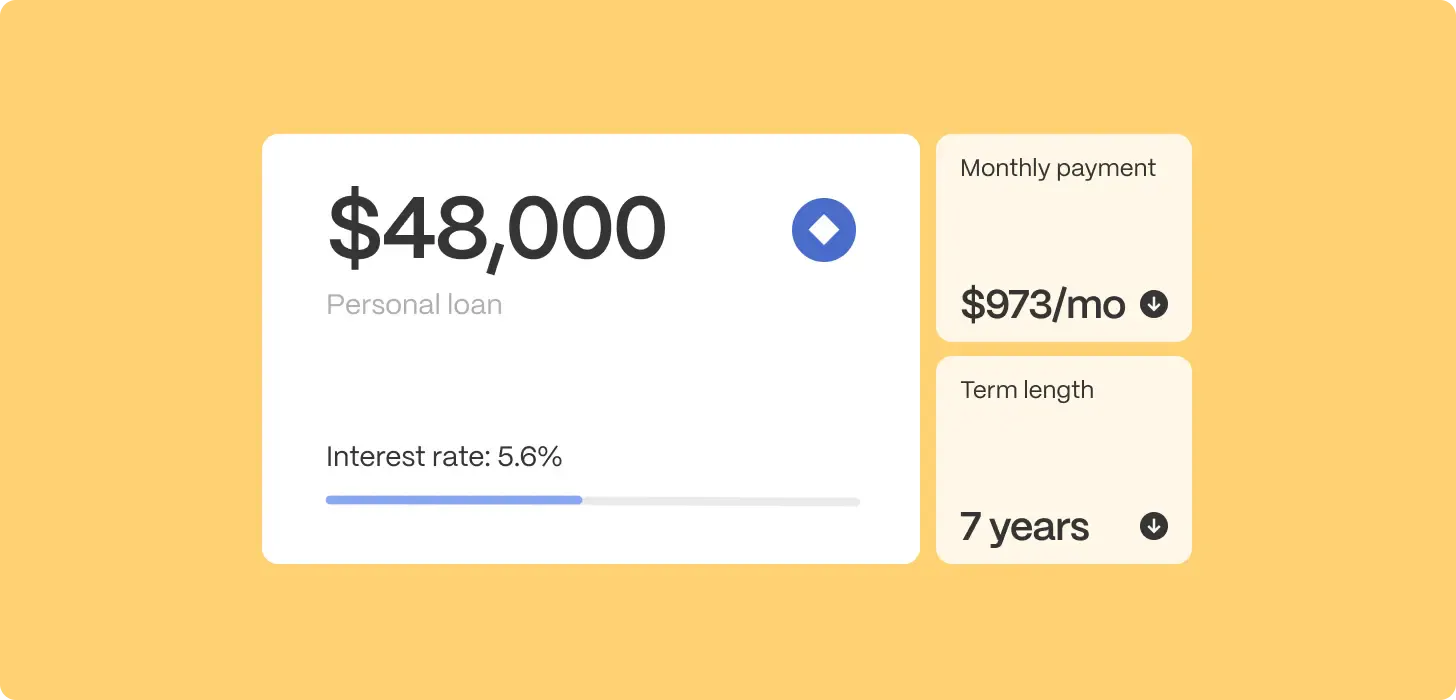

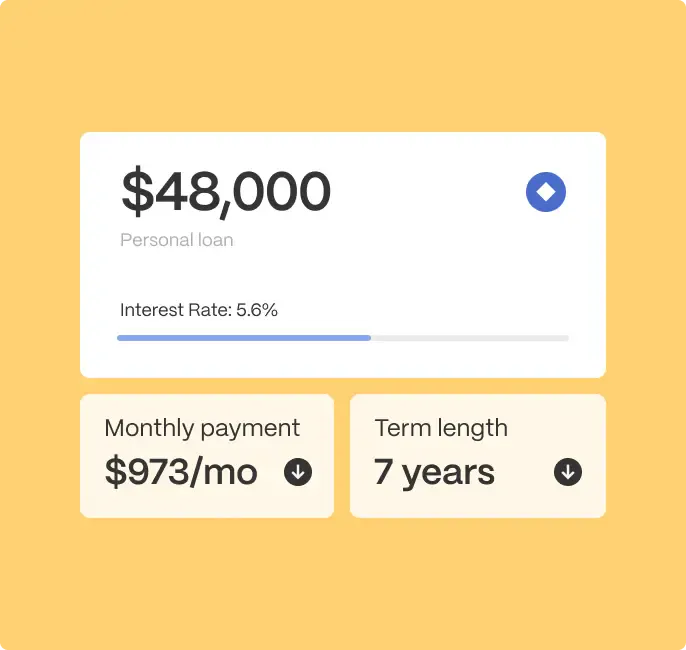

A personal loan is a lump sum you borrow from a lender and repay in fixed monthly installments, usually over two to seven years. Debt consolidation involves rolling multiple debts into a single payment. Personal loans are the most common way to consolidate debt. Consolidation itself isn't a type of loan — it's a reason for borrowing.

Since there's a difference, understanding matters. Whether you need a general-purpose loan or a targeted way to manage existing debt affects which products are appropriate, which terms to watch for, and how to evaluate your options. This guide walks through both options so you can figure out which one actually fits your situation.

What Is a Personal Loan?

A personal loan is a fixed-amount loan from a bank, credit union, or online lender. Most are unsecured, which means you don't need to put up your car or house as collateral. Approval is based on your credit history, income, and how much debt you're already carrying. Some lenders do offer secured versions with lower rates, but those are the exception.

The structure is straightforward. You borrow a set amount, get a fixed interest rate (variable rates exist but are uncommon), and repay it in equal monthly installments over a defined term. The payment stays the same each month.

Where personal loans stand apart from something like an auto loan or a mortgage is flexibility. There's no restriction tying the funds to a specific purchase. People use them for home renovations, medical procedures, moving costs, weddings — and yes, paying off other debts. That general-purpose nature is exactly what makes a personal loan a product category rather than a single-use financial tool.

As mentioned earlier, lenders consider a variety of elements when deciding whether to approve a loan. But not all carry the same weight. Some lenders rely heavily on credit scores, while others emphasize income stability and employment history — which can open doors for borrowers whose credit file doesn't fully reflect their financial situation.

What Is a Debt Consolidation Loan?

A debt consolidation loan is a loan you take out specifically to pay off multiple existing debts — credit cards, medical bills, other loans — and replace them with a single monthly payment.

Structurally, it's almost always a personal loan. The mechanics and repayment format are the same. The difference is purely about intent: the funds go toward wiping out scattered balances, not funding something new.

The appeal is pretty intuitive. Say you're carrying $14,000 across three credit cards with rates between 22% and 27%. You're making three separate payments every month, tracking three due dates, and watching interest compound on all of them. A consolidation loan replaces that mess with one payment, one rate, one due date.

However, don't confuse simplification with major changes. Consolidation doesn't shrink your debt — you still owe the same amount. What changes is how the repayment is structured: potentially at a lower rate, definitely with less administrative hassle, and ideally with a clear payoff date you can plan for.

Beyond personal loans, consolidation can also happen through balance transfer credit cards or home equity products. Realistically, though, most people don't have enough equity or a strong enough credit profile to land a 0% balance transfer. For the majority of borrowers, a personal loan built for consolidation is the most practical route.

Key Differences Between Debt Consolidation and Personal Loans

It's time to organize all the information covered so far. A side-by-side breakdown works perfectly for this — and fortunately, one is already prepared:

| Factor | Personal Loan | Debt Consolidation Loan |

|---|---|---|

| Purpose | General-purpose borrowing for any qualifying expense | Specifically used to combine and repay existing debts |

| Typical Use | Home improvement, medical bills, major purchases, events | Paying off multiple credit cards, medical debt, or other loans |

| Loan Structure | Fixed amount, fixed or variable rate, set repayment term | Same structure — funds are just directed toward existing balances |

| Interest Rate | Varies by lender and borrower profile; fixed rates common | Often lower than current credit card rates; fixed rate is standard |

| Credit Impact | Hard inquiry at application; on-time payments build credit over time | Hard inquiry at application; may improve credit utilization once balances are paid off |

| Flexibility | High — use funds however you need to | Low — funds go toward paying off specific debts |

| Number of Payments | One monthly payment on the new loan | One monthly payment replacing multiple previous ones |

When Does a Personal Loan Make Sense?

A personal loan fits best when your borrowing need isn't primarily about paying off existing debt.

Covering a large planned expense. A renovation, a medical procedure, a cross-country move. A personal loan gives you the lump sum upfront with repayment terms you can budget around — which beats putting $12,000 on a credit card and watching 24% interest pile up for the next three years.

Short-term borrowing with a defined payoff plan. If you know you need capital now and can realistically pay it back within two to three years, a short-term personal loan keeps the math clean.

When you need the money for more than one thing. Maybe part of the funds cover a move and part go toward paying down a credit card. A standard personal loan doesn't care how you allocate it. That flexibility is the entire point.

When Does Debt Consolidation Make Sense?

If you're carrying balances on four or five credit cards at rates north of 20%, you're not comparison shopping out of curiosity. You need a structural solution. Consolidation is built for exactly that scenario.

Multiple high-interest debts eating into your monthly budget. Combining them into a single loan at a lower rate makes the entire repayment visible. For example, $10,000 spread across three credit cards at 22–26% interest could cost over $3,000 in interest over three years, while a consolidation loan at 12% might save more than $1,200 in total interest.

Too many due dates and minimum payments to track. Missed payments happen more often because of disorganization than inability to pay. One consolidation loan means one payment on one date. That alone reduces the risk of late fees and credit damage.

You want a real payoff date. Credit cards don't give you that. The minimum payment shifts, the balance barely moves, and the timeline stretches indefinitely. A consolidation loan with a fixed rate and a set term gives you a date on the calendar where you're done. For a lot of borrowers, that psychological clarity is just as valuable as the interest savings.

Pros and Cons of Each Option

There's no perfect solution, but some advantages outweigh the drawbacks. It's worth taking a closer look.

Personal Loan

What works in your favor: Flexibility is the headline. You can use the funds for almost anything, payments are predictable, rates are fixed in most cases, and you don't need to put up collateral. Funding is usually fast — a few business days in many cases.

What to watch for: Rates can run higher than secured options, particularly if your credit isn't strong. Origination fees are common and reduce your actual disbursement. And because nobody tells you how to spend the money, borrowers without a clear plan sometimes use it for things that don't move the needle financially

Debt Consolidation Loan

What works in your favor: Simplification is the core value. Fewer payments, less room for error, and potentially lower interest costs if the new rate undercuts what you're currently paying. There's also a credit benefit: paying off revolving balances can improve your credit utilization ratio, which is one of the more influential factors in your credit score.

What to watch for: Consolidation restructures your debt. If the new loan stretches the repayment term out further, you might pay more in total interest even at a lower rate. And here's the trap that catches more people than you'd expect: once those credit cards are paid off, the temptation to use them again is real. Running up new balances on cards you just zeroed out puts you in a worse position than where you started.

When Consolidation is a Bad Idea

Debt consolidation can simplify payments, but it's not always the right choice.

Consider avoiding it if:

You don't have discipline with spending. Paying off credit cards with a new loan only to rack up balances again can make things worse. This can lead to more debt than before. In the long run, it defeats the purpose of consolidation.

The new loan has high fees or a longer term. Sometimes extending the repayment period or paying origination fees can increase total interest compared to your current debts. Even if the monthly payment looks lower, you might pay far more overall.

Your debt is already manageable. You can comfortably pay off your credit card balances each month without stress or missed payments. In this case, consolidation might not offer meaningful savings.

Debt Consolidation vs Personal Loan – How to Decide

Making a choice becomes easier when you have clear criteria. When deciding between a debt consolidation loan and a personal loan, it comes down to four things.

Your credit profile. Better credit gets you better rates. That makes consolidation more cost-effective for borrowers with strong scores. But it's not the only path — some lenders evaluate income and employment stability alongside credit history, which can surface options that a score alone wouldn't unlock.

Your income stability. A fixed monthly payment only works if you can actually make it every month. Before committing, run the numbers against your real budget. Lenders that look at your full financial picture rather than just a three-digit score can sometimes structure terms that better reflect what you can genuinely afford.

Your debt structure. This one is usually the clearest signal. Debt scattered across many accounts at different rates? Consolidation. A single borrowing need that has nothing to do with existing debt? Personal loan. It's rarely more complicated than that.

What you're actually trying to accomplish. Simplify payments and reduce interest on existing debt? Consolidation is purpose-built for that. Need capital for something new? A personal loan gives you room to move.

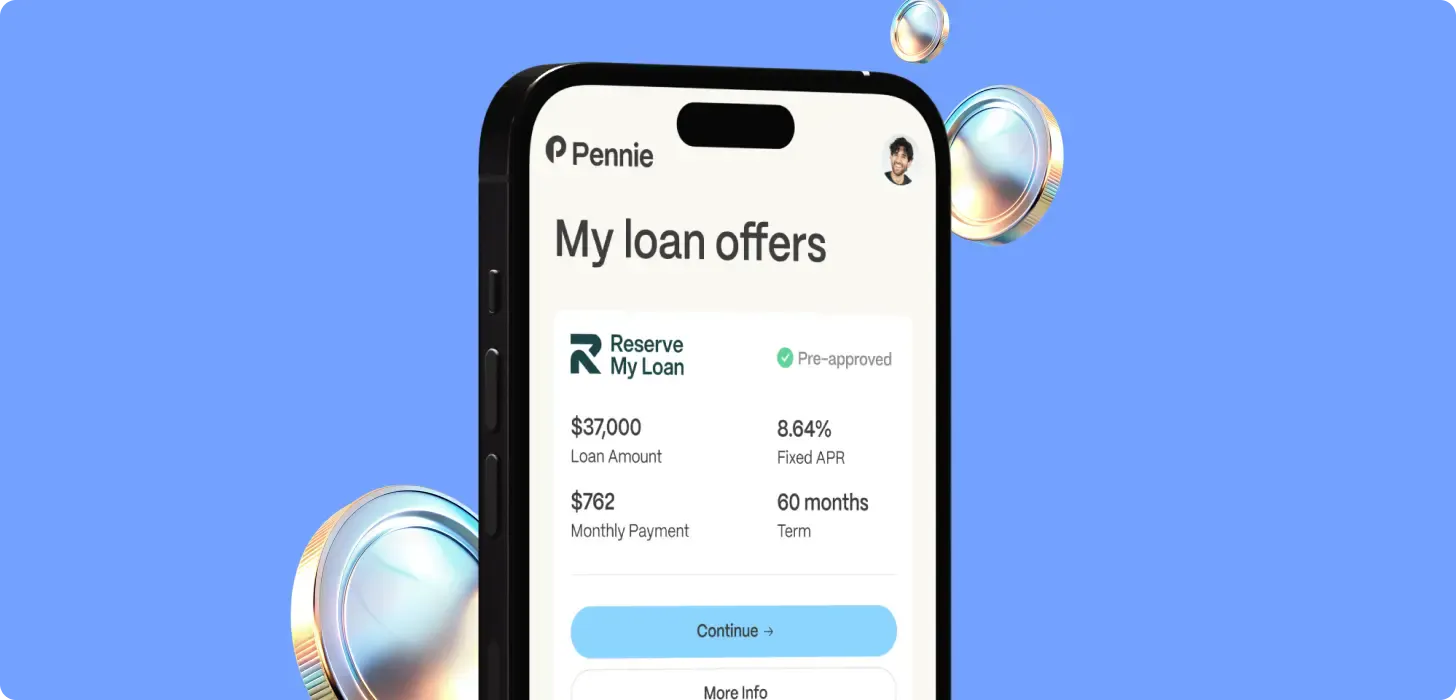

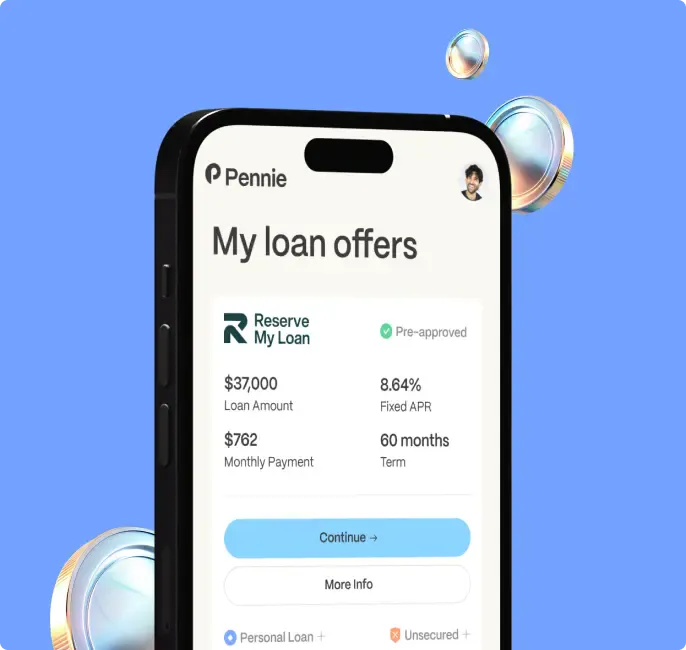

Whichever direction you lean, comparing offers across multiple lenders is non-negotiable. Rates, terms, fees, and qualification standards vary more than most expect. Platforms, such as Pennie Financial, may evaluate borrowers differently, so checking your options across multiple services can give a clearer picture — without locking you into a commitment.

Frequently Asked Questions

Is debt consolidation the same as a personal loan?

No, but they're closely related. A personal loan is a financial product — a lump sum you borrow and repay in installments. Debt consolidation is a strategy for combining multiple debts into one.

Can I use a personal loan for debt consolidation?

Absolutely — it's one of the most common reasons people take out a personal loan in the first place. You receive the funds, pay off your existing balances, and then make a single monthly payment on the new loan going forward.

Is a personal loan good for debt consolidation?

It can be a strong fit, especially if you qualify for a rate that's meaningfully lower than your current debts. You get a fixed payment, a clear payoff date, and simplified repayment.

Which is better: a personal loan or debt consolidation?

Neither is categorically better. They solve different problems. If you're buried under multiple high-interest balances and need to get organized, consolidation is the direct answer. If you need funds for a purpose that isn't about existing debt, a personal loan gives you that flexibility.

Get loan offers in as little as 60 seconds

You deserve options. So we built an industry leading platform to compete for your business.

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years

Your info is never sold