Find the help you need for any problem

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

Unsecured Personal Loans Explained: Rates, Requirements, and Risks

Unsecured personal loans don’t ask for collateral. No home equity, no car title, no savings account on the line. Lenders look at your credit score, your income, and your debt history. That’s what decides if they approve you. Because there’s nothing backing the loan, approval can be faster than with secured loans. And more people can actually get approved — even if you don’t own a house.

But here’s the real deal. Lenders aren’t all the same. One might like a steady paycheck even if credit is rough. Another might care more about existing credit card debt. So instead of offering a one-size-fits-all answer, this breakdown shows how to figure out what you qualify for, what rates really look like, and when walking away is the smarter move.

In this article:

- What is an unsecured personal loan?

- How unsecured personal loans work

- What can unsecured personal loans be used for?

- Unsecured personal loan rates

- Requirements for unsecured personal loans

- Pros and cons

- Unsecured vs secured loans

- Risks of unsecured personal loans

- When an unsecured personal loan may make sense

- When other options may be worth considering

- Where Pennie Financial fits

- Final thoughts

- Frequently Asked Questions

What is an Unsecured Personal Loan?

In simple terms, it’s a loan where nothing you own is on the line. If you default, the lender’s only recourse is legal action. They have to sue to recover their money rather than seizing your property.

Common examples of unsecured personal loans include:

- Debt consolidation loans used to pay off credit cards

- Emergency loans for medical bills or home repairs

- Loans to cover large purchases like appliances or electronics

- Wedding, vacation, or relocation financing

- Business startup funds for self-employed borrowers

With a secured loan like a mortgage or auto loan, the asset itself backs the debt. Miss enough payments and the lender repossesses the car or forecloses on the home. That security lets them offer lower rates and more flexible terms. With an unsecured loan, the lender takes on more risk, and that risk gets priced into your interest rate. That’s why these loans tend to cost more than secured alternatives, but also why they move faster and don't require anything to be put up front.

How Unsecured Personal Loans Work

The mechanics are simpler than most people expect. From application to funding, the process typically includes these steps:

1. Application

You fill out an application with basic information: income, employment, existing debts, and the amount you want to borrow.

2. Credit check

The lender pulls your credit report. Some lenders use a soft pull (no impact on your score) for a quick pre-qualification, while others perform a hard pull during formal underwriting.

3. Lender evaluation

The lender reviews your credit score, income, debt-to-income ratio, and payment history to assess risk.

4. Approval or conditional offer

You receive a decision—approved, approved with conditions, or denied. Conditional approvals might require documentation like recent pay stubs.

5. Funding

Once fully approved, the lender transfers the money to your bank account. If you’re wondering what affects that timeline, our guide to how long it takes to get a personal loan walks through the key variables.

What Can Unsecured Personal Loans Be Used For?

Unsecured personal loans are flexible. Once approved, you can use the money for almost any purpose:

- Debt consolidation. Combine multiple credit cards or high-interest debts into a single loan with one predictable monthly payment. Simpler to manage and often cheaper.

- Medical expenses. Cover unexpected health costs that insurance doesn’t fully pick up. A practical alternative to draining savings or letting unpaid bills go to collections.

- Emergency repairs. A broken appliance, roof damage, or car malfunction can’t always wait. A personal loan gets money in your account quickly enough to handle it.

- Large purchases. Buy furniture, electronics, or other big-ticket items on a fixed repayment schedule instead of putting them on a high-interest credit card.

- Education. Pay for training programs or certifications when student loans aren’t available or don’t cover the full cost of what you need.

- Life events. Finance a wedding, relocation, or vacation with a structured loan rather than charging everything to a card and managing the interest later.

- Business startup. Self-employed borrowers can use a personal loan as seed funding when business credit history isn’t yet established.

That said, there are a few things most lenders won’t cover. Illegal activities are off the table, and some lenders won't fund a down payment on a car or home purchase. If you’re unsure which product fits your needs, our overview of personal loan types can help you narrow it down.

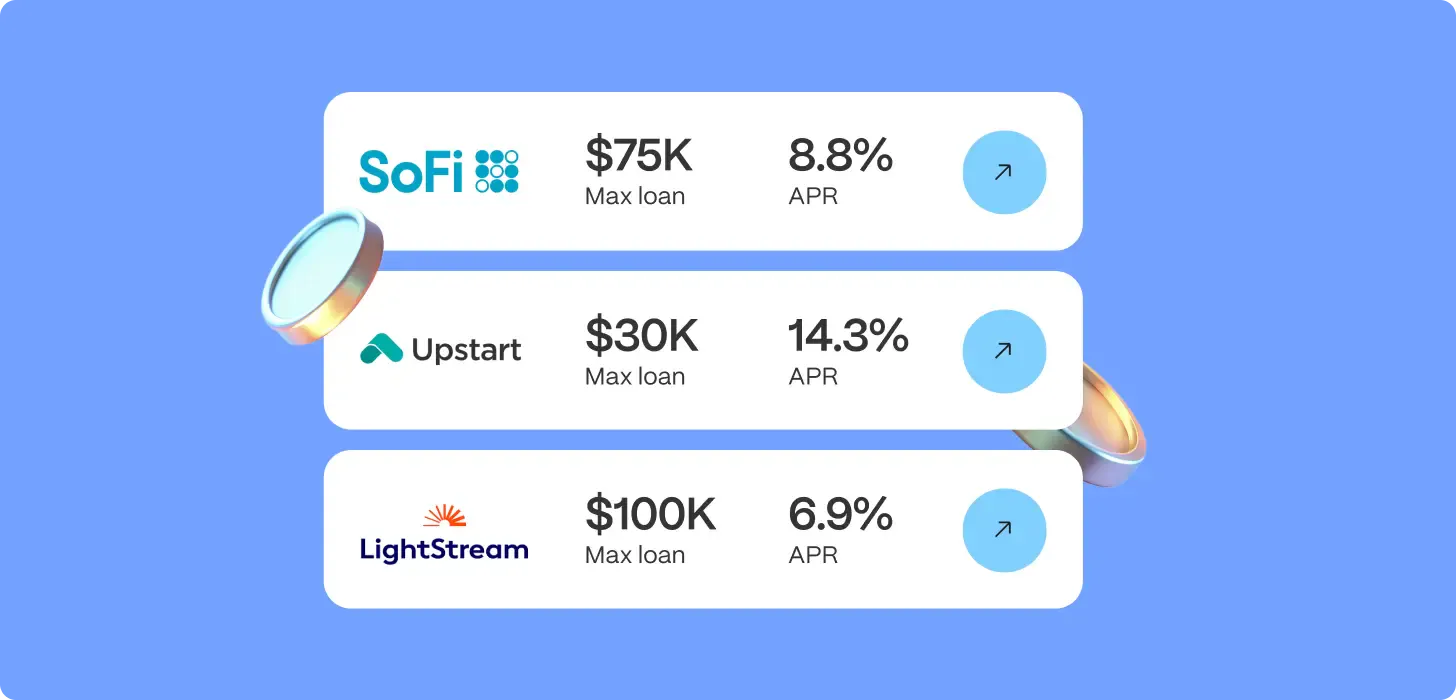

Unsecured Personal Loan Rates

Unsecured personal loan rates generally range from about 6% to 36% APR based on your situation. Where you fall within that range depends on several factors — and credit score is only one of them.

Income and Employment Stability

Steady employment and higher income signal lower risk to a lender. The longer you’ve been with the same employer, the better. A strong income can offset weaknesses elsewhere in your application. It’s one of the most straightforward ways to improve your odds.

Debt-to-Income Ratio (DTI)

Lenders want to see that your monthly debt payments don’t exceed 43% of your gross monthly income. This number tells them how much financial breathing room you actually have. A high DTI raises red flags even when income looks solid. Paying down existing debt before applying can meaningfully improve your position.

Loan Amount

Smaller loans sometimes carry higher rates because they’re more expensive to service relative to the return. A $2,000 loan costs a lender nearly as much to process as a $10,000 one. That overhead gets reflected in the rate. Borrowing a slightly larger amount can occasionally work in your favor.

Loan Term

Longer repayment periods often come with slightly higher rates because the risk extends further into the future. A 60-month loan carries more uncertainty than a 24-month one. Lenders price that in. Shorter terms usually mean lower rates but higher monthly payments.

Purpose of the Loan

Debt consolidation tends to qualify for better terms than discretionary spending. Lenders view it as financially responsible behavior. It doesn’t reduce your overall debt load, but it simplifies repayment and can lower your rate. That’s a meaningful difference over the life of a loan.

If your credit score is lower, income increasingly matters. Lenders, especially through a marketplace, will often approve borrowers with thin credit files if the paycheck is steady.

Requirements for Unsecured Personal Loans

Lenders don’t all use the same rulebook, but most evaluate a consistent set of factors when reviewing an application. Here’s what they typically look at:

- Credit score. Unsecured personal loan rates generally range from about 6% to 36% APR — a wide spread that comes down to more than just your credit score, as we explain in our guide to personal loan rates and APR. Where you fall within that range depends on several factors.

- Income. Lenders want proof of regular income, whether from employment, self-employment, disability, or retirement benefits. Depending on your situation, you’ll need to provide pay stubs, tax returns, or bank statements.

- Employment history. Lenders like to see at least 2 years at your current job, though gaps or job changes are often acceptable if you have continuous income. What matters most is that money keeps coming in reliably.

- Debt-to-income ratio. Your monthly debt payments including the new loan should not exceed 43–50% of your gross monthly income. The exact threshold varies by lender, so it’s worth checking before you apply.

- Bank account. Most lenders require a working checking or savings account for direct deposit of funds and automatic repayment. It's a basic operational requirement, not a creditworthiness check.

- Age. You must be at least 18 years old, or 19 in a few states. There is no upper age limit.

- Citizenship or residency. Most lenders require a valid Social Security number or ITIN and proof of U.S. residency. Permanent residents and certain visa holders often qualify as well.

Different lenders prioritize these factors differently. Some may overlook a short employment history if your income is strong. Others may approve you with a lower score if your DTI is excellent. Our full breakdown of personal loan requirements and eligibility covers the nuances in more detail.

Pros and cons of Unsecured Personal Loans

Before committing to any loan, it helps to weigh what you’re actually getting against what it costs you. The short version:

Pros

No collateral required, so your home, car, and savings stay out of the equation.

Pre-approval often takes minutes, with funds hitting your account within 1–3 business days.

Fixed monthly payments make it easy to plan around a set number every month.

Flexible use means you can cover almost any expense without justifying it to the lender.

Unlike a credit card, the total interest cost is locked in from day one.

Cons

Rates run higher than secured loans since the lender has no asset to fall back on.

Easy access makes it tempting to borrow more than you can comfortably repay.

You'll need to document your income, whatever the source.

Some lenders charge a prepayment penalty if you pay off the loan ahead of schedule.

Comparing offers before you commit matters more than most people realize. A difference of even two or three percentage points in APR adds up to hundreds of dollars over the life of a loan.

Unsecured vs Secured Loans

The right loan type depends largely on what you own, what you need, and how much risk you're willing to take on. Here’s how the two compare:

| Factor | Unsecured | Secured |

|---|---|---|

| Collateral | None required | House, car, savings, or other asset |

| Approval Criteria | Credit score, income, DTI | Collateral value, income, credit |

| Interest Rates | Typically 6%–36%+ | Typically 3%–10% (for mortgages/auto) |

| Risk to Borrower | Credit damage, legal action | Loss of collateral (foreclosure/repossession) |

| Typical Use | Debt consolidation, emergencies, discretionary purchases | Home purchase, car purchase, large home improvements |

Risks of Unsecured Personal Loans

Unsecured loans are flexible, but they come with costs worth understanding:

- Higher total interest cost. The price you pay for not securing the loan with collateral adds up fast — even a small rate difference means thousands more over the life of the loan.

- Credit damage from missed payments. One missed payment reports to credit bureaus and can drop your score by 50–100+ points, with collections and lawsuits following close behind. Our guide to improving your credit score outlines how to get back on track if that happens

- Debt accumulation trap. Quick approval makes it tempting to borrow more than you need, and stacking a personal loan on top of existing card debt can worsen your DTI significantly.

- Default and legal consequences. If you default, the lender can sue you, obtain a judgment, and pursue wage garnishment or bank account levies in some states.

- Impact on future borrowing. A loan default stays on your credit report for 7 years, making it considerably harder to qualify for a mortgage, auto loan, or credit card.

Unsecured loans are a practical tool when used responsibly. Borrow only what you can repay and compare rates before committing.

When an Unsecured Personal Loan May Make Sense

An unsecured personal loan tends to be the right call in a few specific situations. If you have no collateral to put up, it’s often your most accessible option. If you need money quickly, few products can match the turnaround — funds typically arrive within days, well ahead of anything that requires an appraisal or extended underwriting. And if you’re carrying balances across multiple high-interest credit cards, consolidating into a single personal loan at a lower rate can meaningfully reduce what you pay over time, even if the total debt stays the same.

When Other Options May Be Worth Considering

Unsecured personal loans are not the right tool for every situation. If you have home equity, excellent credit, or access to lower-cost financing, there are alternatives worth exploring before committing to a higher-rate personal loan.

A HELOC or home equity loan typically comes in at 4–8% for borrowers with equity to tap. A 0% balance transfer card can eliminate interest entirely for up to 21 months if your credit score is strong enough to qualify. Auto loans and mortgages offer substantially lower rates than any personal loan because the asset secures the debt. And if medical bills are the issue, many providers will negotiate a payment plan at zero interest before you ever need to borrow.

Where Pennie Financial Fits

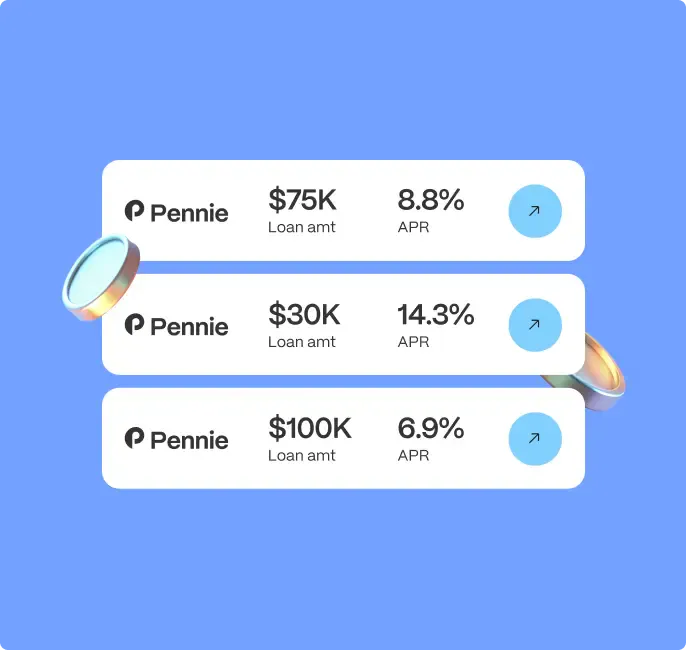

Pennie Financial is a lending marketplace, not a direct lender. When you submit a single application, the platform connects you with multiple lending partners rather than routing your request to one institution. Each partner reviews your profile independently and returns its own offer, so what you see is a genuine range of options, not a single take-it-or-leave-it decision.

From there, you compare personal loan offers side by side — amount, rate, term, and monthly payment — and choose the one that fits your situation. Pennie does not issue loans, set rates, or make approval decisions. Those decisions rest entirely with the lenders. Learn more about how the process works.

Final Thoughts

Unsecured personal loans are among the most accessible borrowing options available: no collateral, fast funding, and flexible use. What you qualify for depends on your income, credit history, and existing debt. Before committing, figure out what monthly payment fits your budget and compare offers from multiple lenders. A small rate difference adds up more than most people expect.

Frequently Asked Questions

What is an unsecured personal loan?

An unsecured personal loan is a loan that doesn’t require collateral. The lender approves you based on your credit score, income, and debt history instead.

What credit score do I need for an unsecured personal loan?

Most lenders prefer a credit score of 600 or higher, but some work with lower scores. A lender may approve you with a 550 score if your income is stable and your debt-to-income ratio is healthy.

Are unsecured personal loans harder to get than secured loans?

Unsecured loans have stricter income and credit requirements because the lender has no collateral to recover losses. However, they’re faster to approve than secured loans.

Do unsecured personal loans affect my credit score?

Only if a hard credit pull occurs — and that typically happens during final lender underwriting, not when you’re shopping for offers.

Get loan offers in as little as 60 seconds

You deserve options. So we built an industry leading platform to compete for your business.

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years

Your info is never sold