Find the help you need for any problem

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

How Long Does It Take to Get a Personal Loan? (Approval and Funding Timeline Explained)

If you’re waiting for a personal loan to come through, the timeline can feel like guessing the weather a week out. The actual timeframe stretches from a few hours to several days, depending on the situation. The biggest factors are the lender you pick and how closely your financial profile fits their criteria. Online lenders can move an application to a funded deposit in 24 to 48 hours. Traditional banks usually need three to seven business days. Credit unions sit somewhere in between.

Nothing cuts the wait more than showing up ready before you even apply. A clean application with up-to-date documents and a credit profile that the lender can verify without follow‑ups is your fastest route to cash in hand. The following text breaks down the full timeline stage by stage and shows you what can speed up or slow down the process.

In this article:

- How long does it take to get a personal loan (quick answer)

- Personal loan timeline — step by step

- How long approval takes (by lender type)

- What affects how long it takes

- How to get a personal loan faster

- Delays you should expect

- Same-day personal loans — are they real?

- Alternatives if you need money faster

- Where Pennie Financial fits

- Final thoughts

- Frequently Asked Questions

How long does it take to get a personal loan (quick answer)

The application itself eats up only a few minutes of your time. Approval might land the same day or drift into a couple of days — that part depends on the lender. Once you sign, the clock for funding starts running. That step can finish the same day or stretch to several days later. Bottom line: many online lenders will post the money to your account within 24 to 48 hours. Banks and credit unions, on the other hand, usually run on a timeline of three to seven business days.

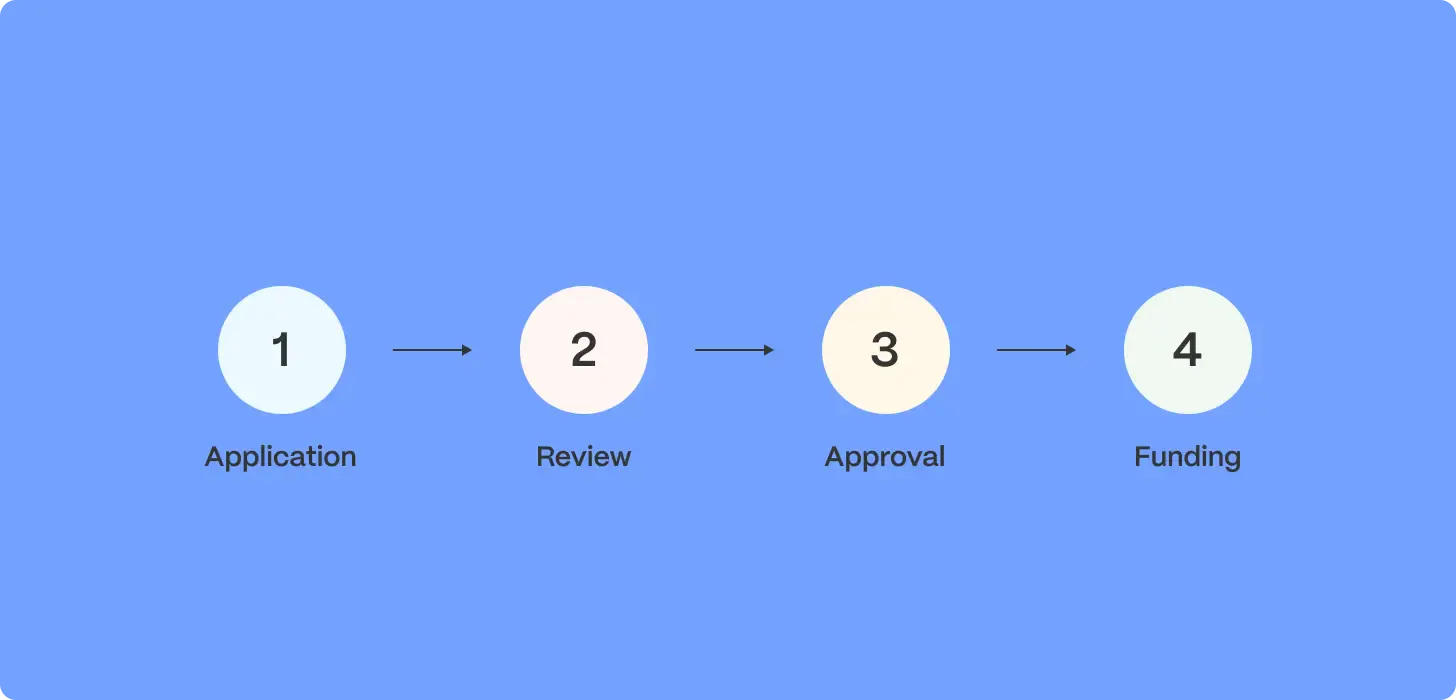

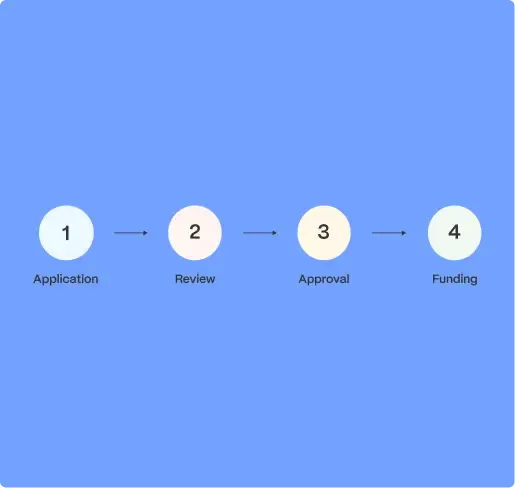

Personal loan timeline — step by step

Rather than trying to collapse everything into a single number, it helps to look at the four distinct stages a personal loan moves through. Each one has its own pace and its own variables. Let’s get into these stages:

Application submission

You can expect to spend 5 to 15 minutes filling out an online application. It asks for your personal information, employment, income, the amount you need, and what you plan to use it for. If you’re applying at a bank or credit union branch, expect it to take longer because you’ll be submitting physical documents and possibly waiting for a loan officer.

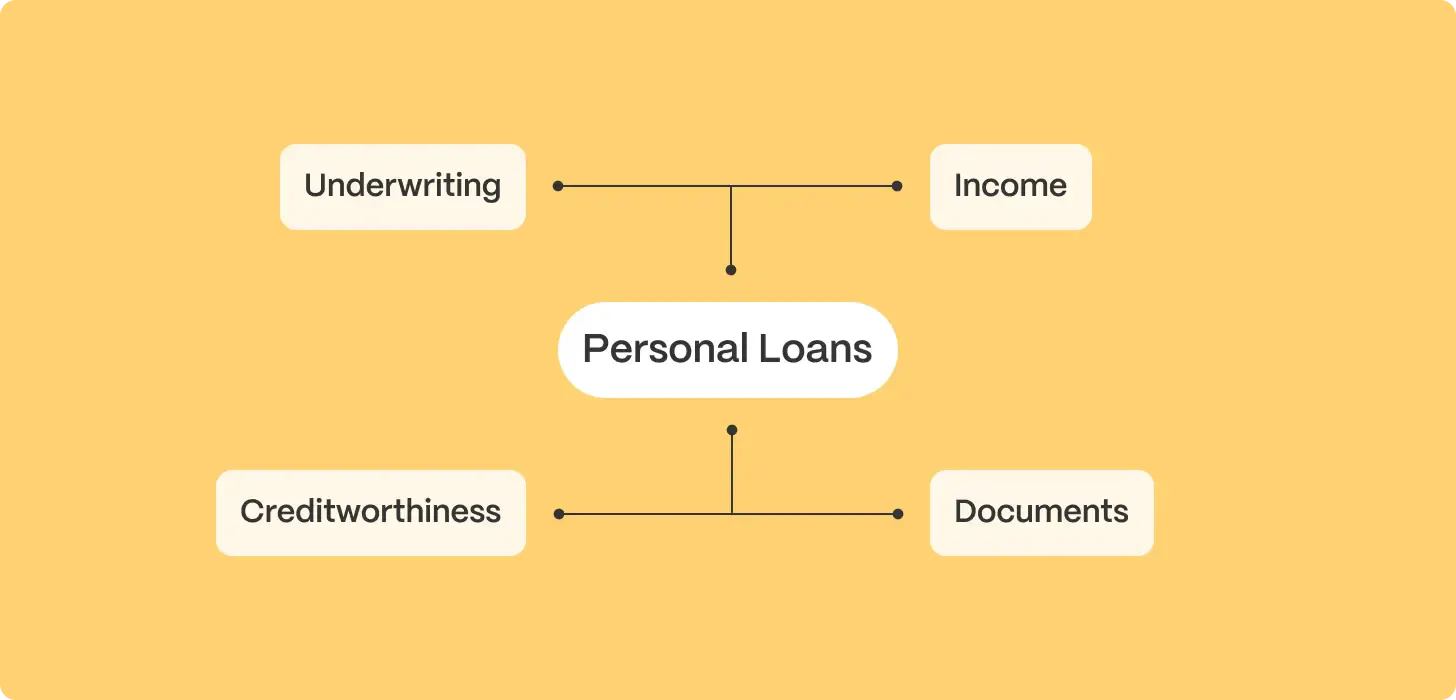

Review and underwriting

This is where the lender pulls your credit, checks your income, verifies employment, and runs its own risk models. For many online lenders, this happens in minutes using automated systems. For banks, it often involves a human underwriter reviewing the file, which takes longer.

Approval decision

Once underwriting finishes, the lender either offers you a loan, asks for more information, or declines. An offer will come with the specific APR, loan amount, and term. If you accept, you sign the loan agreement — usually electronically for online loans. Unsure how those figures translate into what you’ll pay each month?? Read our guide on personal loan rates and APR.

Funding

After signing, the lender initiates the transfer to your bank account. Many online lenders use same-day ACH for loans finalized before their daily cutoff, but funds may not post until the next business day on the receiving bank’s side. Larger loans and bank-issued loans may be funded by check or wire, which adds a day .For a full walkthrough of every stage, check out our step-by-step guide on the loan application process from start to funding.

How long approval takes (by lender type)

Lenders don’t share a single gear when it comes to approval speed. Online lenders are the quickest. Their systems run entirely on digital applications and automated underwriting, so decisions often land within minutes. For most borrowers with a straightforward profile, the approval process is near‑instant.

Banks move more slowly. Manual review steps and paper‑based processes stretch their average timeline to several days. Credit unions fall between the two — faster than most banks, but rarely as quick as a pure online lender.

Marketplace platforms are a different story. They don’t lend directly. Instead, they match you with partner lenders, each with its own approval pace. The matching itself is fast, but the final timeline depends entirely on the lender you end up with.

What affects how long it takes

Several factors determine whether your loan moves fast or gets stuck in review. Here’s how each one can speed up the timeline or slow it down.

Credit score

A clean credit profile moves through automated underwriting without a hitch. The system checks your score, sees a solid history, and clears you almost instantly. A borderline score or a thin file, however, often gets flagged for manual review. A person has to look at it, which adds hours or days.

For a full breakdown of what lenders typically expect, check out our article on personal loan requirements and eligibility.

Income verification

If your income comes from a regular W-2 job and you upload a recent pay stub, the lender can verify it in minutes. Self-employment, freelance work, or irregular pay tells the system to ask for more proof — tax returns, bank statements, profit-and-loss sheets. Each extra document adds a round of back-and-forth. For a deeper look at what lenders evaluate, read our article on how to get approved for a loan and what lenders look for.

Documentation

Submitting a complete package from the start leaves no loose ends. The lender checks every box and moves on. Leave something out — a missing signature, an outdated ID, a blurred bank statement — and the process stalls. You wait for them to ask, then wait again while they review what you send.

Lender processes

Some lenders decide in real time. Their software gives a yes or no within seconds of hitting submit. Others batch applications overnight, so a submission at 5 p.m. sits idle until the next morning. A few still use human underwriters for all loans, no matter how clean your file looks. Their speed is measured in days.

How to get a personal loan faster

A few smart moves before you apply can trim days off the usual timeline. These three steps make the biggest difference.

1. Prepare documents

Waiting until the lender asks for paperwork adds a round-trip. Have your pay stubs, ID, bank statements, and tax returns (if self‑employed) ready before you start the application. Upload everything at once. The lender checks the box and keeps moving, instead of stopping to send you a request and waiting for your reply. And if you’re curious about the score impact of shopping around for rates, read our article on whether prequalification affects your credit score.

2. Check credit first

A surprise on your credit report can derail an otherwise clean application. Get your report before you submit an application. Scan for mistakes, old collection entries, or unfamiliar accounts. Handle any corrections you can before the lender sees it. Fix what you can ahead of time. A lender who sees what they expect will approve faster than one who has to ask questions about something you didn’t know was there.

3. Apply with appropriate lenders

Choosing a lender that fits your credit profile makes a massive difference. A bank built for high‑score borrowers will likely leave you waiting. An online lender that regularly works with fair credit can size you up in minutes. Marketplaces help you skip the guesswork by matching you with partners whose criteria actually align with your situation. Picking the right match shortens the whole process dramatically.

If you’re not sure where your score stands, check out our article on what credit score you need for a personal loan.

Delays you should expect

Even a smooth application can hit friction points. Knowing what causes the common delays helps you plan around them. The main delays fall into four categories:

Missing information

Any gap — employer phone number, recent address, wrong account number — will pause the process while the lender reaches out. Respond to those requests quickly; some lenders auto-withdraw applications that go quiet for 48 hours. In the meantime, if your score is holding you back, read our guide on how to improve your credit score.

Verification issues

If your income can’t be verified digitally, the lender may request pay stubs, a letter from your employer, or tax returns. Self-employed borrowers should assume this step adds a few days.

Weekends and bank holidays

ACH transfers don’t process on weekends, and most banks don’t fund new loans on weekends either. A loan approved at 6pm Friday often doesn’t fund until Monday or Tuesday.

Fraud review holds

Lenders occasionally flag applications for a manual fraud check. Sometimes that’s triggered by unusual patterns (new address, income profile that’s atypical for the credit file); sometimes it’s random. These reviews typically clear within 24 to 48 hours.

Same-day personal loans — are they real?

Same‑day funding is real, but it doesn’t work for everyone. Some online lenders will put money in your account the same day you apply, provided you finish the application early, get approved, and sign electronically before their daily cutoff. That cutoff often falls around 2 p.m. ET. Even then, your own bank might hold the incoming funds overnight.

Getting money that fast requires three things to line up: a lender that offers same‑day funding, an instant approval decision, and a borrower profile that fits the lender’s express underwriting model. Ads promising “loans in minutes” are accurate for a lucky few. For everyone else, the fine print matters.

Alternatives if you need money faster

A personal loan isn’t the only way to get cash quickly. Sometimes, even the fastest online loan still takes a day or two. Several other options can put money in your hands within hours or less, each with its own trade‑offs:

- Credit card — instant access, but interest adds up fast if you don’t pay the balance in full.

- Cash advance on the same card — same‑day cash, though fees and immediate interest make it costly.

- Paycheck advance app — small amounts, often same‑day or by the next morning.

- Home equity line of credit (already open) — quick to draw, but your home secures the loan.

- Borrowing from family or a friend — fast and interest‑free, provided the relationship can handle it.

One example shows how this works in real life. An emergency plumbing repair costs $1,200. The plumber won’t wait two days for a personal loan. A credit card covers the bill on the spot, and the borrower pays it off the next day when the loan arrives.

If you need financing but your credit isn’t perfect, take a look at our guide on the best personal loans for fair credit.

Where Pennie Financial Fits

If speed is part of what matters to you, Pennie Financial connects borrowers with lending partners that include fast-funding online options. You can browse personal loan options and compare offers side by side based on your profile, rather than applying to one lender, waiting, and starting over if it doesn’t work out. The timeline depends on the lender you ultimately select — some partners fund within a business day; others have longer underwriting processes. Before you apply, it’s worth taking a look at how the process works from start to finish.

Final thoughts

Loan timelines don’t follow the glossy promises in ads. What a bank finishes in three days might beat an online lender that gets stuck on extra review steps. The real shortcut is boring but works every time: send a clean application, attach the right documents, and pick a lender that actually wants your profile. Add one buffer day when you’re in a hurry. When you have a week to breathe, slow down — better terms usually reward patience over panic.

Frequently Asked Questions

Can you get a personal loan the same day?

Yes, some online lenders fund the same day if you apply early, get approved quickly, and sign the loan agreement before their daily ACH cutoff.

What is the fastest way to get a personal loan?

Apply with an online lender that offers same-day or next-day funding, submit a complete application with all documents attached, apply during business hours on a weekday, and respond immediately to any verification requests.

Why does loan approval sometimes take longer?

Usually, because of verification. Income that can’t be confirmed automatically, credit file items that need explanation, documentation that's incomplete, or a fraud review flag can each add a day or more.

Do online lenders process loans faster than banks?

Generally yes. Online lenders are built around automated underwriting and electronic signatures, which compress the timeline.

How long does it take to receive funds after approval?

Commonly 1 to 2 business days. Same-day funding is possible with some lenders if you complete everything before their daily cutoff. Bank transfers take one business day; a mailed check takes longer.

Can weekends delay personal loan funding?

Yes. ACH transfers don’t process on weekends or bank holidays, so loans approved on Friday after business hours often don't fund until Monday or Tuesday.

Does your credit score affect approval speed?

Indirectly. A strong credit profile typically clears automated underwriting immediately. A borderline profile is more likely to be routed to manual review, which adds time.

Get loan offers in as little as 60 seconds

You deserve options. So we built an industry leading platform to compete for your business.

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years

Your info is never sold