Find the help you need for any problem

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

Does Prequalification Affect Your Credit Score? The Full Answer Explained

A lot of people assume that checking whether they qualify for a loan will damage their credit. That belief stops many from even looking. The truth doesn’t work that way. Prequalifying for a personal loan uses a soft credit inquiry, which leaves your credit score untouched. You can check what rates you might qualify for without any damage to your file.

Submitting a full application after prequalifying usually triggers a hard inquiry, which may cause a small temporary dip — typically a few points. That small dip fades quickly and matters far less than a single missed payment. This guide covers soft versus hard inquiries, how prequalification fits into the lending process, and how to shop for rates without hurting your credit.

In this article:

- Does prequalification affect your credit score?

- What is prequalification, and how does it work?

- Soft vs hard inquiry: what’s the difference?

- When prequalification does not affect your credit score

- When your credit score might be affected

- Can checking multiple offers hurt your credit?

- Prequalification vs preapproval: what’s the difference?

- How to check loan offers without hurting your credit

- Where Pennie Financial fits

- Frequently Asked Questions

Does prequalification affect your credit score?

Prequalification relies on a soft inquiry, so your credit score stays untouched. You can check rates with multiple lenders, compare terms, and stop there without any impact on your file. Soft inquiries don’t appear to other lenders and carry no scoring penalty. Still haven’t looked at your number? Our guide on how to check your credit score walks you through it.

You can prequalify with ten different lenders today, see exactly what each one would offer, and walk away without a single point lost. That’s the whole point of prequalification: to shop for the best rate without worrying about your credit. Only when you decide to accept an offer do you move to the formal application stage.

What is prequalification, and how does it work?

Prequalification is a lender’s early peek at your situation. You give basic details — income, loan amount, and address. The lender runs a soft credit check that leaves your score untouched. You get back an estimate: possible rate, monthly payment, and whether you’re likely to be approved.

Think of it as turning the lights on before you walk through a door. You see whether the room works for you without stepping inside. The estimate comes from a soft credit check — so your score stays exactly where it is, and no lender sees that you ever looked.

Soft vs hard credit inquiries: what's the difference?

A soft inquiry leaves no trace on your credit score. It happens during a self‑check of your credit, a lender’s prequalification, or a company’s promotional offer preparation. Other lenders never see these checks, and your score stays completely unaffected, no matter how many soft inquiries you accumulate.

Hard inquiries work differently. You only get one when you actually apply for credit — a loan, a credit card, a mortgage. You give permission, the lender pulls your full report, and your score may dip by a small number of points. That effect fades over time, and hard inquiries disappear from your report after two years, though scoring models stop counting them much sooner. The logic behind that makes more sense once you understand how credit scores are actually built.

Soft inquiry vs hard inquiry (quick comparison table)

The difference between a soft and hard inquiry comes down to what triggers them and who sees them. Here’s how the two types compare side by side:

| Aspect | Soft Inquiry | Hard Inquiry |

|---|---|---|

| Affects your credit score? | No | Small, temporary dip (a few points) |

| Visible to other lenders? | No | Yes |

| When it happens | Credit prequalification, checking your own score, promotional offers | Formal loan or credit card applications |

| How long it stays visible | Not visible to lenders at all | Up to two years on your credit report |

When prequalification does not affect your credit score

In most situations where you’re simply looking, your credit stays exactly as it is. Checking prequalification offers from a lender’s website uses a soft inquiry. Using a marketplace to compare rates from multiple lenders also relies on soft pulls. Any tool that checks your eligibility before you formally apply is designed to leave your score unchanged.

You can run these checks as many times as you want. The results may vary across lenders, but your score never drops from the search. As long as you stay at the prequalification stage – without submitting a full application or signing a loan agreement – you’ve triggered no hard inquiry and lost no points.

When your credit score might be affected

Now you know when your credit score holds firm. Let’s look at situations with the opposite effect:

The typical impact of a hard inquiry

A single hard inquiry usually lowers a credit score by a small amount — often just a few points — and the impact fades within a few months. Multiple hard inquiries in a short window can compound, though, which is why rate-shopping windows exist. If damage has already been done, our article on improving your credit score lays out what actually moves the needle.

Hard inquiries stay on your credit report for up to two years, but affect credit scoring calculations for a shorter period — typically around 12 months or less in most scoring models.

When the hard inquiry isn’t triggered

If you prequalify and decide not to submit a full application, there’s no hard inquiry and no impact. If you prequalify with five different lenders and never apply to any of them, all five were soft inquiries, and none affected your score.

Can checking multiple offers hurt your credit?

Checking multiple prequalification offers won’t hurt your credit because each check uses a soft inquiry. You can look at rates from five different lenders today and lose zero points from your score. That’s the whole point of prequalification — to let you shop without penalty.

The situation changes slightly when you move from prequalification to formal applications. Each formal application triggers a hard inquiry, and several hard inquiries in a short window could lower your score by a small amount.

But credit scoring models recognize rate shopping for personal loans, mortgages, and auto loans. They typically count multiple hard inquiries made within a 14‑ to 45‑day window as a single event, so your score doesn’t get penalized for each separate application.

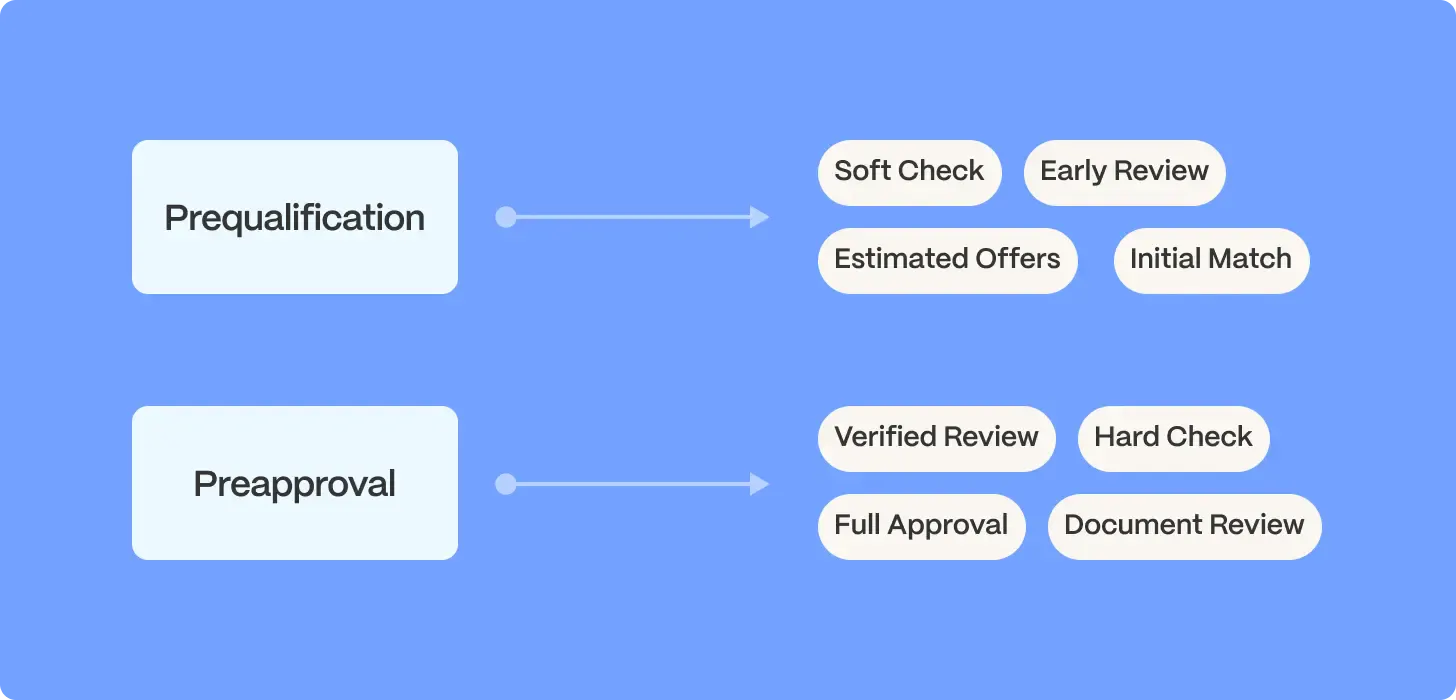

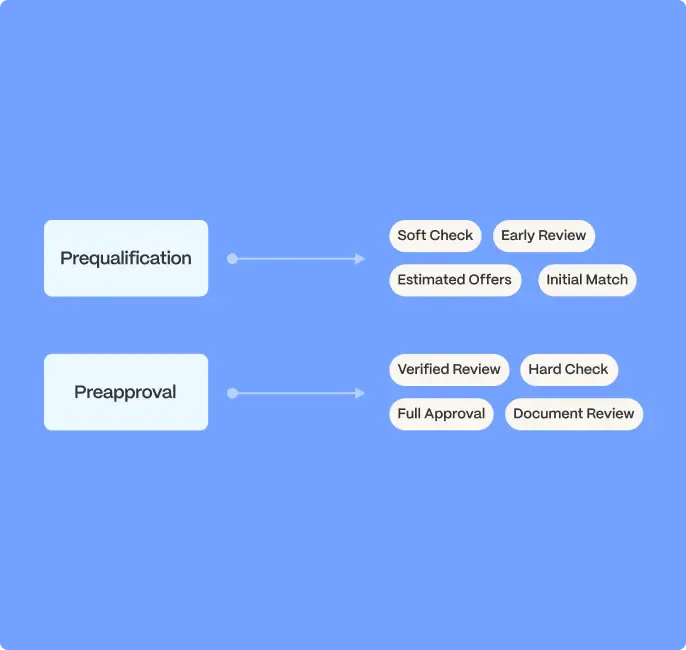

Prequalification vs preapproval: what’s the difference?

These terms get used loosely, and different lenders mean slightly different things by them. In the personal loan space, the distinction is often practical rather than technical. Here’s how the two terms usually break down:

Prequalification

A lender runs a soft inquiry and provides indicative offers based on limited information. The lender still needs to verify income, employment, and run a hard credit check before funding. That final stage is a different beast — our article on what lenders actually look for when they review a full application breaks it down.

Preapproval

In personal lending, “preapproval” is sometimes used interchangeably with prequalification. In other contexts — like mortgages — preapproval is a more rigorous process that may involve a hard credit pull and full documentation review.

Always read the fine print to confirm whether a check is a soft or hard inquiry. Reputable lenders disclose this clearly before pulling your credit.

How to check loan offers without hurting your credit

Shopping for a loan should feel like comparing prices, a calm search for the best deal. Prequalification lets you kick the tires on real offers using a soft check, even if you check five or ten lenders.

Quick checklist before you compare offers

A few simple steps keep your credit safe while you shop. Run through these points before you start comparing:

- Confirm that the prequalification check uses a soft inquiry. Reputable lenders disclose this clearly.

- Gather basic information: income, address, loan amount, and purpose.

- Check at least three lenders or use a marketplace to see multiple offers at once

- Check at least three lenders or use a marketplace to see multiple offers at once.

- Compare APRs — not just monthly payments — to see the real cost of each loan.

- Walk away if you don’t like the terms. No hard inquiry has touched your credit yet.

If you need a starting point, our roundup of the best personal loans gives you a shortlist worth comparing.

Where Pennie Financial Fits

Pennie Financial helps you see real loan offers without guessing or hurting your credit. You fill out one form, and the platform runs a soft credit pull to show you prequalified options from multiple lenders. Your score stays completely unchanged during this process. You can see personal loan options, compare APRs and terms, and choose the best fit — all without a hard inquiry.

Once you pick an offer, the formal application goes through the lender. That’s when a hard inquiry may happen, but only after you’ve decided to move forward. For a closer look at how the platform operates, see how Pennie works.

Frequently Asked Questions

Does prequalification hurt your credit score?

No — prequalification uses a soft credit inquiry, which does not affect your credit score.

How many times can I prequalify without hurting my credit?

As many as you want. Because each prequalification is a soft inquiry, the number of checks doesn’t affect your credit score.

What’s the difference between a soft and a hard credit inquiry?

A soft inquiry doesn’t affect your credit score and is visible only to you on your credit report. A hard inquiry may cause a small temporary score dip and is visible to other lenders.

Does prequalification guarantee approval?

No. Prequalification is an indicative check based on limited information. The final offer depends on full underwriting, which verifies income, employment, and pulls a full credit check.

How long does a hard inquiry stay on your credit report?

Hard inquiries stay on your credit report for up to two years, but typically affect credit scoring calculations for a shorter period — often around 12 months or less in most modern scoring models.

Is checking my own credit score a hard inquiry?

No. Checking your own credit through a free service is a soft inquiry and doesn’t affect your score. You can check your credit as often as you want without any impact.

If I prequalify and don’t take the loan, does anything show up on my credit report?

Only a soft inquiry, which is visible only to you — not to other lenders. There’s no impact on your credit score and no record visible to others that you prequalified.

Get loan offers in as little as 60 seconds

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years