Looking at personal loan options across multiple lenders? Pennie Financial connects you with a network of lending partners — including those who weigh income alongside credit — so you can compare real offers for your actual financial profile before deciding.

Find the help you need for any problem

Topics

Personal loans

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

Ready to move forward?Get started

Best Personal Loans: Types & How to Choose the Right One

Getting a personal loan doesn’t feel complicated at the surface level. You receive a defined sum from a lender and repay it in fixed monthly installments over a set period at a predetermined interest rate. Simple enough in structure — but the differences between loan types, lenders, and terms can meaningfully change what you actually pay. A loan that looks affordable based on the monthly payment might carry a higher total cost than a different loan with a slightly higher payment and a shorter term. The reverse is also true. Small differences in rates, fees, and structure compound over time.

Most borrowers accept the first offer they qualify for. That’s usually a mistake. The spread in rates and terms across lenders for the same borrower can be several percentage points, which is real money over a multi-year loan. The single most useful thing you can do before committing to any personal loan is to compare multiple options rather than defaulting to whoever responds first.

In this article:

- What Is the Best Personal Loan for You?

- Types of Personal Loans Explained

- How to Choose the Best Personal Loan

- How to Compare Personal Loans

- Best Personal Loan Options by Financial Situation

- Frequently Asked Questions

What Is the Best Personal Loan for You? Key Factors to Consider

The “best” personal loan is contextual. A loan that’s excellent for a borrower with a 750 credit score, steady employment, and a clear repayment plan may be entirely wrong for someone with a 580 score, variable income, and a different borrowing purpose. What makes a loan the right fit depends on several factors specific to you.

Your Monthly Budget

The payment has to be sustainable for the full term. A lower monthly payment sounds better, but it usually comes from a longer term, which means more total interest paid. Choosing an amount aligned with your regular budget helps avoid strain over time.

Your Purpose

Debt consolidation, emergency expenses, home improvement, and medical bills each call for different loan structures. The purpose shapes the amount, the term, and which lender types are most relevant.

Your Credit and Income Profile

The rate you’re offered depends heavily on both. A borrower with strong credit and documented income has access to different pricing than someone with a thinner file. Both can find options suited to their situation by comparing across enough lenders.

Your Risk Tolerance

Secured loans offer lower rates in exchange for collateral risk. Unsecured loans cost more but don’t require putting assets up. That tradeoff is worth thinking through before you start applying.

Types of Personal Loans Explained: Which One Fits Your Needs?

Loan types differ in cost, risk level, eligibility requirements, and borrower protections. They’re not interchangeable — and knowing which category you’re evaluating matters before you start comparing rates.

1. Unsecured Personal Loans

These loans don’t require any collateral, so the lender assumes all the risk. Eligibility hinges primarily on your credit history, income, and overall debt load. Rates are higher than secured alternatives because the lender has nothing to fall back on if you default. For most borrowers with fair to good credit and a defined borrowing purpose, this is the standard starting point.

2. Secured Personal Loans

With a secured personal loan, you pledge an asset — like a car, savings account, or certificate of deposit — to support the borrowing. This arrangement lowers the lender’s risk, which usually translates into a better interest rate. Miss a payment, and the asset could be claimed, so it’s important to borrow within your means.

3. Debt Consolidation Loans

A personal loan is used to pay off multiple existing debts — usually high-rate credit cards — rolling them into a single payment at a single rate. If the consolidation rate is lower than your current blended rate across existing balances, the math can work substantially in your favor. Understanding how a debt consolidation loan works before applying is worth the time — the structure, the fee implications, and whether the numbers actually pencil out for your situation.

4. Fixed-Rate Personal Loans

Most personal loans fall into this category — your rate and monthly payment don’t change from month one through the final payment. That predictability has genuine value: you can budget around a fixed obligation. Variable-rate personal loans exist but are far less common. The payment uncertainty generally isn’t worth whatever rate savings they might offer at origination.

5. Co-Signed Personal Loans

A creditworthy co-signer joins the application, their profile supporting yours. This can unlock better rates and approval odds for borrowers with limited or damaged credit. Both you and the co-signer share the consequences of missed payments, so any slip-up hits their credit too. Because of this, it’s essential to discuss the arrangement openly before anyone commits to co-signing.

6. Credit Union Personal Loans

Member-owned and often more flexible than commercial lenders on credit score thresholds, particularly for existing members with account history. Rates are generally competitive. Many credit unions also offer credit-builder products specifically for borrowers trying to establish a payment track record. If you have an existing membership, this is worth a conversation before going elsewhere.

7. Online Personal Loans

Available through digital-first lenders and marketplace platforms. The main advantages are speed and comparison access — a single application can surface offers from multiple lenders, letting you evaluate real APRs side by side. Online personal loan options vary significantly in interest rates, terms, and eligibility criteria. Before applying for any loan, it’s also worth understanding how personal loans affect your credit score.

8. Short-Term and High-Cost Loans

Payday loans, cash advances, and similar products are in a different category from personal installment loans. The effective APRs can run 300% or higher, repayment terms are measured in weeks rather than years, and repayment is often structured around your next paycheck. These are not personal loans in the conventional sense. If you’re evaluating short-term options, a personal loan vs a line of credit comparison typically offers a more predictable structure at substantially lower cost.

How to Choose the Best Personal Loan

Choosing the right personal loan starts with understanding your own financial picture and borrowing goals. Taking a moment to clarify what you need and why sets the stage for evaluating options that truly fit your situation.

Identify Your Purpose First. The borrowing purpose shapes everything else: the amount, the appropriate term, and which lender types make sense. Debt consolidation, emergency expenses, and home improvement have different borrowing profiles. Starting with purpose prevents you from optimizing for the wrong thing.

Decide How Much You Actually Need. Borrow what the situation requires — not more. Over-borrowing increases total cost; under-borrowing may mean a second application later, with another hard inquiry and potentially worse terms. Be specific before you apply.

Review Your Financial Situation Honestly. Pull your credit report, calculate your debt-to-income ratio, and have income documentation ready. Knowing your profile before applying lets you target lenders whose criteria you’re likely to meet, which reduces unnecessary hard pulls and the associated temporary credit score impact.

Compare Multiple Options Before Deciding. One lender’s offer tells you almost nothing about what the market has for your profile. The rate spread between lenders for the same borrower can be several percentage points, which over a three-to-five-year term is a meaningful dollar difference. Prequalify with soft pulls before committing to full applications.

Read the Full Terms Before Applying. APR (which includes fees), origination fee amount, prepayment penalty language, late fee structure, and confirmation that the rate is fixed. Each of these affects what you actually pay.

How to Compare Personal Loans: What to Look For Before You Apply

Before applying for a personal loan, focus first on the factors that have the biggest impact on your monthly budget and likelihood of approval. Paying attention to these key elements first will make the rest of the process smoother:

- Monthly payment affordability — make sure the payment fits comfortably within your realistic monthly budget.

- Total repayment amount — look at the full amount you’ll repay to understand the true cost of the loan.

- Loan term length — shorter terms mean higher monthly payments but less interest overall, while longer terms lower each installment at the cost of more interest over time.

- Approval requirements — check that your credit score, income, and DTI ratio meet the lender’s criteria.

Once you’ve addressed these critical elements, it’s worth reviewing additional factors that can affect cost, convenience, and flexibility:

- Fees (origination, late, prepayment) — evaluate any charges that could add to the total cost.

- Flexibility (early repayment options) — see if the lender allows early payoff without penalties.

- Compare at least 2–3 lenders — looking at multiple offers helps identify the most favorable terms.

- Use prequalification where available — check potential loan options with a soft inquiry that leaves your credit score unchanged.

- Review full terms before committing — read the complete agreement, including fine print and less obvious clauses.

- Check lender credibility — confirm the lender is licensed and transparent about their operations.

Comparing options through a marketplace platform like Pennie Financial routes a single application across multiple lenders — letting you see real offers side by side without triggering separate hard inquiries for each. See how Pennie’s lender matching works before applying.

Before making a decision, run through a quick checklist to ensure you’ve considered the most important details:

1. Can I comfortably afford this payment every month for the full term?

2. What is the total repayment amount — not just the monthly payment?

3. Are there origination fees, prepayment penalties, or other costs I haven’t accounted for?

4. Do I fully understand the repayment terms, including what happens if I miss a payment?

5. Is this lender licensed and verifiable in my state?

Best Personal Loan Options Based on Your Financial Situation

Your financial background shapes which loans make sense and how much you can realistically afford. Here’s a snapshot of common situations and the options that tend to work best for each:

| Situation | Best Fit | Key Consideration |

|---|---|---|

| Good credit (700+) | Unsecured personal loan from a bank, credit union, or online lender. | Comparison matters most — rate spreads across lenders can be significant even at this tier. |

| Fair or bad credit (below 670) | Income-focused lenders, secured loans, or co-signed applications. | Rates reflect risk; evaluate total repayment cost carefully before committing. |

| Debt consolidation | Personal installment loan at a rate lower than your current blended rate. | Interest savings must justify origination fees; bad credit options exist. |

| Fast funding needed | Online lenders and marketplace platforms. | Speed is not the same as a good deal — review terms carefully, regardless of timeline. |

| Limited credit history | Credit union credit-builder loans, secured loans, and co-signed applications. | The goal is building payment history, not just accessing funds. |

Your options depend on your credit and goals. Strong credit opens up the most choices, while fair or limited credit often means looking at secured or co-signed loans. Debt consolidation makes sense only if it lowers your overall rate, and even without a credit history, building a track record or using a secured option can get you started. For guidance, check how to secure a loan with no credit and get a debt consolidation loan with bad credit.

Frequently Asked Questions

How do I choose the best personal loan for my situation?

Start with your purpose, budget, and credit profile. Then compare multiple lenders using APR.

What should I check before accepting a personal loan offer?

Confirm the APR includes all fees, calculate total repayment cost, check for prepayment penalties, verify the rate is fixed for the full term, and confirm the lender is licensed in your state.

How many lenders should I compare?

At a minimum of two or three.

Can I get a personal loan with bad credit?

Yes, though the options are narrower and rates are higher.

Does checking loan options affect my credit score?

Prequalification with a soft credit pull does not affect your score. A full application triggers a hard inquiry.

How fast can I get approved for a personal loan?

Approval times vary: online lenders can fund within a day or two, while traditional banks usually take several business days.

What’s the difference between interest rate and APR?

The interest rate shows the lender’s base charge for borrowing, and the APR adds fees to reveal the loan’s total cost.

Share

Ready to move forward?Get started

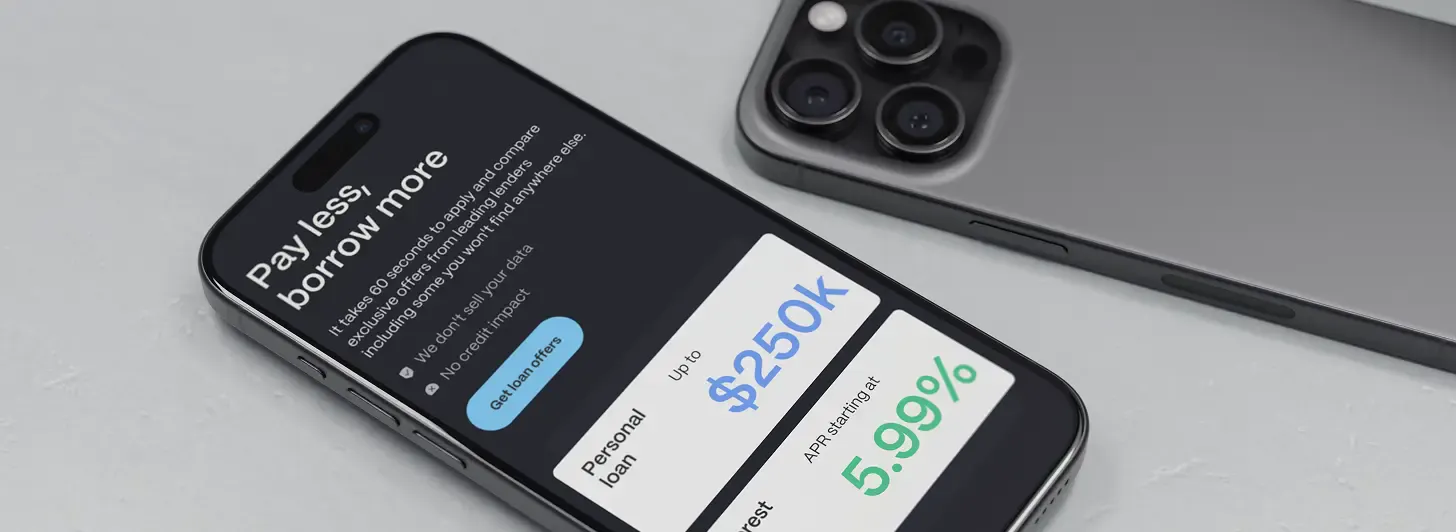

Get loan offers in as little as 60 seconds

You deserve options. So we built an industry leading platform to compete for your business.

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years

Your info is never sold