Find the help you need for any problem

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

What Is a Credit Score and How Does It Work

Most people have heard of a credit score. Fewer actually know what goes into it. It’s a three-digit number that lenders use to gauge how likely you are to repay what you borrow — and it shows up every time you apply for a loan, a credit card, or even a rental apartment. A higher score generally means better terms and more options. A lower one can mean higher rates, stricter conditions, or an outright denial.

And the gap between those outcomes can be significant — sometimes thousands of dollars over the life of a loan. What surprises most people is how the number is actually calculated, why it shifts over time, and why it can look different depending on where you check it. This guide breaks all of that down without the jargon.

In this article:

- What Is a Credit Score

- Why Your Credit Score Matters

- What Is Considered a Good Credit Score

- How Credit Scores Are Calculated

- Why You May Have Different Credit Scores

- How Lenders Use Your Credit Score

- How to Check Your Credit Score

- Pennie's Role in the Lending Process

- Frequently Asked Questions

What Is a Credit Score

At its core, a credit score is a three-digit number that measures creditworthiness. The most common range is 300 to 850, though some models use slightly different scales. Think of it as a grade for how you have managed credit in the past.

The meaning of a credit score is straightforward: it predicts your likelihood of repaying a debt on time. A higher score signals to lenders that you have historically paid your obligations, managed credit responsibly, and pose less financial risk. A lower score suggests you have missed payments, carried high balances, or had other credit problems that make lenders nervous.

Lenders need a fast way to evaluate thousands of applicants. That is why credit scores exist. Without them, every lending decision would require hours of manual review. The score compresses your financial behavior into one number that lenders can reference in seconds.

Why Your Credit Score Matters

When you apply for a personal loan or any other credit product, lenders use your score as a starting point for evaluating risk. It influences whether you get approved, what interest rate you’re offered, and what repayment terms are on the table. A borrower with a score of 760 and a borrower with a score of 580 applying for the same loan will likely see very different offers — sometimes a difference of ten or more percentage points in APR.

That said, credit score is one input among several. Lenders also weigh your income, employment stability, existing debt load, and overall financial profile. A strong score can open doors, but it doesn’t guarantee approval, and a lower score doesn’t automatically close them. Understanding how personal loans can affect your credit score is part of managing both strategically.

What Is Considered a Good Credit Score

Credit score ranges vary slightly depending on the scoring model, but here is the general framework used by most major lenders:

| Score Range | Rating | What It Means |

|---|---|---|

| 300–669 | Poor to Fair | High risk; harder to qualify; higher rates if approved |

| 670–739 | Good | Acceptable risk; reasonable rates; decent approval odds |

| 740–799 | Very Good | Low risk; competitive rates; strong approval odds |

| 800–850 | Excellent | Lowest risk; best rates; highest approval odds |

The higher the score, the better, but the minimum score you need depends on the specific lender and loan product.

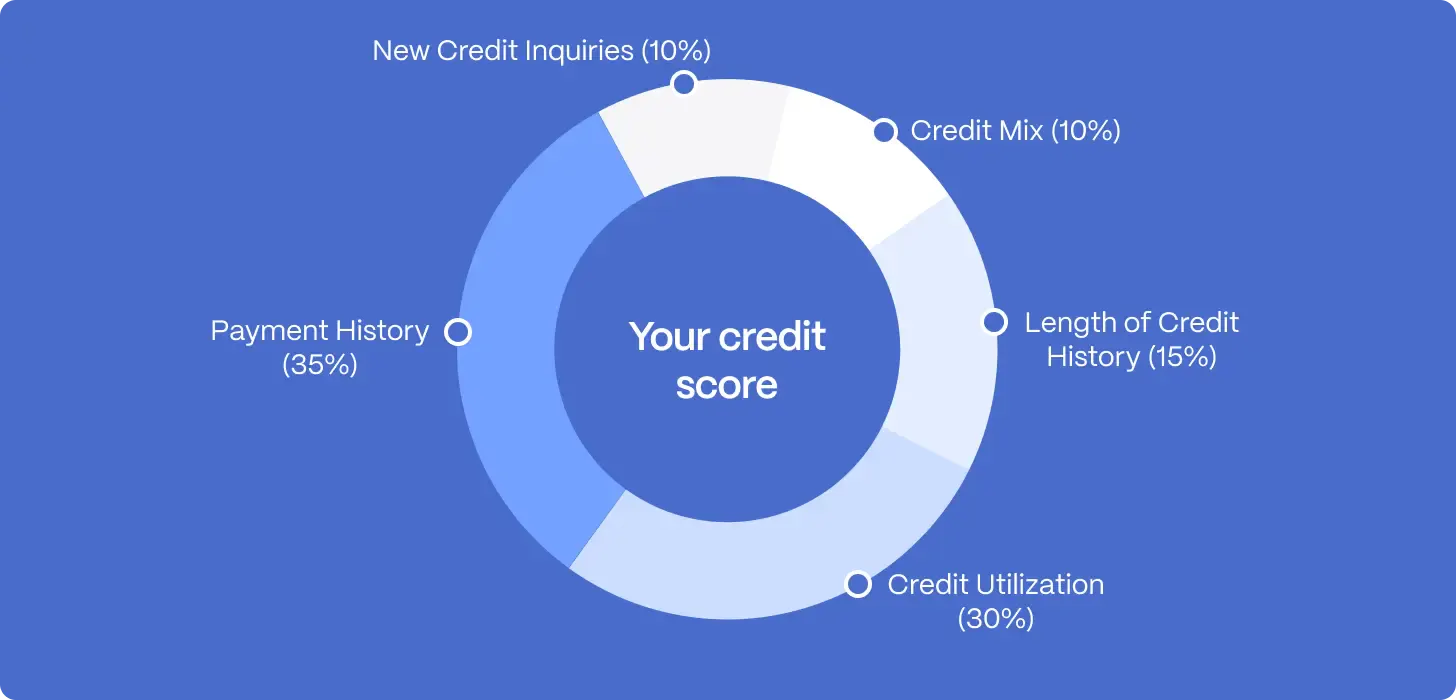

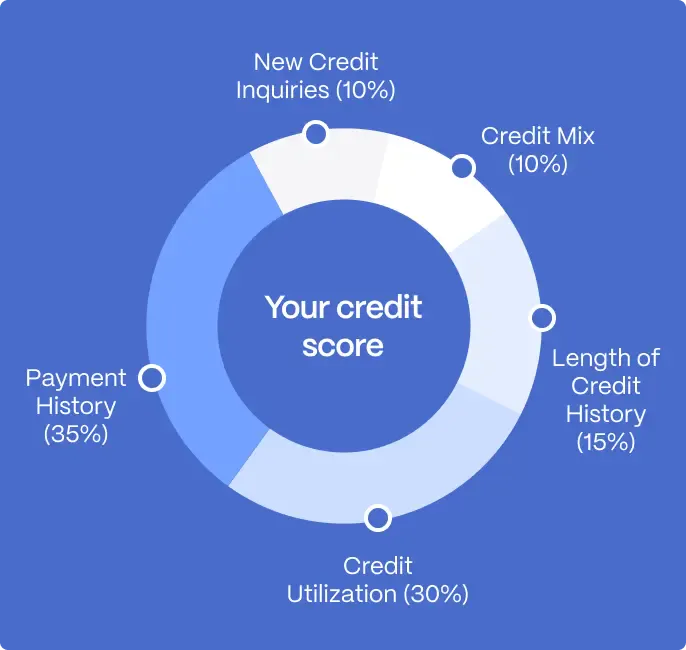

How Credit Scores Are Calculated

Your credit score is calculated using five main factors. They are not weighted equally — some matter much more than others.

Payment History (35%)

This is the heaviest factor in most scoring models. It measures whether you have paid your bills on time. Missed payments, late payments, collections, charge-offs, and bankruptcies all damage your payment history. A single missed payment can drop your score by 50–100 points. Recent damage matters more than old damage. If you paid late but eventually caught up, that is better than a missed payment, but still counts against you.

Credit Utilization (30%)

This is the percentage of available credit you are actively using. If you have a credit card with a $5,000 limit and a $2,500 balance, your utilization is 50%. Lower utilization is better. Most scoring models favor utilization below 30%. Maxing out your cards, even if you pay them off monthly, signals financial stress and damages your score. Utilization recalculates monthly, so it is one factor you can improve quickly by paying down balances.

Length of Credit History (15%)

This measures how long your credit accounts have been open. Older is generally better. If you opened your first credit card at age 20 and you are now 50, you have 30 years of credit history, which boosts your score. Closing old accounts or having accounts closed can shorten your average account age and hurt your score. Closing your oldest credit card, even if you never use it, can be counterproductive.

Credit Mix (10%)

Lenders want to see that you can handle different types of credit responsibly. Having only credit cards is less favorable than having credit cards, an auto loan, a mortgage, and other forms of credit. This does not mean you should take on debt you do not need—it just means having diverse credit accounts works in your favor.

New Credit Inquiries and Recent Accounts (10%)

When you apply for credit, a lender pulls a hard inquiry into your credit report. Multiple hard inquiries in a short time can lower your score because they signal you are actively seeking credit — which may indicate financial desperation. Opening new accounts also temporarily lowers your score. However, rate-shopping for mortgages or auto loans within 14–45 days (depending on the model) usually counts as a single inquiry, so shopping around does not penalize you as much as you would think.

Different credit scoring models — FICO, VantageScore, and specialty models used by specific lenders — weigh these factors differently. The percentages above reflect the most common FICO model, but variations exist. What matters most is understanding the general structure: payment history dominates, followed by utilization, history length, mix, and new credit.

Why You May Have Different Credit Scores

If you check your credit score from three different sources and get three different numbers, do not panic. Score variations are normal. Here is why:

1. Different Credit Bureaus

There are three major credit reporting bureaus: Equifax, Experian, and TransUnion. Each maintains its own credit report and score. If information is reported to one bureau but not the others, your scores will differ. Some lenders report to all three; others report to only one or two. Over time, the bureaus tend to sync up, but at any moment, they may have slightly different data.

2. Different Scoring Models

FICO (the most common model, used by roughly 80% of lenders) comes in multiple versions. There is FICO 8 (standard), FICO 9 (recent), and industry-specific versions like FICO Auto Score and FICO Bankcard Score. VantageScore is an alternative model created by the three bureaus. Credit card companies, insurance companies, and specialty lenders may use proprietary models. A single credit report can generate a dozen different scores depending on which model calculates it.

3. Different Update Cycles

Your credit report updates continuously as creditors report new information. However, the timing varies. One bureau might receive a payment report before another. If you check your score on Tuesday, the bureaus might reflect different data by Friday. Score fluctuations of 10–20 points month to month are normal and usually minor.

Your credit score is not a single fixed number. It is a snapshot that changes constantly. Knowing your approximate score (within 50 points) is useful; obsessing over a 5-point fluctuation is not.

But when your score takes an unexpected dive — no missed payment, nothing obvious — you can find more on that in our article about why your credit score dropped. It covers hidden triggers like a closed account shifting your utilization or an old collections entry appearing out of nowhere.

How Lenders Use Your Credit Score

Your credit score is a starting point. Lenders use it as part of a broader evaluation that includes income, employment history, debt-to-income ratio, and the type of credit you’re applying for. A borrower with a middling score and strong, stable income can look more attractive to some lenders than a borrower with a higher score and irregular earnings.

Approval decisions, rates, and terms vary significantly from one lender to the next. That’s why comparing offers across multiple lenders — rather than applying to one and accepting whatever comes back — tends to produce better outcomes. If you’re curious about options when credit history is limited, our guide on how to secure a loan with no credit covers that ground in detail.

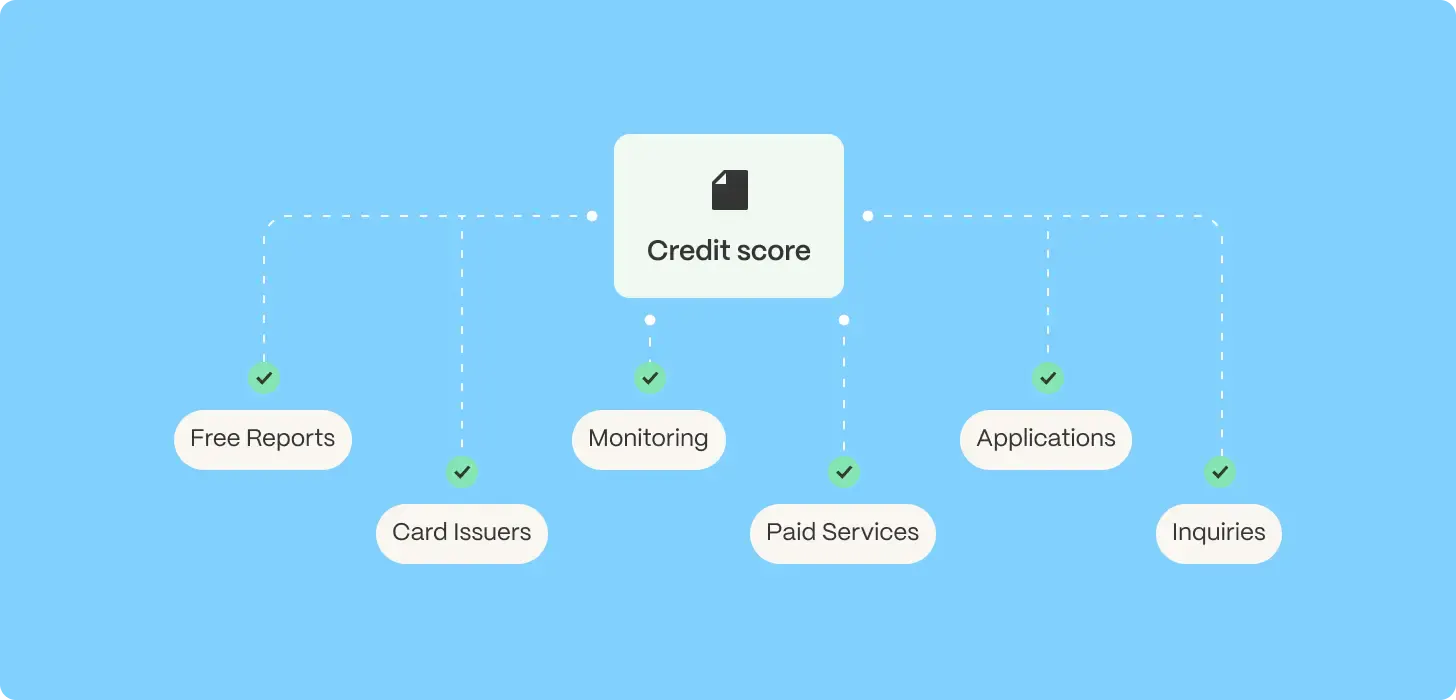

How to Check Your Credit Score

You can access your credit score through several channels:

Free Credit Report Access

You are entitled to one free credit report per year from each of the three major bureaus at annualcreditreport.com. This report shows your history but not a numerical score in all cases.

Credit Card Issuers

Many major credit card issuers (Chase, American Express, Discover, etc.) provide free credit scores to their cardholders. This is often FICO 8 or VantageScore. It updates monthly.

Free Credit Monitoring Services

Apps and websites like Credit Karma, NerdWallet, and Experian offer free credit scores. These are usually VantageScore or non-FICO models. They are useful for tracking trends but may differ from the FICO scores lenders actually use.

Paid Score Services

FICO Score is an official website (myfico.com) that allows you to purchase your official FICO scores directly.

When Applying for Credit

When you apply for a loan or credit card, the lender pulls your score as part of the process. You do not need to check it beforehand—the lender will do it.

Pick one or two free sources and check regularly (monthly or quarterly). Tracking your score over time matters more than obsessing over a single snapshot. Need a full walkthrough of every method — including which free scores actually match what lenders use? We’ve got a separate guide that breaks it all down. Focus on the actions that improve your score: paying on time and lowering credit utilization.

Soft Inquiries vs. Hard Inquiries

Checking your own credit score is a soft inquiry and does not affect your score. Hard inquiries (from lenders when you apply for credit) may temporarily lower your score by 5–10 points. Soft inquiries (credit monitoring, employer checks) do not count.

Pick one or two free sources and check regularly (monthly or quarterly). Tracking your score over time matters more than obsessing over a single snapshot. Focus on the actions that improve your score: paying on time and lowering credit utilization.

Pennie’s Role in the Lending Process

Pennie Financial is a lending marketplace. When you submit an application, the platform routes it to multiple lending partners, each of which reviews your profile independently and returns its own offer. Pennie does not calculate credit scores, set rates, or make approval decisions — those come from the lenders themselves.

What the platform does is give you a range of real offers to compare in one place, based on a soft credit pull that doesn’t affect your score. From there, you choose. Learn more about how the process works, or explore available personal loan options. If you're weighing different borrowing structures, our breakdown of personal loan vs line of credit may also be useful.

Frequently Asked Questions

What is a credit score in simple terms?

A credit score is a number between 300 and 850 that summarizes how responsibly you have managed credit in the past.

How is your credit score calculated?

Your score is calculated using five main factors: payment history (35%), credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit inquiries (10%).

What is the meaning of total credit score?

Total credit score typically refers to your overall credit score from a specific bureau or model.

What is a good credit score to get a loan?

It depends on the lender and loan type. For personal loans, many lenders look for 620–650 or above, though some work with lower scores. For mortgages, 620 is a common floor, with 740+ unlocking the best rates. For credit cards, 670+ is often workable.

Does checking your credit score affect it?

Checking your own credit score is a soft inquiry and does not affect your score.

Why do credit scores vary?

Credit scores vary because different bureaus have slightly different information, different scoring models exist, and your credit profile is constantly updating.

How often does your credit score update?

Your credit report updates continuously as creditors report activity. Scores typically update monthly, though some update more frequently.

Can you improve your credit score quickly?

Some changes — like paying down a high credit card balance — can move the number within a billing cycle or two. Our guide to improving your credit score covers the most effective approaches in order of impact.

Get loan offers in as little as 60 seconds

You deserve options. So we built an industry leading platform to compete for your business.

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years

Your info is never sold