Find the help you need for any problem

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

Loan Application Process: Step-by-Step Guide from Application to Funding

In this article:

- How Loan Applications Actually Work

- Overview of the Loan Application Process

- Step-by-Step Loan Application Process

- What Lenders Evaluate During the Process

- Loan Application Timeline: How Long It Takes

- What Can Delay Your Loan Application

- What Happens After You Apply

- How to Improve Your Chances Before Applying

- When You May Get Approved vs Denied

- Where Pennie Financial Fits

- Final Thoughts

- Frequently Asked Questions

How Loan Applications Actually Work

When you apply for a personal loan, more happens behind the scenes than most people expect. Lenders run credit checks, review your finances, and may give conditional approval before the final yes. You might need to provide documents. Funding eventually shows up — but how fast depends on who you apply with and how. Most people don’t realize there are two very different paths to get there.

The traditional way means applying to lenders one at a time. Each application triggers a hard credit pull, and a rejection sends you back to the start. A marketplace flips that: one application, one soft pull, and you see pre-approved offers from multiple lenders side by side before committing. Same loan at the end. Just a smarter path to get there. This guide walks you through both so you can compare timing, process, and which approach puts you in control.

Overview of the Loan Application Process

Applying for a loan is straightforward on the surface. What happens behind it is more involved. Once you submit an application, the lender runs their own evaluation — independently, on their own timeline, against their own criteria.

You don’t control that part. What you can control is how prepared you are going in and how quickly you respond if they need something from you. Understanding personal loan requirements and what lenders typically look for before you before you submit puts you in a better position from the start.

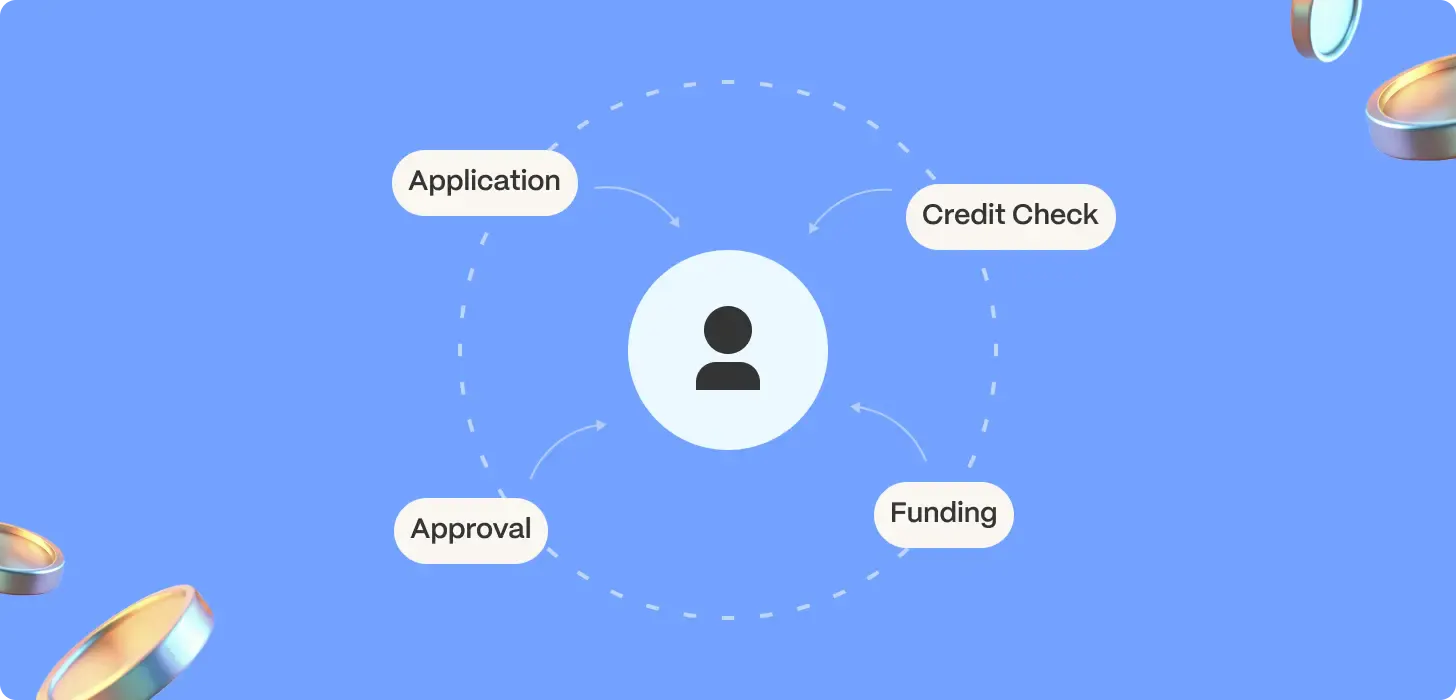

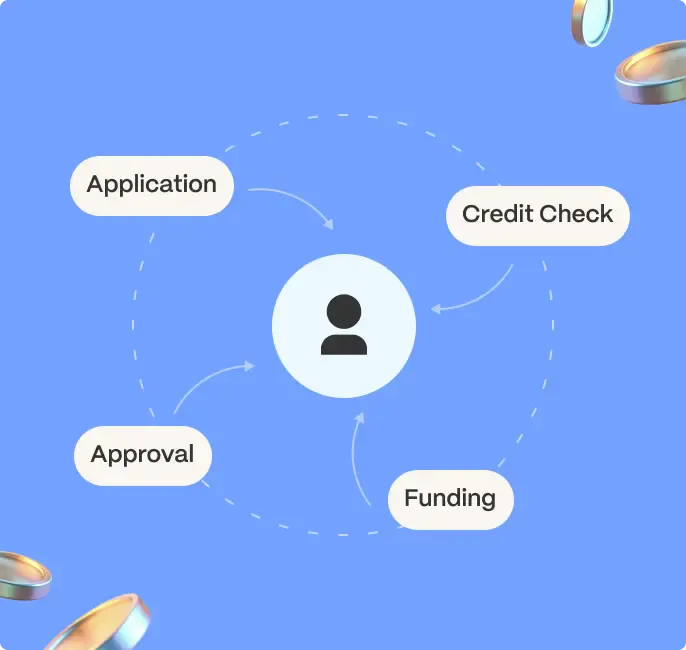

Step-by-Step Loan Application Process

The process moves through six distinct stages, and knowing what happens at each one reduces the chance of surprises along the way:

1. Application Submission

You fill out a form with basic personal and financial information: name, address, employment, income, existing debts, and the amount you want to borrow. Most online applications take under ten minutes. Some lenders offer a soft credit pull at this stage for pre-qualification — this gives you an early read on likely offers without affecting your credit score.

2. Credit Check

Once you submit a formal application, the lender performs a hard inquiry on your credit report. This gives them a detailed view of your borrowing history: payment behavior, current balances, account age, and any negative marks. The hard inquiry itself causes a small, temporary dip in your score. If you’re comparing offers across multiple lenders in a short window, many scoring models treat those inquiries as a single event rather than several separate ones.

3. Underwriting

This is the stage most applicants don’t see but that determines the outcome. An underwriter — sometimes a person, sometimes an automated system — reviews your full financial profile against the lender’s criteria. They’re looking at your credit score, income, debt-to-income ratio, employment stability, and the purpose of the loan. Some lenders complete this in minutes. Others take days.

4. Conditional Approval

Many applicants receive a conditional approval before a final decision. This means the lender is willing to proceed, but needs something first — a recent pay stub, a bank statement, proof of address, or clarification on something in your file. Responding quickly at this stage keeps the process moving. Delays here are one of the most common reasons funding takes longer than expected.

5. Final Approval

Once all conditions are satisfied and documentation verified, the lender issues a final decision. At this point, the loan terms are confirmed: amount, rate, repayment schedule, and any fees. Review everything carefully before signing. The terms set here are binding.

6. Funding

After you sign the loan agreement, the lender initiates the transfer. Timing varies — some lenders fund the same day, others take one to three business days. The speed depends on the lender’s processes, your bank, and whether any last-minute verification is required.

To see how the timeline can compress in practice: someone applies online for a $7,000 debt consolidation loan on a Monday morning, receives a conditional approval by afternoon requesting two months of bank statements, uploads them that evening, and has funds in their account by Wednesday. The whole thing took two days — mostly because they had the documents ready and didn't wait.

What Lenders Evaluate During the Process

Every lender weighs these factors, though the emphasis varies:

- Credit Score. A snapshot of your credit history compressed into a single number. It’s often the first thing a lender looks at. Higher scores generally unlock better rates and broader options. How your credit score works and what goes into it is worth understanding before you apply.

- Income. Lenders want to know you can make the payments. They’ll ask for documentation — pay stubs, tax returns, bank statements — depending on your employment situation.

- DTI. Your monthly debt obligations are divided by your gross monthly income. Most lenders want this below 43–50%. A high DTI signals financial strain even when income looks adequate.

- Credit History. Beyond the score, lenders look at the details: how long you’ve held accounts, whether payments were made on time, and whether there are any serious negative marks like collections or defaults.

- What Lenders May Also Request. Beyond the standard application information, be prepared to provide any of the following: government-issued ID, proof of address, recent bank statements, employer contact information, or explanation letters for gaps in employment or unusual account activity.

Loan Application Timeline: How Long It Takes

There’s no universal answer. Some lenders approve and fund within 24 hours. Others take a week or more. The honest answer is that it depends on the lender, your financial profile, and how quickly you respond to any requests.

Typical timelines break down like this:

| Scenario | Typical timeline |

|---|---|

| Strong profile, online lender, clean documents | Same day to 48 hours |

| Average profile, some documentation needed | 2–5 business days |

| Complex profile, traditional bank, manual review | 1–2 weeks or longer |

What Speeds Things Up

Getting your documents together before you apply makes a big difference. A strong credit profile helps, obviously. Applying through an online lender with automated underwriting also cuts down the clock. And responding quickly when they ask for something — that’s where many people lose days.

What Slows Things Down

Missing or incomplete documents are the number one delay. Manual underwriting takes longer than automated systems. Lower credit scores often trigger extra review, which adds time. And some lenders just have longer internal processes — nothing you did wrong, but it still slows the whole thing down.

Delays are normal and don’t necessarily signal a problem. If you haven’t heard back within the lender’s stated timeframe, following up directly is reasonable.

What Can Delay Your Loan Application

Most delays are avoidable. Here are the common culprits:

1. Missing or Incomplete Documentation

If you don’t provide the documents requested during conditional approval, the process pauses until you respond. Lenders set deadlines (usually 3–7 days). Miss that window and some may close your application.

2. Employment Verification Delays

If you’re self-employed, freelance, or recently changed jobs, the lender may need extra time to verify income. Some employers are slow to respond to verification requests, which is outside your control but can add 3–5 business days.

3. Inconsistencies or Discrepancies

If information on your application doesn’t match your credit report — different address, different income figure, different name spelling — the lender will ask for clarification. Double-checking your application before submitting avoids this.

4. Bank Processing Delays

Even after the lender approves and disburses funds, your bank may take 1–2 business days to process the deposit. Weekends and holidays add time too.

If your approval is taking longer than expected, it doesn’t mean you’ll be denied. Delays are normal and usually mean the lender is being thorough. Don’t hesitate to contact them (or the marketplace platform) if you haven’t heard anything in 3–5 business days.

What Happens After You Apply

Submitting an application doesn’t guarantee a decision comes back immediately or that the first response is a final one. A few things commonly happen after you apply:

You May Receive Multiple Offers

Through a marketplace like Pennie Financial, a single application routes to several lending partners. Each returns its own offer independently. You compare them and choose — or decline all of them.

You May receive a Conditional Approval

This is not a final yes. It means the lender is interested but needs more information before committing. A typical conditional approval might read: “We’re prepared to offer you $8,000 at 13.5% APR, pending verification of your most recent two months of income.” Once you provide what’s requested and it checks out, the offer becomes final.

You may be asked for additional documentation at any point before final approval. This is standard procedure, not a warning sign.

How to Improve Your Chances Before Applying

Preparation matters more than most applicants realize. A few things worth doing before you submit:

1. Check Your Credit Before the Lender Does

Reviewing your credit score and report in advance lets you spot errors, understand where you stand, and set realistic expectations about the rates you’re likely to see. If the number isn't where you’d like it to be, our guide on how to improve your credit score covers the most practical ways to move it before you apply.

2. Know Your Numbers

Calculate your DTI before applying. If it’s high, paying down existing balances before submitting can meaningfully improve your profile. Understanding what lenders typically require helps you anticipate what they’ll ask for.

3. Compare Options Rather Than Committing To the First Offer

Rates and terms vary significantly across lenders. Seeing multiple offers side by side — through a marketplace or by applying to several lenders within a short window — gives you a better basis for deciding. How to get approved for a loan covers preparation strategies in more detail.

4. Have Documentation Ready

Pay stubs, tax returns, bank statements, and ID. Having these on hand before you apply eliminates one of the most common sources of delay.

When You May Get Approved vs Denied

Approval depends on how your financial profile aligns with a specific lender’s criteria. There’s no universal threshold. A borrower with a 610 score and strong income might be approved by one lender and denied by another. A high DTI might disqualify you with one institution and be acceptable to another.

Denial is common and not final. A rejection from one lender doesn’t reflect every lender’s position. Different lenders serve different borrower profiles, and a marketplace gives you access to several at once rather than going through them one by one.

If you’re denied, the lender is required to provide an adverse action notice explaining the primary reasons. That information is useful — it tells you exactly what to address before applying again. How long it takes to get a personal loan and what affects that timeline is covered in more detail separately.

Where Pennie Financial Fits

Pennie Financial is a lending marketplace. When you submit a single application, it’s reviewed by multiple lending partners simultaneously. Each partner evaluates your profile independently and returns its own offer — or declines. Pennie doesn’t make approval decisions, set rates, or issue loans directly.

What the platform does is give you a range of real offers to compare without submitting multiple separate applications. The initial pre-qualification uses a soft credit pull, which doesn't affect your score. From there, you choose an offer, the lender conducts final underwriting, and the process moves toward funding. Learn more about how the process works or explore available personal loan options.

Final Thoughts

The loan application process is structured, but it isn’t uniform. Every lender runs their own version of it, weighs factors differently, and moves at their own pace. What stays consistent is the sequence: application, credit check, underwriting, conditional approval, final approval, funding. Knowing what happens at each stage, what lenders are looking for, and what can slow things down puts you in a better position to navigate it — and reduces the chance that something unexpected derails the timeline.

Frequently Asked Questions

What are the main steps in the loan application process?

Through a traditional lender, the steps are: application, credit check (hard pull), underwriting, conditional approval, final approval, and funding. Through a lending marketplace you submit one application with a soft credit pull, receive pre-approved and pre-qualified offers from multiple lenders, choose the best one, and then the lender handles final approval and funding.

How long does the loan application process take?

Through a marketplace you see offers instantly after applying. Final lender approval can happen the same day, with funding as soon as the next business day. Traditional direct lender applications typically take 3–7 business days per lender — and if you’re denied and need to reapply elsewhere, the process starts over.

Does applying for a loan hurt my credit score?

It depends on how you apply. Traditional direct lender applications trigger a hard inquiry, which can lower your score by a few points. Lending marketplaces use a soft credit pull at the application stage, which has no impact on your score.

What do lenders look at besides credit score?

Income, employment stability, DTI, credit history patterns, and sometimes alternative data like rent payment history or bank account activity. Income is often the most important factor, especially for lenders who specialize in lower-credit or thin-file borrowers.

Can I get a personal loan with bad credit or no credit history?

Yes. Many lenders specialize in working with borrowers who have lower credit scores, thin files, or no traditional credit history. A marketplace hosts one of the largest lending networks for these borrowers in the U.S. — there are more options available than most people expect, especially for borrowers with steady income.

What is the difference between a lending marketplace and a direct lender?

A direct lender (bank, credit union, online lender) evaluates and funds your loan themselves. A lending marketplace connects you with multiple lenders through a single application, showing you pre-approved offers so you can compare before committing.

What happens after I accept an offer through a marketplace?

The lender you selected handles the final approval process — this includes a hard credit pull, verification of your income and employment, and any additional documentation they need. Once everything checks out, you sign loan documents and the lender funds the loan, often as soon as the next business day.

Can I get same-day funding for a personal loan?

Through Pennie, you see offers instantly and lender approval can happen the same day you accept an offer. Funding is typically as soon as the next business day after final approval. Some lenders may fund even faster depending on their process and how quickly documents are verified.

Get loan offers in as little as 60 seconds

You deserve options. So we built an industry leading platform to compete for your business.

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years

Your info is never sold