Exploring your options for a personal loan based on income? Pennie Financial connects you with multiple lenders whose underwriting models weight income — so you can compare real offers based on your actual financial profile. This content is for informational purposes only and does not constitute a loan offer or guarantee of approval. Terms, rates, and eligibility vary by lender.

Find the help you need for any problem

Topics

Personal loans

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

Ready to move forward?Get started

Income-Based Loans Explained: Can You Get Approved Without Good Credit?

Not everyone walks into a loan application with a clean credit history. Income-based loans are designed to fill exactly that gap. Lenders using this approach consider your paycheck, your employment history, and the debt you already carry. What you earn today and how reliably you earn it — that’s what drives the decision.

An income-based loan is one where the lender evaluates your earnings and debt load as the primary approval factors, rather than your credit score. The term covers both how lenders qualify borrowers and how repayments are structured.

This guide covers how income-based lending works, what loan types use this approach, who it’s built for, and how to find the right option without settling for the first one you find.

In this article:

- What Is an Income-Based Loan?

- How Income-Based Loans Work

- Types of Income-Based Loans

- Key Benefits of Income-Based Loans

- Potential Drawbacks of Income-Based Loans

- Who Might Consider Income-Based Loans

- How to Evaluate Income-Based Loan Options

- Frequently Asked Questions

What Is an Income-Based Loan?

An income-based loan is a lending arrangement where your income does the heavy lifting. Instead of filtering applicants by credit score, the lender focuses on what you earn, how consistently you earn it, and whether your existing obligations leave room for a new payment.

In traditional lending, a credit score drives the decision. A lender reviews your payment history, credit utilization, and length of credit history to assess risk. Income-based lending shifts that calculus.

Two distinct concepts live under this label:

1. Qualification-Based

Income is the dominant approval factor. Borrowers with limited or damaged credit may still qualify if their income is sufficient and their existing debt is manageable. The lender may still pull credit — but a thin or imperfect file doesn’t automatically end the conversation.

2. Repayment-Based

The monthly payment is calculated as a percentage of your discretionary income rather than a fixed amount. This structure is most common in federal student loan income-driven repayment plans, but the income-first philosophy carries into personal lending as well.

What Lenders Typically Evaluate in Income-Based Approval

Income-based approval isn’t a gut call. Lenders run a structured evaluation of your financial picture before making a decision. Five factors consistently show up across lenders who use this approach:

- Gross monthly income and income source type (W-2, self-employed, benefits)

- Employment stability and tenure

- Debt-to-income ratio (DTI)

- Consistency — is the income predictable month-to-month?

- Existing financial obligations and how they interact with a new payment

How Income-Based Loans Work

Income verification is the backbone of this entire process. Each element below — from your pay stubs to your employment timeline — feeds directly into how a lender evaluates your application.

How Lenders Verify Income

Pay stubs (typically the last 2–3 months), bank statements showing regular deposits, W-2s or tax returns, employer verification letters, benefit award letters for Social Security or disability recipients, and 1099s or profit-and-loss statements for self-employed borrowers.

Why Employment History Matters

A paycheck from last month is useful. A consistent employment track record spanning years is what lenders actually want to see. Frequent job changes or income gaps raise the question of whether your earnings will hold through the full repayment term.

The DTI Calculation

Your debt-to-income ratio is your total monthly debt payments divided by your gross monthly income. If you earn $4,500/month and your existing minimums (rent, car, credit cards) total $1,575, your DTI is 35%. Many lenders prefer a DTI below 43% before adding a new loan payment.

How Income Shapes Your Terms

Your earnings don’t just determine whether you get approved. They influence how much you can borrow, the repayment period you qualify for, and sometimes the rate. A tight DTI caps the loan amount regardless of gross income.

A Real-Life Scenario

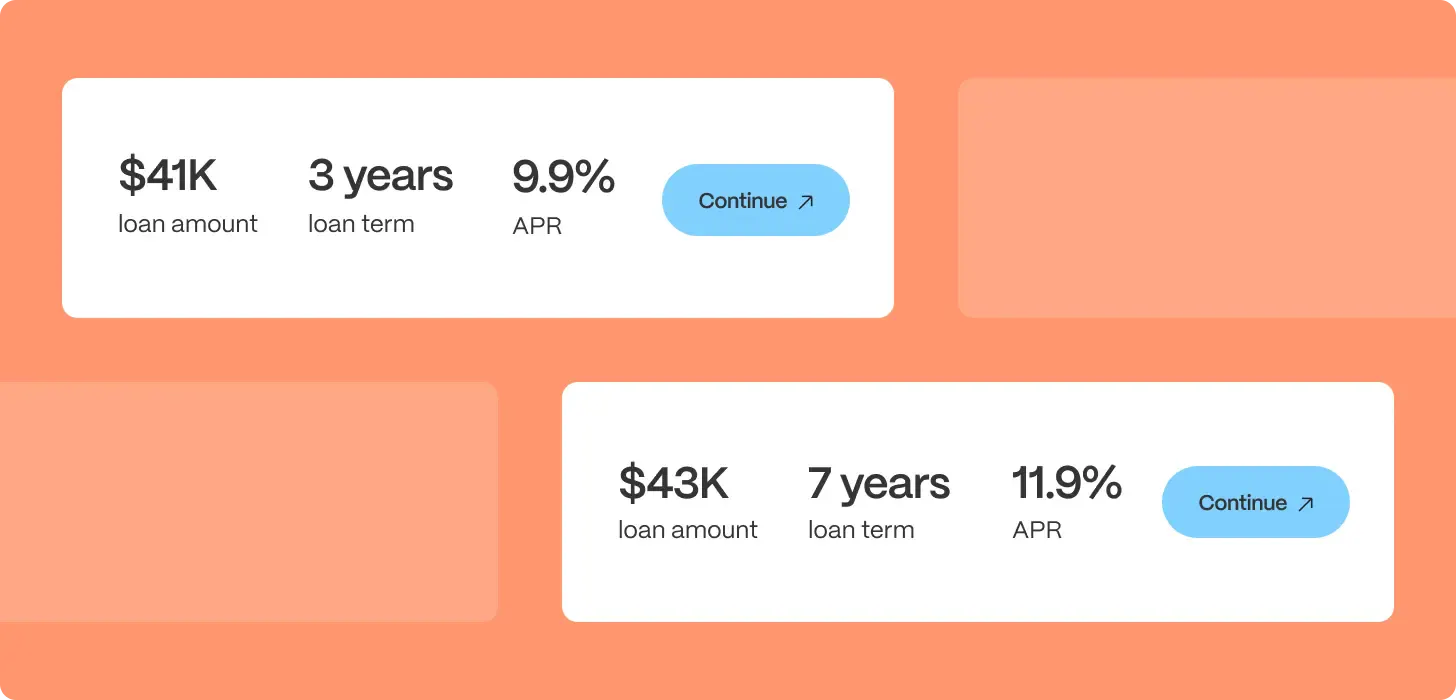

Numbers make more sense with a real example behind them. Take a 31-year-old operations manager: four years at the same employer, $8,400 in monthly gross income, $2,700 in existing debt obligations, a DTI of 32%, and a credit score of 631. A traditional bank stops at that score. An income-focused lender sees four years of stable employment and a DTI with room to absorb an additional payment. A $20,000–$30,000 loan over a structured term is a realistic outcome for this profile.

Types of Income-Based Loans

Income-based qualification shows up across several loan categories, and the differences between them are significant. The right fit depends on what you need and what you can qualify for.

Personal Loans

Personal loans are the most accessible income-based option for most borrowers, available through online lenders, credit unions, and marketplace networks. Loan amounts can reach up to $250,000, with rates ranging from 5.99% to 36% depending on your income profile and the lender. It’s also worth understanding how personal loans affect your credit score before you apply.

Credit Union Loans

Many credit unions offer personal loans to members where income is a primary qualification factor and credit history plays a secondary role. Rates are generally reasonable — often in the 12–18% APR range — and repayment terms are structured for actual payoff. Membership is required.

Payday Alternative Loans (PALs)

Offered by federal credit unions and regulated by the NCUA, PALs are designed for smaller, short-term borrowing needs. Loan amounts run $200–$2,000, repayment terms are 1–12 months, and the APR is capped at 28%. If you need a small amount fast and qualify as a credit union member, a PAL is one of the more affordable short-term options available.

Peer-to-Peer Lending Platforms

P2P platforms connect borrowers directly with individual investors and often use broader underwriting criteria than traditional banks. Many weigh income and cash flow alongside credit, making them accessible to borrowers within the fair credit category.

Key Benefits of Income-Based Loans

Income-based lending solves a specific problem: good financial standing that a credit score doesn’t fully capture. These are the practical advantages that make it worth considering.

A Path in When Credit Closes the Door

If your credit score is in the 500s or your file is thin, income-based approval gives you options that traditional underwriting doesn’t. A solid paycheck and a manageable debt load can carry an application that a score-first lender would reject outright.

Recent Stability Counts for Something

Traditional credit scoring is backward-looking by design. Income-based lending puts more weight on the present. If you’ve had credit problems in the past but your financial situation has genuinely improved, income-focused lenders are more likely to see that than a score that still reflects old history.

Access to Meaningful Loan Amounts

This isn’t a small-dollar workaround. Income-based personal loans through marketplace networks can reach $250,000 for qualified borrowers. The ceiling is set by income and DTI.

Faster Decisions

Verifying income is more straightforward than a full credit analysis. Many online lenders and marketplace platforms can turn around decisions within hours. That speed matters when you’re dealing with a time-sensitive expense.

Better Rates Through Comparison

No single lender has the best rate for every income profile. Marketplace networks let you see multiple offers side by side. The difference across offers for the same borrower can be several percentage points.

Potential Drawbacks of Income-Based Loans

Flexible qualification comes with tradeoffs. Understanding them upfront is what separates a smart borrowing decision from an expensive one.

Higher Interest Rates for Lower Credit Profiles

Lenders taking on more risk price the loan accordingly. Rates vary by income, DTI, employment history, and credit profile. Comparing multiple offers is the only way to know if you’re getting the best available rate for your situation.

Shorter Repayment Terms on Some Products

Small-dollar income-based loans are often structured for repayment in months. A shorter term keeps total interest costs low but raises the monthly payment.

Fees That Change the Actual Cost

Origination fees, late fees, and prepayment penalties vary widely across lenders. Some build fee structures that push the effective cost well above the stated rate. Always calculate total repayment cost.

Income Instability Risk

An income-based loan is underwritten on the assumption that your income holds. Job loss, a pay cut, or variable gig income changes the math entirely.

Who Might Consider Income-Based Loans

Income-based lending serves borrowers that traditional underwriting tends to misread. The profiles below are where it makes the most practical sense.

Borrowers With a Steady Income But a Thin Credit File

Young professionals, recent immigrants, or anyone who hasn’t yet built a credit history aren’t necessarily risky borrowers — they just don’t have much on their record. Income-based lending focuses on whether you can repay what you’re asking to borrow.

People Rebuilding After Credit Setbacks

A bankruptcy, missed payments, or high utilization can leave a score that no longer reflects your actual financial position. If the problems are in the past and the income is stable now, income-focused lenders are more likely to weigh the present over the past.

Borrowers Who Need More Than Small-Dollar Access

PALs and credit union products work for small, short-term needs. For $10,000, $25,000, or more, income-based personal loans through a marketplace network are where that capacity exists. Comparing income-based personal loans across a network gives you a realistic picture of what’s available at your income and debt level.

Borrowers Who’ve Been Turned Down Elsewhere

A “no” from a bank isn’t the final word. If your DTI is healthy and your employment history is solid, an income-focused lender may reach a different conclusion. For borrowers with no credit at all, there are personal loans for thin credit profiles worth knowing about before moving to higher-cost alternatives.

How to Evaluate Income-Based Loan Options

The range from “well-structured personal loan with flexible underwriting” to “expensive short-term product” is wide in this space. Here’s how to tell the difference before you commit.

Compare APR, Not Just Rate

The annual percentage rate includes fees. A lender advertising a low rate with heavy origination fees can end up more expensive than a competitor with a higher stated rate and no fees. APR is the number that actually lets you compare across offers.

Calculate Total Repayment Cost

Multiply your monthly payment by the number of payments. Subtract the principal. That number is what you’re paying to borrow. It’s often more clarifying than the monthly payment figure alone.

Know the Repayment Structure

Fixed monthly payments over a set term mean you know exactly what you owe each month and for how long. Repayment structure matters more than most borrowers realize — a personal loan vs line of credit comparison shows how differently they handle repayment, and choosing the wrong one for your borrowing needs is a costly mistake.

Verify the Lender

Check the CFPB complaint database and your state’s financial regulator. Legitimate lenders are licensed. If you can’t verify a lender’s license in your state, that’s a reason to stop.

Use a Network, Not Just One Lender

Applying to one lender and accepting whatever rate comes back is the most expensive mistake income-based borrowers make. A platform like Pennie Financial connects you to multiple lenders whose underwriting models emphasize income. Take a look at how Pennie connects borrowers with lenders before submitting your first full application.

Lender Evaluation Checklist

Not every lender in this space plays by the same rules. Use this as your baseline before signing anything:

- APR clearly disclosed

- Total repayment cost calculated (payments × term, minus principal)

- Repayment structure is fully understood

- No prepayment penalty

- No upfront fees required before funding

- Income verification requirements are clear

Frequently Asked Questions

Who qualifies for income-based repayment programs?

It depends on the program. For personal income-based loans, qualification generally requires verifiable income, an active bank account, and meeting a lender’s minimum income and DTI thresholds.

Can I get a loan based only on my income?

Most lenders still review some credit data. What changes is how much weight that data carries.

Do income-based loans have higher interest rates?

Not necessarily. Rates across marketplace lenders can vary widely — some lenders in these networks advertise starting rates as low as 5.99%.

Are income-based loans only for student loans?

No. The term is widely associated with federal student loan income-driven repayment plans, which is where most people first encounter it.

Do income-based loans reduce the total amount you repay?

Not automatically. For federal student loan income-driven repayment, remaining balances can be forgiven after 20–25 years of qualifying payments — but that’s a program-specific feature.

What’s the difference between income-based personal loans and loans based on income only?

Income-based personal loans use your earnings as the primary approval factor, but may still review credit as a secondary signal. Income-based personal loans through marketplace networks tend to offer better rates, higher loan amounts, and more structured terms.

Share

Ready to move forward?Get started

Get loan offers in as little as 60 seconds

You deserve options. So we built an industry leading platform to compete for your business.

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years

Your info is never sold