Find the help you need for any problem

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

Personal Loans for Non-US Citizens: Requirements, Options, and What to Expect

You’ve been in the U.S. for a while, you have a steady job, but you still get that sinking feeling when a lender asks for your citizenship status. Yes, non‑U.S. citizens can get personal loans in America. But the options are often narrower than what’s available to citizens, the requirements tend to be tighter, and the rates can be higher. That’s the honest starting point.

What really matters isn’t your passport — it’s your residency status, your U.S. credit history, and how cleanly you can document your income. Some lenders serve permanent residents and visa holders without much fuss. Others specialize in ITIN filers who file taxes but don’t have a Social Security number. This guide explains what lenders look for, which options exist for each status, and how to improve your chances before you apply.

In this article:

- Can non-US citizens get a personal loan in the U.S.?

- Who qualifies as a non-US citizen borrower

- Basic requirements for non-US citizens

- Do you need an SSN or can you use an ITIN?

- What lenders look for (beyond citizenship status)

- Challenges non-US citizens may face

- Loan options available for non-US citizens

- Example scenarios — how approval may vary

- How to improve your chances of approval

- Alternatives if you can't qualify

- Where Pennie Financial fits

- Final takeaway

- Frequently Asked Questions

Can non-US citizens get a personal loan in the U.S.?

Short answer: yes, with limitations. Citizenship itself is rarely a deal-breaker, but it’s one input into a larger risk picture. Lenders want to see a paper trail — consistent U.S. residency, documented income, a credit file they can evaluate — that gives them confidence the loan will be repaid.

Borrowers with strong documentation and stable profiles find the market. Borrowers with short U.S. histories, irregular income, or limited documentation often face declines or meaningfully worse terms.

The variability is the main point. One lender may decline an applicant, another lender would approve, because each weighs residency, credit depth, and income stability differently.

Who qualifies as a non-US citizen borrower

Lenders don’t treat all non‑citizens the same. Your residency status shapes which lenders will even look at your application, how much documentation you’ll need, and what rates you might see. The main categories break down into three practical groups:

Visa holders

H‑1B, L‑1, O‑1, and other employment or study visas are accepted by many online lenders and some banks. Policies vary widely — some lenders want to see at least two or three years remaining on your visa before they’ll approve a longer loan term. Strong income and a clean U.S. credit file make a bigger difference here than the visa type itself.

Permanent residents

Green card holders are treated almost identically to U.S. citizens by most lenders. You have documented residency, straightforward employment authorization, and typically build credit the same way a citizen would. The process and rates usually reflect your credit profile, not your status. If you’re still figuring out which product fits your situation, our guide on the types of personal loans walks through all the options.

ITIN users

If you file taxes with an Individual Taxpayer Identification Number instead of an SSN, your options are narrower but real. ITIN‑focused lenders specialize in this category and use tax returns, bank statements, and utility histories in place of a traditional credit file. Rates may run higher, but approval is possible without an SSN.

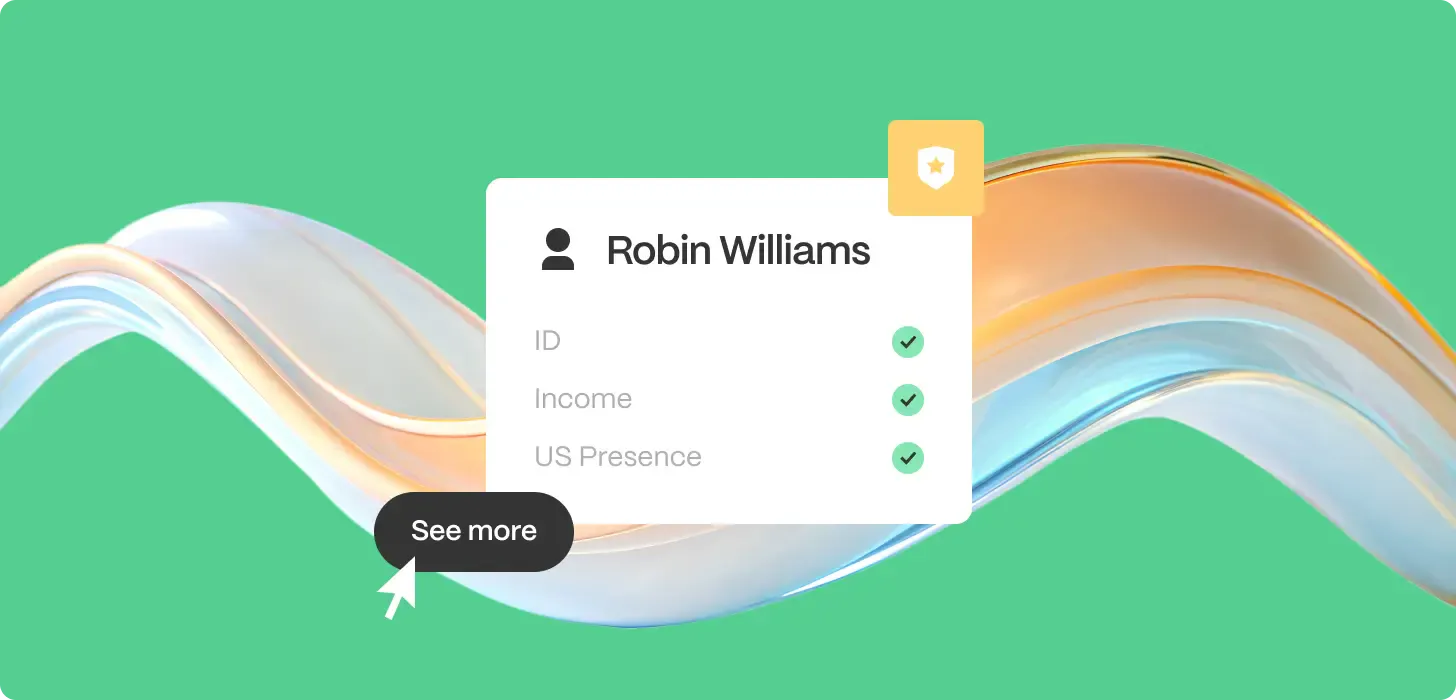

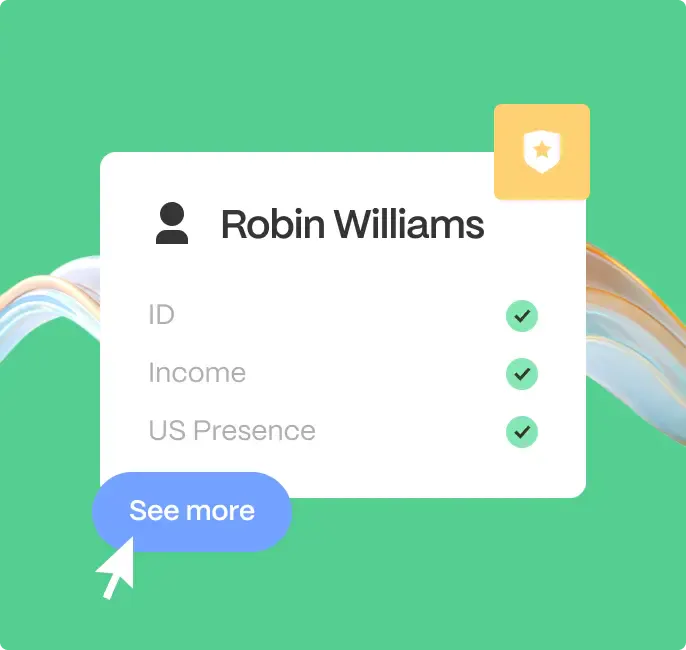

Basic requirements for non-US citizens

Lenders ask for the same few things from almost every non‑citizen applicant. They’re not trying to make the process harder — each requirement reduces a specific kind of risk. Here’s what they typically want and why:

ID

A passport, visa, or green card proves who you are and that you’re in the country legally. Without a solid ID, a lender can’t verify your identity or check whether you’re authorized to be here. That’s a non‑starter for any regulated financial institution.

Income

Recent pay stubs, tax returns, or an employment letter show that you earn enough to cover the loan payment. Stable, documentable income is often the single most important factor, especially when your credit history is still thin. Lenders want to see that you won’t struggle to repay.

US presence

A lease, utility bill, or bank statement in your name at a U.S. address tells the lender you have roots here. Consistent address history and an active bank account reduce the risk that you’ll disappear with the money. The longer you’ve been in one place, the better you look on paper.

Do you need an SSN or can you use an ITIN?

This is the most common point of confusion. Some lenders require a Social Security number; others accept an ITIN. The difference isn’t just paperwork — it also shapes what kind of credit file a lender can see.

The differences show up in three main ways:

- SSN-based loans pull a traditional credit report from the major bureaus. Lenders have full underwriting visibility and offer the broadest range of products and rates.

- ITIN-based loans exist but are more limited. Fewer lenders participate, underwriting often leans on alternative data (tax returns, bank statement flow, rent history), and rates may be higher to offset the narrower file.

- Dual-option lenders accept both and sometimes use a borrower’s stronger documentation to balance out a less developed credit file.

If you only have an ITIN, your pool of lenders is smaller but not empty. Specialty lenders, credit unions with immigrant-focused programs, and some community development financial institutions (CDFIs) actively serve ITIN borrowers.

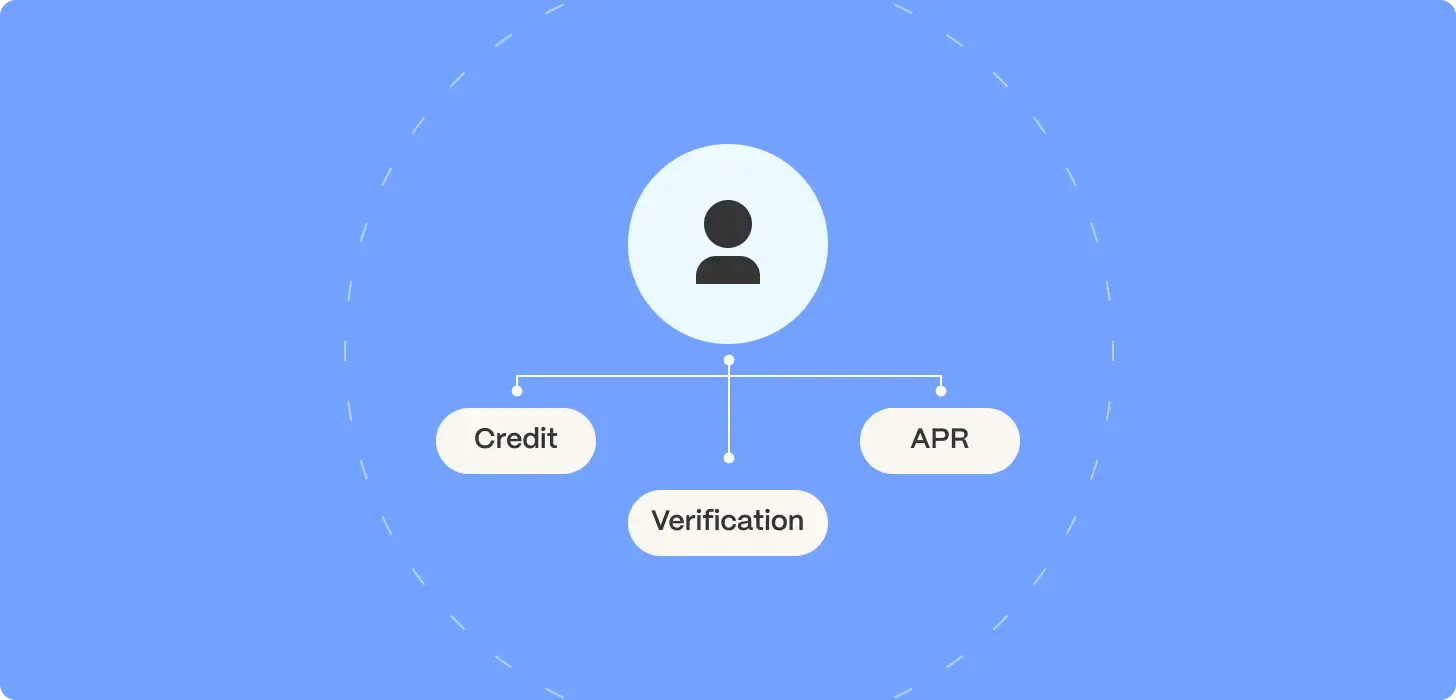

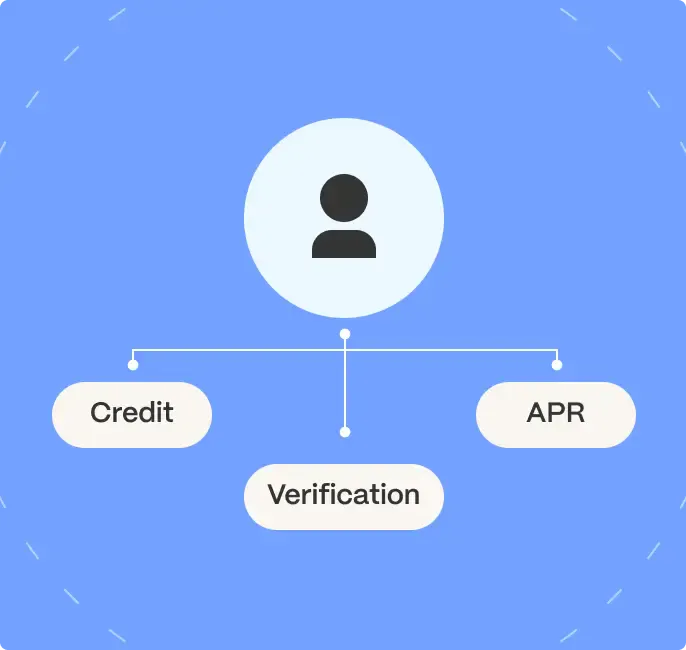

What lenders look for (beyond citizenship status)

For most personal loan applications, citizenship status is a gate to pass through. Once you’re past the gate, the same factors matter for you as for any applicant. Three factors carry the most weight:

Income stability

A steady income, documented clearly, is often the single most important factor — especially for borrowers whose credit file is thin. W-2 income with recent pay stubs is the easiest to verify; self-employment income requires tax returns and bank statements. For borrowers whose income is the strongest part of their profile, our guide on income-based loans is worth a read.

Employment

Length of current employment and industry stability both matter. A long tenure or a recent job in a sector with strong demand both work in the applicant’s favor.

Credit history in the U.S

The depth of your U.S. credit file matters a lot. Someone with two years of clean credit cards and an on-time auto loan will look different to underwriting than someone who just opened their first U.S. account last month, even if both are equally creditworthy by any reasonable measure.

These factors often matter more than citizenship itself. Strong performance on them can offset lender hesitation around status; weakness in them can’t be overcome by citizenship alone. The full picture of what goes into that evaluation is in our article on how to get approved for a loan and what lenders look for.

Challenges non-US citizens may face

Real barriers exist, and it’s worth naming them clearly so you can plan around them. Here are the three biggest hurdles non‑citizen applicants run into:

Limited credit history

Most newer U.S. residents have a thin file — not because their creditworthiness is poor, but because they haven’t had time to build visibility. This is the single most common obstacle to approval. Once your file starts building, our article on what credit score you need for a personal loan gives you a concrete target to aim for.

Stricter documentation requirements

Lenders often ask non-citizen applicants for more documents than they’d ask a citizen applicant. Visa, proof of residency, extended income documentation — all reasonable, but it’s more work and can slow the process.

Higher APR in some cases

If your file is thin or your status adds perceived risk, some lenders will price a higher rate to compensate. That’s not universal — a strong applicant with solid credit can still get competitive rates — but it’s a pattern to expect on the thin-file end of the spectrum.

A few real‑life situations show the range. An H‑1B visa holder with two years of U.S. work history and a clean credit card record likely clears the hurdles. A green card holder with five years of stable employment faces almost the same process as a U.S. citizen. An ITIN filer with filed taxes and consistent bank deposits may get approved, but with stricter documentation and a higher rate.

Loan options available for non-US citizens

Lender policies vary with your residency status. Some doors open easily; others stay shut. Let’s walk through the practical categories:

1. Traditional bank and credit union personal loans.

Many accept permanent residents; some accept visa holders; fewer accept ITINs. Credit unions with immigrant-focused programs can be a strong fit.

2. Online lenders.

Some specialize in newer arrivals and international students, using alternative data to underwrite. Others only accept applicants with SSNs and established U.S. credit.

3. Specialty ITIN lenders and CDFIs.

Focused specifically on serving ITIN filers and mixed-status households. Application flows are often built around alternative documentation.

4. Secured loans

Backing a personal loan with savings, a CD, or a vehicle can open doors that an unsecured application wouldn’t. Collateral reduces the lender’s risk and often makes citizenship status less of a barrier. If unsecured is still your preferred route, our guide on unsecured personal loans, rates, requirements, and risks lays out exactly what to expect.

If you want a broader market view, our guide on the best personal loans breaks down what's out there.

Example scenarios — how approval may vary

Your residency status and credit history don’t just change which lenders will talk to you — they shift approval amounts, rates, and the size of the lender pool. Watch how:

An H-1B visa holder with three years of U.S. employment, a clean credit file, and recent pay stubs applies for a $15,000 unsecured personal loan. Most online lenders and many banks approve the application at competitive rates.

A green card holder of five years with a full credit file and stable income applies for the same $15,000 loan. Treated essentially identically to a citizen applicant; approval and rates reflect their credit profile, not their residency status.

An ITIN filer with two years of filed taxes, consistent bank statement deposits, and no U.S. credit history applies for $8,000. The pool of lenders is smaller, rates are higher, and amounts are typically capped lower than they’d be for an SSN borrower — but approval is possible through ITIN-focused lenders and some credit unions. If your credit profile is still developing, our guide on the best personal loans for fair credit covers lenders worth considering.

How to improve your chances of approval

Small moves before you apply can shift the odds. None of them guarantees a yes, but each removes a reason for a lender to say no. A checklist to work through:

- Start building U.S. credit early. A secured credit card used responsibly creates a file lenders can see.

- Keep your address, employer, and bank account stable. Consistency lowers perceived risk.

- Gather full documentation before you apply: visa or green card, pay stubs, bank statements, tax returns if self‑employed.

- Match yourself to lenders that serve your status. Applying to generic mass‑market lenders wastes time.

- Consider a secured loan or a co‑signer if unsecured options are limited.

For a full picture of what happens after you hit submit, our step-by-step guide on the loan application process walks you through every stage.

Alternatives if you can’t qualify

If an unsecured personal loan isn’t available to you yet, a few options can fill the gap or build toward eligibility. The most practical fallbacks break down into these categories:

Secured credit products

A secured credit card or secured personal loan backed by cash collateral is often available to borrowers whose status or credit file makes them ineligible for unsecured products. Using them responsibly builds a credit history that broadens future options.

Co-signers

A U.S. citizen or permanent resident with strong credit can sometimes co-sign a personal loan with you, opening approval that wouldn’t be available on your own. The co-signer takes on full legal responsibility, so this is a significant task.

Credit-builder loans

Small loans held in a locked account while you make payments. The payments report to the credit bureaus; the loan proceeds release at the end. A slow route, but a real one.

Waiting and building

If your U.S. history is very short, giving it six to twelve more months while using a credit card responsibly can meaningfully change which lenders will approve you.

Where Pennie Financial Fits

Finding a lender that actually works with your status is half the battle. Pennie Financial cuts that part short — the platform matches you with lending partners whose criteria align with your profile, so you're comparing real personal loan offers rather than collecting declines. Eligibility depends on each lender's own criteria — Pennie narrows the field, lenders make the call. If you want to understand the mechanics first, read how Pennie works.

Final takeaway

Personal loans are available to non-US citizens, but the path is more documentation-heavy and lender-specific than it is for citizens. Permanent residents face few additional hurdles; visa holders often find strong options with the right lender; ITIN borrowers have a smaller but real market.

The deciding factors are usually not citizenship itself but the things that sit underneath it — income stability, credit history depth, and documentation completeness. Setting realistic expectations about rate and amount, matching yourself to lenders that serve your profile, and bringing a complete application are the levers that matter most.

Frequently Asked Questions

Can non-US citizens get a personal loan in the U.S.?

Yes. Permanent residents, many visa holders, and ITIN filers all have options, though the lender pool and terms vary by status.

Can you get a personal loan without an SSN?

Yes, with an ITIN. The lender pool is smaller and terms may differ from SSN-based loans, but specialty lenders, credit unions, and community development financial institutions actively serve ITIN borrowers.

What is an ITIN loan?

A personal loan underwritten using an Individual Taxpayer Identification Number instead of a Social Security number.

Do visa holders qualify for personal loans?

Often yes, particularly H-1B, L-1, and similar employment visa holders. Lender policies vary on visa categories and on how much visa validity needs to remain.

Why is it harder for non-US citizens to get approved?

Usually because credit files are thinner, not because status itself is a disqualifier. Lenders rely heavily on U.S. credit history to evaluate risk, and newer residents simply haven’t had time to build one.

Can a co-signer improve approval chances?

Yes. A U.S. citizen or permanent resident co-signer with strong credit can substantially improve approval odds and may lower the offered rate. The co-signer takes on full legal liability, so it’s a significant commitment on their side.

What documents do non-US citizens usually need to apply?

Typically: government-issued ID (passport, visa, green card), proof of U.S. address, proof of income (pay stubs, employment letter, or tax returns), a U.S. bank account, and either an SSN or ITIN.

Get loan offers in as little as 60 seconds

You deserve options. So we built an industry leading platform to compete for your business.

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years

Your info is never sold