Find the help you need for any problem

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

HELOC vs Personal Loan: What's the Difference and Which Is Better?

A HELOC and a personal loan are two different ways to borrow money. The biggest difference comes down to collateral. A HELOC is secured by your home — you’re borrowing against the equity you’ve built. A personal loan is typically unsecured, so no property is at stake if you default. That single difference drives almost everything else: interest rates, flexibility, approval speed, and risk. But herу’s the catch: neither option is universally better.

A HELOC might save you money on interest but puts your home on the line. A personal loan costs more but keeps your house out of the equation. Which one works for you depends on your situation, how much risk you can tolerate, and what you’re trying to achieve financially. This guide breaks down how each product works, their pros and cons, and when one makes more sense than the other.

In this article:

- HELOC vs Personal Loan: Key Differences

- What Is a HELOC?

- What Is a Personal Loan?

- Pros and Cons of a HELOC

- Pros and Cons of a Personal Loan

- HELOC vs Personal Loan: Which Is Better?

- When a HELOC May Make Sense

- When a Personal Loan May Make Sense

- Other Options to Consider

- Risks and Considerations

- Where Pennie Financial Fits

- Final Thoughts

- Frequently Asked Questions

HELOC vs Personal Loan: Key Differences

Before getting into the details, it helps to see how these two borrowing options line up. The table highlights the main differences — from how each loan is structured to the risks involved.

| Aspect | HELOC | Personal Loan |

|---|---|---|

| Structure | Revolving line of credit secured by your home's equity | Lump-sum unsecured (usually) installment loan |

| Collateral | Your home equity backs the loan | No collateral required (personal creditworthiness) |

| Interest Rates | Variable (tied to prime rate, subject to change) | Fixed (stays the same for life of loan) |

| Repayment | Draw as needed during draw period; interest-only or principal + interest during repayment period | Lump sum upfront; fixed payments over set term (typically 2–7 years) |

| Flexibility | Borrow, repay, borrow again — like a credit card | Borrow once; repay in installments; can't reborrow without reapplying |

| Risk | Risk of foreclosure if you default; home equity fluctuates with market | Risk of debt collection and credit damage, but not foreclosure |

| Speed | Slower approval (requires home appraisal and equity verification) | Faster approval (often within 24–48 hours) |

What Is a HELOC?

A HELOC is a revolving line of credit backed by the equity in your home. Say you own a home worth $300,000 with a $200,000 mortgage. You have $100,000 in equity. A lender might let you borrow against some or all of it.

Once approved, you get a credit limit—say $75,000. You can draw from it as needed: $5,000 one month, $20,000 the next, nothing for three months. You only pay interest on what you actually borrow. It works like a credit card tied to your home.

HELOCs have two phases:

- Draw period (typically 5–10 years): You can withdraw funds. You may pay just interest, keeping payments low.

- Repayment period (typically 10–20 years): You can’t draw anymore. You repay what you borrowed plus interest.

The tradeoff: interest rates on HELOCs are variable. They move with the prime rate. If rates rise, your payment rises. That unpredictability makes budgeting harder.

What Is a Personal Loan?

A personal loan is a fixed-amount installment loan. You apply, get approved for a specific amount (say $25,000), and receive the full sum upfront. Then you repay it in equal monthly installments over a set period, typically 24 to 84 months.

Most personal loans are unsecured. The lender has no collateral to seize if you default. Your promise to repay and your credit history are the security. Because the lender takes on more risk, personal loans typically carry higher rates than HELOCs.

The payoff: your interest rate is fixed. Your monthly payment never changes (barring loan modifications). You know exactly what you owe and when you’ll be done. That certainty is a major advantage.

Pros and Cons of a HELOC

A HELOC offers clear advantages if you have home equity and need flexible access to cash. But those benefits come with real risks — some of which are easy to overlook. Below is a breakdown of what works in favor of a HELOC and what should give you pause.

Pros

Lower interest rates. HELOCs often run 1–3% lower than personal loans because your home backs the loan.

Flexibility. You borrow what you need, when you need it. Unused credit costs nothing.

Large borrowing capacity. You can access tens of thousands of dollars, limited only by your equity.

Potential tax deductibility. If you use HELOC money for home improvement, the interest may be tax-deductible (check with a tax pro).

Interest-only payments. During the draw period, some HELOCs let you pay just interest, lowering upfront costs.

Cons

Variable interest rates. Your rate can increase, raising your monthly payment — sometimes substantially.

Risk of foreclosure. Default on a HELOC and you could lose your home. This isn’t theoretical. During the 2008 crisis, many homeowners with HELOCs lost their homes when they couldn’t repay.

Longer approval process. HELOCs require a home appraisal, equity verification, and underwriting. Expect 2–4 weeks.

Equity requirement. You need sufficient equity to qualify. Declining home values or negative equity disqualify you.

It’s easy to borrow too much. The revolving structure tempts you to keep drawing. You can easily end up borrowing more than you should.

Rate cap complexity. Even with caps, rates can jump when caps reset or during inflation.

Pros and Cons of a Personal Loan

A personal loan is simpler and faster than a HELOC, with no collateral required. But that convenience comes at a cost — typically higher rates and less flexibility. Below is a look at what makes personal loans attractive and where they fall short.

Pros

Fixed interest rate. Your rate and payment are locked in. No surprises when rates rise.

No collateral required. Your home (or other assets) stays protected.

Faster approval. Many lenders approve in 24–48 hours and fund within days.

Predictable repayment. You know your payoff date and total cost. Budgeting is simpler.

Simpler structure. One lump sum, one term, one monthly payment. No draws, no phases, no rate resets.

No home equity needed. Your credit profile matters more than your home value.

Cons

Higher interest rates. Personal loans typically cost more because they’re unsecured.

Smaller loan amounts. Most cap out at $50,000–$100,000; HELOCs often offer more.

Fixed loan amount. You can’t borrow more without reapplying and going through underwriting again.

No flexibility. Once funded, you have a fixed repayment schedule. No “borrow as you go.”

Interest cost over time. Over a 5–7 year term, interest adds up. Total repayment is often higher than HELOC interest on the same principal.

Credit impact. The lender does a hard credit pull, which temporarily dings your score.

Those are the main trade-offs. A full breakdown of what lenders typically require — from credit scores to income documents — is in our guide on personal loan requirements & eligibility.

HELOC vs Personal Loan: Which Is Better?

There’s no single right answer. Which option wins depends entirely on what you need the money for, how you prefer to borrow, and what kind of risk you’re willing to carry.

Think of it this way: a HELOC makes sense when flexibility and low rates matter more than predictability. A personal loan works better when you want a fixed payment, a clear payoff date, and no collateral at stake.

To figure out which fits your situation, run through this quick checklist:

- Do you own a home with enough equity?

- Do you need ongoing access to funds or just one lump sum?

- Can you handle a variable interest rate that might rise?

- How fast do you need the money?

- Is protecting your home from any risk a top priority?

When a HELOC May Make Sense

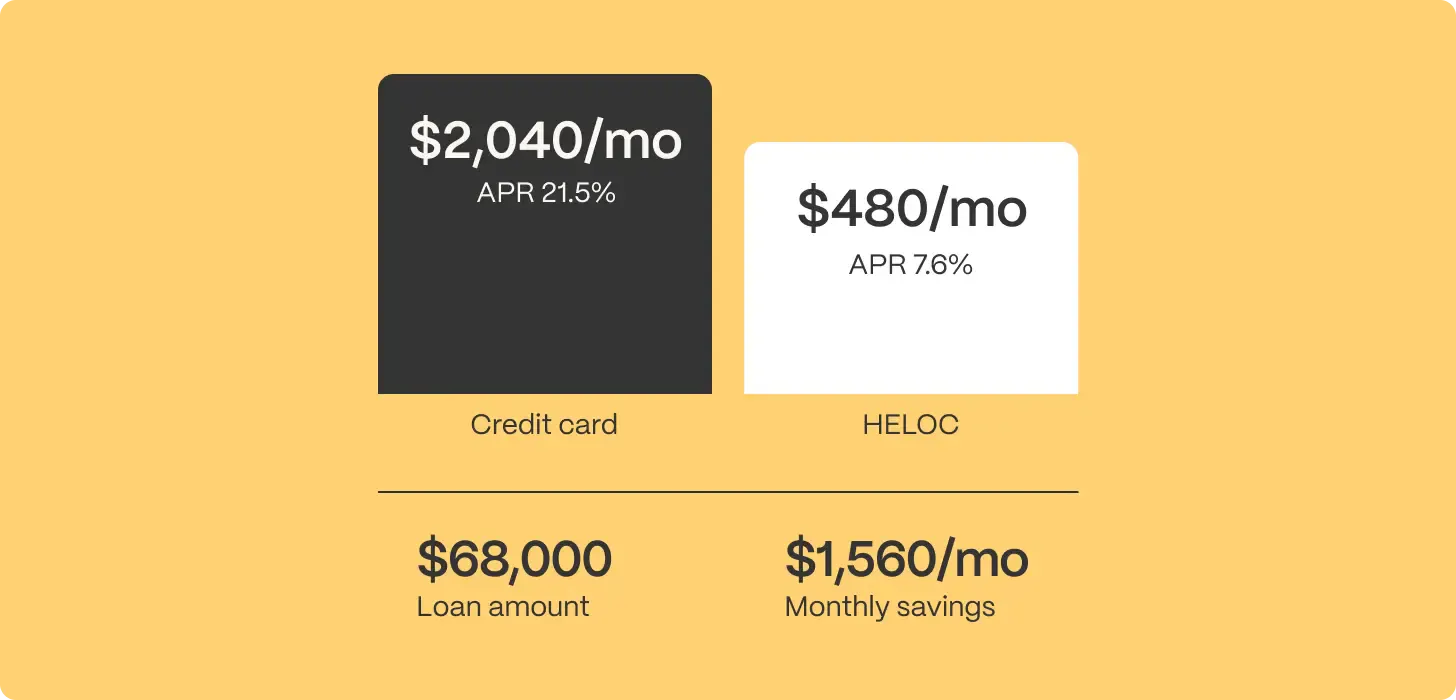

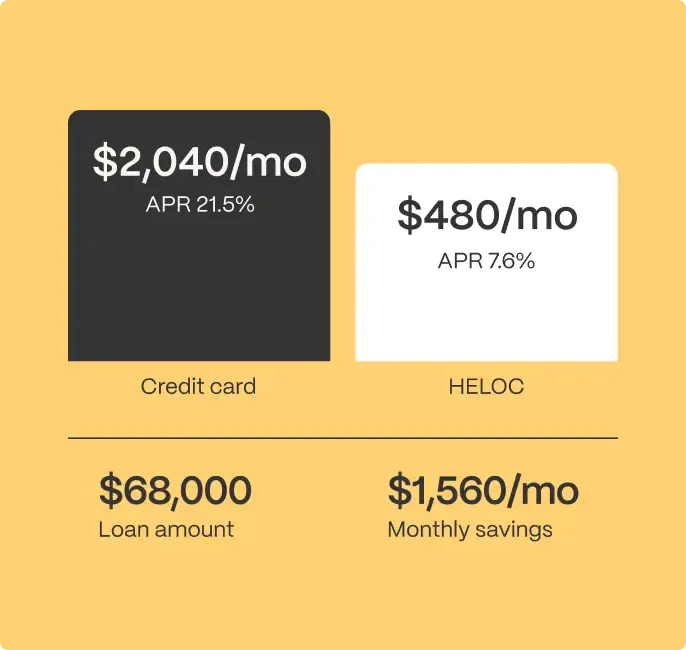

A HELOC fits best when you need money over time, not all at once. Home renovations are the classic example — you pay contractors in stages. The same goes for funding a business with irregular expenses or covering education costs semester by semester. In these situations, borrowing only what you need keeps your interest costs lower than taking a large personal loan upfront.

Take a homeowner with a $300,000 house and $200,000 left on the mortgage. A kitchen and bathroom remodel costs $80,000, but the work stretches over 18 months. Contractors bill in phases. A HELOC lets you draw only what each phase costs and pay interest just on that amount. A personal loan would force you to take the full $80,000 upfront and pay interest on everything from day one — including money sitting idle.

When a Personal Loan May Make Sense

A personal loan works best when you need a fixed amount of money upfront and want predictable payments. Debt consolidation is the most common example — you have multiple credit card balances at high rates, and you want to combine them into one loan with a single monthly payment and a clear payoff date. The same logic applies to covering a large one-time expense like a wedding, medical bill, or major car repair.

Imagine three credit cards totaling $20,000 at APRs between 18% and 22%. A personal loan at 10% APR lets you pay off all three cards at once. If you want to see how this comparison breaks down in more detail, we have a separate piece on debt consolidation vs personal loan.

Now you have one fixed payment over five years, no variable rates, and no risk of running up new debt on the old cards unless you choose to. A HELOC would offer a lower rate but with variable payments and your home on the line — not ideal if your main goal is simplicity and discipline.

Not all personal loans are the same. Our guide on types of personal loans walks through the main variations — secured, unsecured, fixed-rate, and more.

Other Options to Consider

HELOCs and personal loans aren’t the only ways to borrow. Depending on your situation, one of these alternatives might work better — or at least buy you time.

Two other paths worth a quick look are credit cards and a handful of additional financing tools. Neither is right for every situation, but both have their place.

Credit Cards

For smaller amounts — say $10,000 or less — a credit card with a 0% APR promotional period can be a cheap way to borrow if you pay off the balance before the promo ends. The risk is carrying the balance past the deadline, at which point rates often spike. Not ideal for long-term borrowing, but useful for short-term cash flow. If a personal loan still feels like the right fit, knowing which lenders consistently get good reviews helps. We cover that in our guide on best personal loans.

Other Financing Tools

Home equity loans (second mortgages) give you a lump sum with a fixed rate — a middle ground between a HELOC and a personal loan if you have equity but want predictability. Peer-to-peer lending platforms sometimes offer competitive rates, though fees vary widely. And borrowing from a 401(k) is an option for some, but it carries serious risks if you leave your job before repaying.

If a personal loan still feels like the right fit, knowing which lenders consistently get good reviews helps. We cover that in our guide on best personal loans.

Choosing between a credit card and a personal loan? Our comparison of personal loans and credit cards walks through the trade-offs.

Risks and Considerations

Every borrowing option comes with trade-offs. What looks like an advantage on paper can turn into a problem if your situation changes. Here are the main ones to weigh carefully.

- Risk of collateral (HELOC-specific). Your home backs a HELOC. That’s why rates are lower. But it also means you can lose your house if you stop paying. During the 2008 crisis, thousands of homeowners with HELOCs faced foreclosure — often because of job loss or falling home values. If you choose a HELOC, have a realistic repayment plan and a buffer for setbacks.

- Cost of Borrowing. A lower rate doesn’t always mean you pay less overall. A HELOC’s variable rate could climb, while a personal loan’s fixed rate stays the same. Also consider the term: a personal loan typically runs 2–7 years. A HELOC’s repayment period can stretch 10–20 years. Paying interest over two decades adds up, even at a lower rate. Compare total interest paid.

- Long-Term Commitments. Borrowing always ties up future income. A personal loan has a fixed end date. A HELOC’s draw period can last 5–10 years, followed by 10–20 years of repayment. That’s a long time to carry debt. Before signing, ask yourself whether you’re comfortable having this payment in your budget five or ten years from now.

Where Pennie Financial Fits

Pennie Financial doesn’t lend directly. Instead, it connects you with multiple lending options through a single application — including personal loans and HELOCs. You submit one form, see offers from different lenders, and compare them based on your needs.

That matters because different lenders and products have different requirements and terms. What one lender declines, another may approve. What one prices at 18% APR, another might offer at 12%.

You can explore your options on the personal loans page. For a closer look at how the matching process works, visit how Pennie works.

Final Thoughts

A HELOC and a personal loan are fundamentally different tools. A HELOC offers flexibility, lower rates, and larger sums but puts your home at risk and carries rate uncertainty. A personal loan offers simplicity, speed, rate certainty, and home protection but costs more and caps borrowing capacity

The “better” choice is the one that matches your situation. If you have equity, can tolerate rate swings, and prefer ongoing flexibility, a HELOC may work. If you want a quick, predictable, fixed-cost solution without risking collateral, a personal loan may be the answer.

Take time to understand the tradeoffs. Run the numbers. Consider your risk tolerance. Then choose the option that lets you borrow responsibly and repay with confidence.

Frequently Asked Questions

What's the main difference between a HELOC and a personal loan?

A HELOC is a secured, revolving line of credit tied to your home’s equity. A personal loan is an unsecured, fixed-amount installment loan. The HELOC offers flexibility and lower rates but variable payments and foreclosure risk. A personal loan offers predictability and no collateral risk but at a higher rate.

Is a HELOC safer than a personal loan?

It depends on your definition of “safe.” A HELOC’s lower rate sounds safer, but it comes with foreclosure risk. A personal loan has no collateral risk but higher interest costs. Neither is universally “safer”—it’s a tradeoff between rate risk and collateral risk.

Can you use a HELOC like a personal loan?

You can draw a lump sum and leave it in your account. But HELOCs are designed for revolving access, not one-time borrowing. If you only need one lump sum and won’t borrow again, a personal loan is a better fit. A HELOC leaves flexibility unused and requires a longer approval timeline.

Is it easier to qualify for a HELOC or personal loan?

If you lack home equity or don't own a home, personal loans are easier. HELOCs require home ownership and sufficient equity. With strong credit and home equity, a HELOC is usually easier. With weaker credit or no home, a personal loan is your path.

Do HELOCs have lower interest rates than personal loans?

Typically, yes—often 1–3% lower. But HELOC rates are variable, so the advantage isn’t guaranteed. If rates rise, the gap narrows or disappears. Compare the rates available to you, not just product averages.

When should you avoid a HELOC?

Avoid a HELOC if: (1) you can't stomach a 2–3% rate increase, (2) you lack home equity, (3) you struggle with credit card debt (revolving credit tempts over-borrowing), or (4) the foreclosure risk keeps you up at night. A personal loan may be a better fit.

Can you switch from a HELOC to a personal loan?

Yes. Pay off the HELOC with personal loan proceeds. This makes sense if rates spike and you want to lock in a fixed payment, or you prefer non-collateral borrowing. Weigh the cost of a new application against the benefit of lower ongoing payments.

Get loan offers in as little as 60 seconds

You deserve options. So we built an industry leading platform to compete for your business.

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years

Your info is never sold