Find the help you need for any problem

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

Conditional Loan Approval: What It Means and What Happens Next

Conditional loan approval sounds like a done deal, but it’s not the final step. Many borrowers get confused at this stage — they think they’re ready to sign, but the lender still needs a few more things. A conditional approval means the lender has reviewed your application and is prepared to fund the loan, provided you satisfy a specific set of conditions before closing.

Those conditions might include extra documentation, identity verification, employment confirmation, or something else. Until you clear every item on that list, the loan isn’t fully approved, and no money changes hands. This article covers what conditional approval means, which conditions pop up most often, and how to push your loan to funding quickly — without extra delays or surprises.

In this article:

- What is conditional loan approval?

- How conditional approval works (step-by-step)

- Common conditions lenders may require

- Does conditional approval guarantee a loan?

- What happens after conditional approval?

- How long does final approval take after conditional approval?

- Can you get denied after conditional approval?

- Tips to move from conditional to final approval faster

- Where Pennie Financial fits

- Frequently Asked Questions

What does conditional loan approval mean?

After you submit a formal loan application, the lender runs a hard credit check and reviews your finances. If everything looks solid, they give you conditional approval. Your credit score drives most of the underwriting decision. Our article on what a credit score is and how it works breaks down how the number is built and what moves it.

That means they’re ready to fund the loan — but only after you hand over a few missing pieces of information. This type of approval sits between a simple prequalification and a final yes.

Think of conditional approval as a “yes, once you complete the remaining steps.” You’ve passed the main underwriting review. Now the lender just needs to verify specific items, like proof of income or identity. Until you satisfy every condition, the loan hasn’t closed, and no money moves. Conditional approval is stronger than prequalification but still short of final approval.

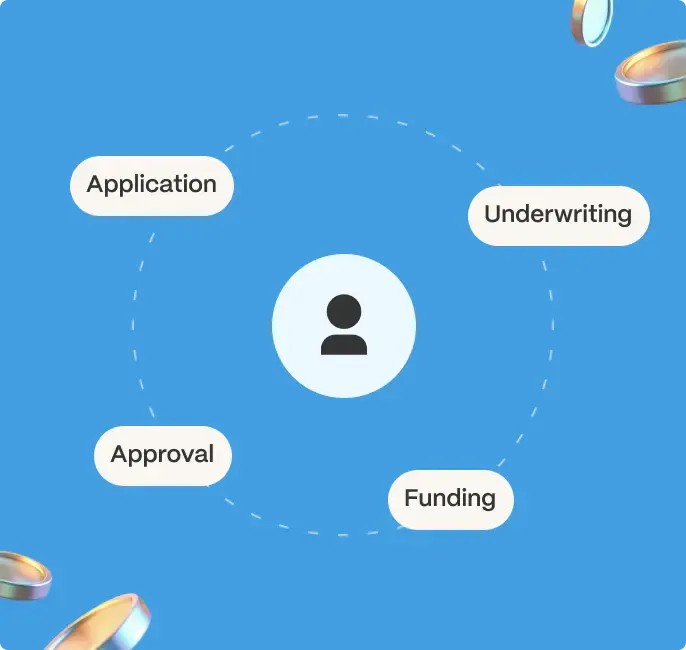

How conditional approval works (step-by-step)

A hard credit check and a full financial review happen right after you hit submit. If your profile passes their initial tests, the lender responds with conditional approval. Here’s how the rest of the process unfolds:

1. Submit a formal application.

You provide all the required information — income, employment, loan amount, and purpose. The lender runs a hard credit check at this stage.

2. Underwriting review.

The lender evaluates your credit, income, debt, and overall financial profile against their loan criteria.

3. Conditional approval issued.

The lender sends a list of outstanding items they need before they can approve the loan.

4. Satisfy the conditions.

You provide the requested documents — pay stubs, bank statements, ID, proof of address, or other items.

5. Final approval and closing.

The lender confirms all conditions are met. You sign the loan agreement.

6. Funding.

Money is sent to your bank account or directly to creditors.

If you want a broader look at the full lending journey, our guide on how long it takes to get a personal loan maps the complete timeline from application to funding.

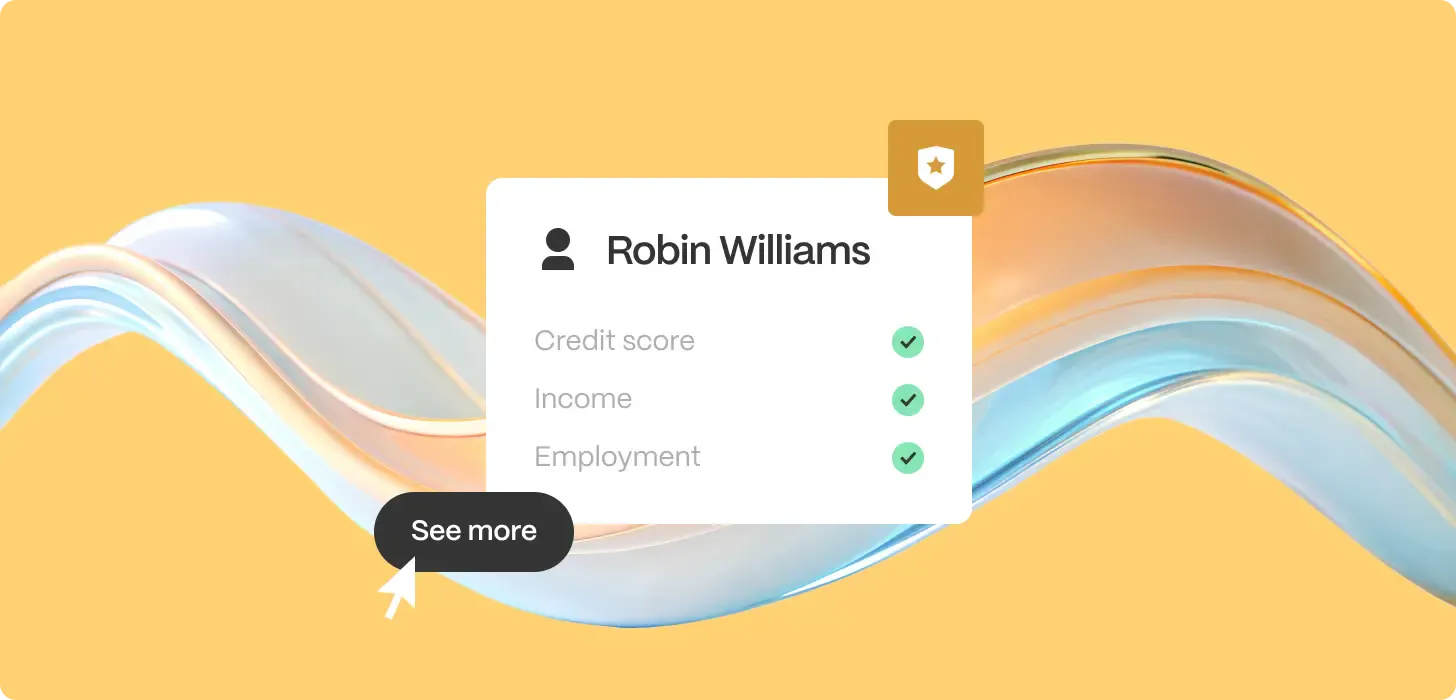

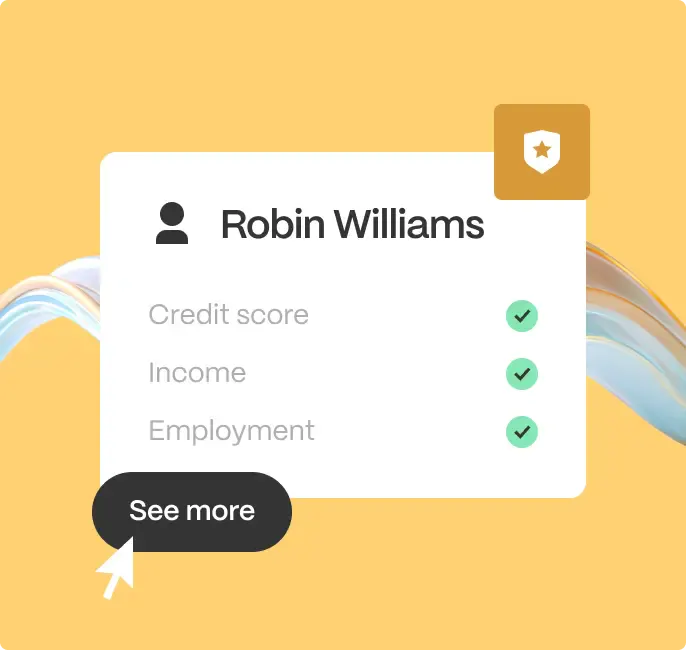

Common conditions lenders may require

Before giving final approval, lenders ask for a few standard items. You’ll typically need to provide:

- Proof of income: recent pay stubs, W‑2s, or tax returns. Self‑employed borrowers often need two years of tax returns.

- Bank statements: usually one to three months of statements to verify your cash flow and account activity.

- Identity verification: a government‑issued photo ID, like a driver’s license or passport.

- Employment confirmation: the lender may call your employer or accept a signed verification of employment form.

- Debt explanations: a short written note about anything unusual on your credit report, such as a large one‑time balance or a past late payment.

- Appraisal (for secured loans): if you’re using a car or home as collateral, the lender needs a current valuation of the asset.

Wondering whether your score is high enough for the loan you want? Our guide on what credit score you need for a personal loan lists the typical thresholds lenders expect.

| Stage | What it means | Impact on your credit |

|---|---|---|

| Prequalification | Early estimate based on basic information | Soft inquiry; no score effect |

| Preapproval | Stronger estimate; some lender commitment | Usually soft, sometimes hard |

| Conditional approval | Loan approved pending conditions | Hard inquiry already done |

Does conditional approval guarantee a loan?

Conditional approval is a positive step, but it doesn’t guarantee you’ll get the loan. The lender still needs you to clear a specific list of items before they fund the money.

Deals fall through for several reasons. Missing or incomplete documents are the most common. Changes in your credit profile also matter — taking on new debt or missing a payment can reverse the approval.

Income problems are another risk. If your pay stubs or tax returns don’t match your application, the lender may withdraw the offer.

What happens after conditional approval?

After you receive conditional approval, the ball is in your court. Let’s walk through what comes next:

- Submit the requested documents. Provide every item on the lender’s list — pay stubs, bank statements, ID, or other verification. Missing a single document can delay the process.

- Underwriting review. The lender checks the documents you sent. If everything matches your application, they move to the final step. If something doesn’t line up, they may ask for clarification or additional paperwork.

- Final decision. Once all conditions are satisfied, the lender issues final approval. At this point, the loan is officially approved.

- Loan closing and funding. You sign the final loan agreement. The lender sends the money to your bank account or directly to your creditors.

How long does final approval take after conditional approval?

The timeline from conditional to final approval varies. In the best case, you’ll have an answer in one to three days. That happens when the requested documents are simple, and you submit them immediately.

Complex cases take longer. Verifying self‑employment income or reviewing an appraisal can stretch the process to one or two weeks. Slow responses or incomplete documents add even more time. The full range usually falls between a few days and two weeks, depending on your situation and how quickly you act.

Not sure where your credit stands right now? Our article on how to check your credit score explains how to pull your report without hurting your score.

Can you get denied after conditional approval?

Conditional approval feels reassuring, but it’s not a lock. The lender still needs to confirm a few final items before funding. If something changes or you miss a deadline, the answer can shift from yes to no. Several factors can turn a conditional approval into a denial.

Job loss

Lenders want to see steady employment. If you lose your job or switch to a lower‑paying position between conditional approval and closing, your ability to repay looks different. The lender can revoke the approval based on the change in income.

New debt

Taking on a new loan, maxing out a credit card, or financing a large purchase changes your debt‑to‑income ratio. Even one new account can push your ratio above the lender’s limit. The lender may deny final approval if they re‑check your credit before closing.

Missing documentation

Conditional approval comes with a list of required items. Fail to provide a single pay stub, bank statement, or verification form, and the lender can close your file. Incomplete or late responses are among the most common reasons approvals fall through.

Appraisal issues

For secured loans, the asset’s value matters. If an appraisal comes in lower than expected, you may no longer qualify for the requested loan amount. The lender can deny the loan or offer a smaller amount based on the reduced value.

Worried that past credit issues could cause a denial? Our guide on how to improve your credit score offers steps you can take before you apply.

Tips to move from conditional to final approval faster

Once you have conditional approval, small actions can speed up the final step. Here’s what helps most:

- Respond quickly: send the requested documents the same day. Every day you wait adds a day to the timeline.

- Avoid new credit applications: don’t apply for any other loan, credit card, or financing until your loan closes.

- Keep finances stable: stay at the same job, avoid large purchases, and don’t move money between accounts without explanation.

- Submit complete documents: double‑check that you’ve included every page the lender asked for. Missing items cause back‑and‑forth delays.

If you want to understand what lenders check before they even issue conditional approval, our article on how to get approved for a loan walks through the full underwriting process.

Where Pennie Financial Fits

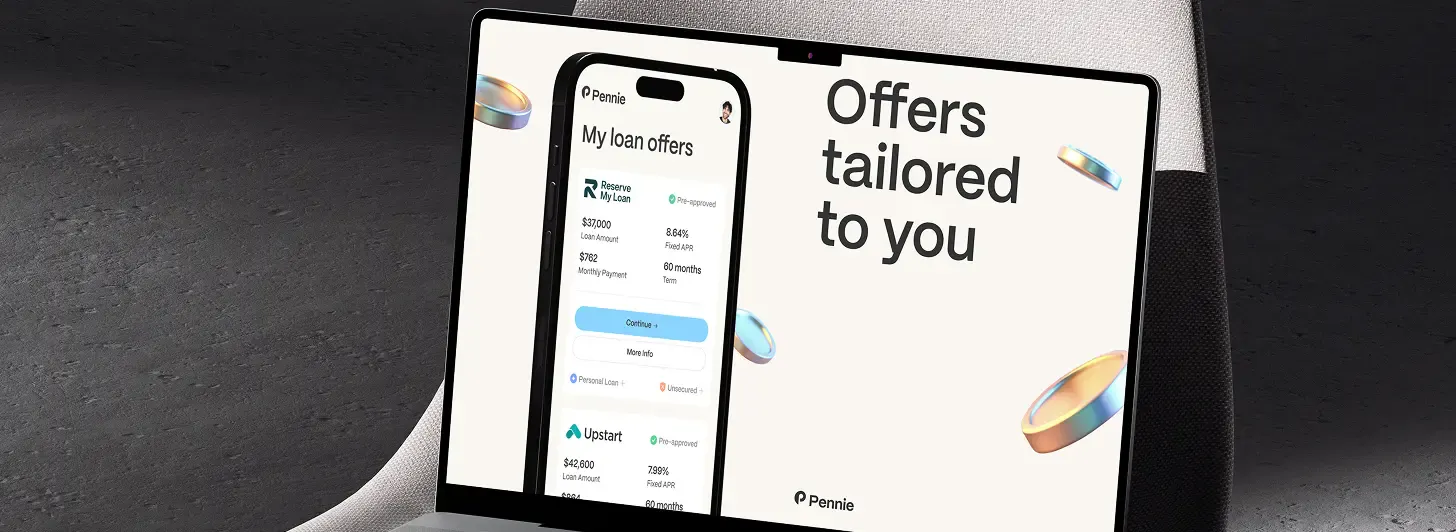

Pennie Financial helps you see your options before you commit to a loan. You fill out one form, and the platform runs a soft credit check to show you prequalified offers from multiple lenders. Your credit score stays unchanged while you compare APRs, monthly payments, and terms.

For a breakdown of the matching process, see how Pennie works. Details on personal loans are also available. Once you pick a lender, the formal application and hard inquiry happen with that lender directly.

Pennie does not guarantee approval — that decision always belongs to the lender.

Ready to start comparing actual offers? Our roundup of the best personal loans gives you a solid shortlist to work from.

Frequently Asked Questions

What does conditional loan approval mean?

It means the lender is prepared to fund your loan once you satisfy specific conditions — typically verification of income, employment, identity, or other application details.

How long does it take to go from conditional approval to funded?

When conditions are straightforward and you respond quickly, the move from conditional approval to funded loan often happens within 24 to 48 hours.

Can a conditional approval be reversed?

Yes. If verification surfaces something inconsistent with the original application — income lower than stated, employment can’t be confirmed, new debt appears, etc. — the conditional approval can be withdrawn.

Is conditional approval the same as preapproval?

No. Preapproval is usually an earlier-stage indication based on a soft inquiry and limited information.

What should I do if I get conditional approval?

Read the condition list carefully, gather all requested documents, upload them through the lender's portal, and respond quickly to any verification requests.

How long does conditional approval last?

Time windows vary by lender — many are around 30 days, but some are shorter.

Why did my lender give conditional approval instead of final approval?

Conditional approval is standard in most lending processes — it gives the lender time to verify specific items before committing funds.

Get loan offers in as little as 60 seconds

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years