Ready to see what's available for your profile? Learn how Pennie Financial works and compare real loan offers across multiple lenders — based on your income and financial profile, not just your credit score.

Find the help you need for any problem

Topics

Debt basics

- Debt basics

- Personal loans

- Rates, fees & APR

- Credit score & eligibility

- Repayment & loan payments

- Loan application

- Debt consolidation

- All articles

Ready to move forward?Get started

How Pennie Financial Differs From Other Loan & Debt Solutions

Personal loans, debt consolidation services, and online lending platforms all look similar at first glance — they all involve borrowing money or managing debt. But how they work, who they're built for, and what they actually do for borrowers vary significantly. Understanding the differences matters when you're trying to figure out which type of financial service fits your situation.

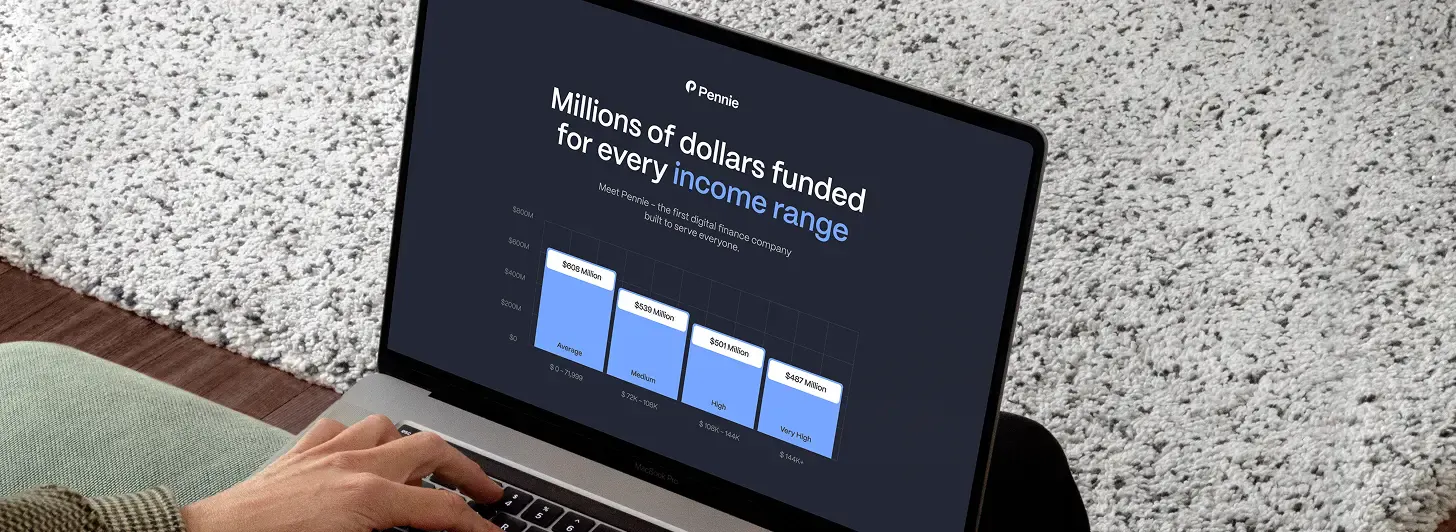

Pennie Financial is a personal loan marketplace that connects borrowers with one of the broader lending partner networks in the personal loan space. Its network includes lenders who prioritize income, employment history, and debt load as primary approval factors alongside credit score. This approach gives borrowers more flexibility and a fairer evaluation.

In this article:

- What Is Pennie Financial?

- How Pennie Financial Works

- Key Differences vs Traditional Lenders

- Pennie Financial vs Other Lending Marketplaces

- Pennie Financial vs Traditional Personal Loans

- Pennie Financial vs Debt Consolidation Services

- Who Pennie Financial May Be a Good Fit For

- Final Thoughts

What Is Pennie Financial?

Pennie Financial is a personal loan marketplace and performance marketing platform focused on connecting borrowers with lending partners whose underwriting models are suited to their financial profile. Unlike a bank or direct lender, Pennie Financial doesn't originate loans itself. It connects borrowers to a network of lenders and evaluates fit based on the borrower's full financial picture.

Part of what distinguishes Pennie Financial is the breadth of its lending partner network. Among those partners are lenders who assess verified income, employment history, and debt-to-income ratio as primary or co-primary factors.

The typical Pennie Financial borrower is someone with a real borrowing need, documented income, and a credit profile that may not meet the threshold of a traditional bank but does reflect genuine repayment capacity. Learn more on this page.

How Pennie Financial Works

The process is built around a single application that routes to multiple lenders simultaneously, rather than requiring separate applications to multiple institutions. This streamlined approach ensures that borrowers provide their information once, while gaining access to multiple lending options.

Application

Borrowers submit one application with their financial information: income, employment, debt obligations, and the loan amount they're seeking. That information goes to Pennie Financial's lending network rather than a single institution.

Income Evaluation

Among the lenders in the network are those who assess income patterns, employment stability, and DTI as primary or co-primary factors alongside credit. Verified, stable income carries real weight with these lenders. A borrower with a 600 credit score and $70,000 in annual income has a meaningfully different risk profile than the credit score alone suggests.

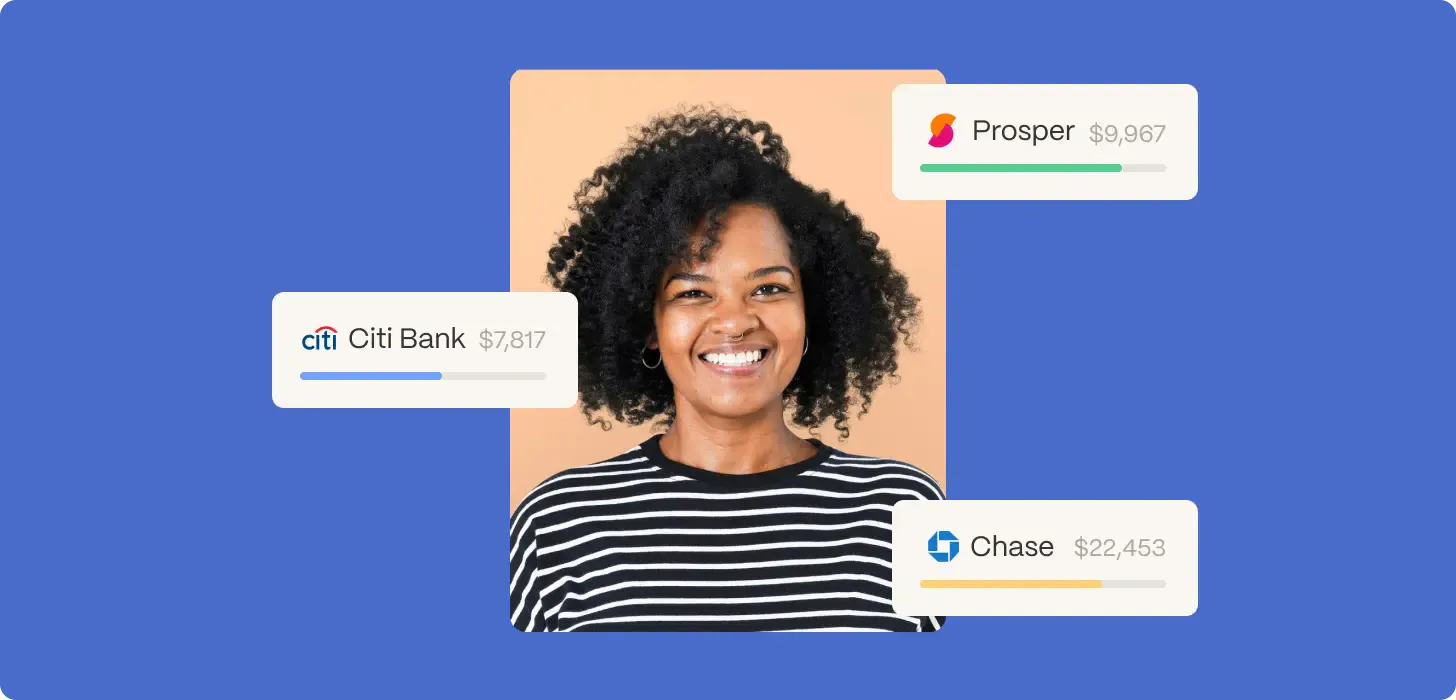

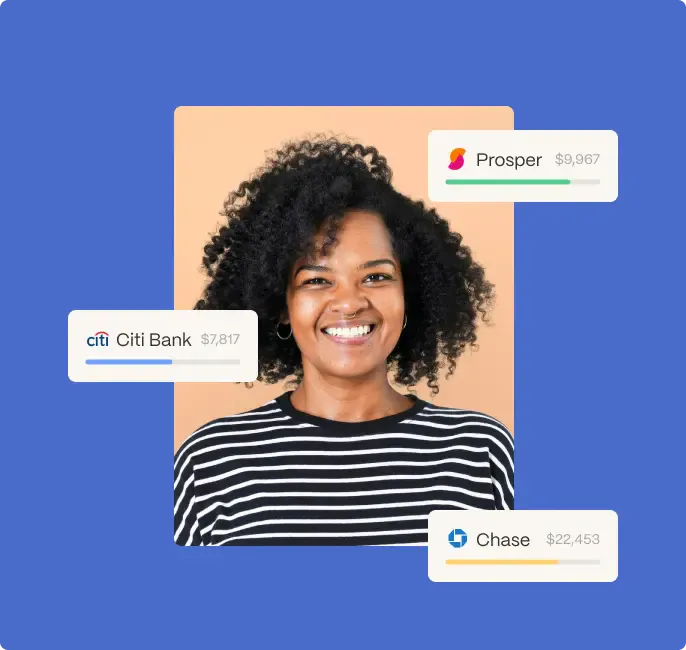

Multiple Offers

Rather than a single yes/no from one lender, borrowers see offers from across the network — different rates, terms, and structures. They can compare before committing. See how the process works in detail before applying.

Repayment Structure

Loans originated through Pennie Financial's lending partners are standard personal loans — fixed monthly payments over a defined term. You borrow a fixed amount and repay it in full with interest.

Key Differences vs Traditional Lenders

Understanding how Pennie Financial differs from traditional banks and direct lenders can help borrowers see why the marketplace approach offers distinct advantages.

Here's a quick comparison:

| Factor | Traditional Bank / Direct Lender | Pennie Financial |

|---|---|---|

| Application process | One application, one lender, one decision | One application, multiple lenders, multiple offers |

| Primary approval factor | Credit score (usually threshold-based) | Income + DTI weighted alongside credit |

| Borrower profile | Optimized for prime/near-prime credit | Broader network — includes income-focused lenders accessible to fair credit borrowers |

| Rate comparison | Single offer; no built-in comparison | Multiple offers visible before committing |

| Credit pull on comparison | Hard pull per application | Soft pull for prequalification |

| Transparency | Varies by institution | APR, fees, and total cost disclosed before decision |

| Speed | 3–7 business days (banks); 1–3 days (online) | 1–2 business days typical |

Pennie Financial vs Other Lending Marketplaces

Not all lending marketplaces work the same way. Most borrowers assume a marketplace is a neutral comparison tool. The reality of how some platforms operate is quite different, and it's worth understanding before you fill out any form.

How Many Marketplace Models Actually Work

On a significant number of lending marketplace platforms, submitting your information is the trigger. Before you've seen a single rate, your contact information has already been shared. The inbound calls start quickly. Some borrowers describe filling out what felt like a rate comparison form and finding themselves fielding calls from several lenders within minutes.

How Pennie Financial's Approach Differs

Pennie Financial is built around the borrower seeing offers first and deciding whether to proceed. The process is designed so the borrower controls the pace. You understand what's available for your profile before any commitment is made. That's a meaningfully different experience from models where submitting a form begins an outbound contact sequence you didn't necessarily anticipate.

Why This Matters for Borrowers With Imperfect Credit

Borrowers who are already navigating financial stress don't benefit from being contacted by multiple parties simultaneously before they've had time to evaluate their options. A borrower with imperfect credit working through their choices deserves the same deliberate comparison experience that a prime borrower gets.

What to Look for When Evaluating Any Marketplace

Before submitting your information to any lending platform, it's worth understanding whether you'll see offers before being contacted, or whether form submission triggers immediate outreach. Prequalification with a soft credit pull is the standard Pennie Financial applies.

Pennie Financial vs Traditional Personal Loans

A personal loan from a bank or direct online lender and a personal loan originated through Pennie Financial's lending network are structurally the same product: fixed amount, fixed payments, fixed term, full repayment of principal plus interest. The difference is in who's evaluating you and how.

Credit Score Role

Traditional lenders — particularly banks and large national institutions — have defined minimum credit score thresholds. Applications that fall below them don't proceed. Lenders in Pennie Financial's network use credit data as one input among several, with income and employment history factoring in more heavily for borrowers in the fair or poor credit range.

Typical Approval Requirements

Standard personal loan approval at a traditional bank generally requires a credit score of 660 or higher, a DTI below 40%, and verifiable income. Lending partners in the Pennie Financial network span a broader range — some work with scores as low as 550–580 if the income profile supports the loan.

Repayment Expectations

Personal loans through any channel require full repayment of the borrowed amount plus interest. There's no reduction in principal, no program-based adjustment to repayment, and no forgiveness component.

When a Traditional Personal Loan May Be a Better Option

If you have excellent credit (720+) and existing relationships with a bank or credit union, going direct may produce the best rate — particularly if the institution offers loyalty pricing or rate discounts for automatic payment. Pennie Financial's advantage is largest for borrowers who need to compare across lenders. Personal loan options determine what's realistically available for your financial profile.

Pennie Financial vs Debt Consolidation Services

The term "debt consolidation" covers two distinct things, and understanding the difference helps clarify where Pennie Financial fits.

Debt Consolidation as a Loan

Taking out a personal loan to pay off multiple existing debts — combining them into one payment at one rate. This is Pennie Financial's core use case. You borrow a fixed amount, use it to pay off existing balances, and repay the new loan over a defined term. The debt structure simplifies.

Debt Consolidation Services

Such services, sometimes called debt relief or debt management companies, are a different category. These are programs that negotiate with creditors on behalf of borrowers, potentially settling debts for less than the full balance owed, in exchange for program enrollment fees (typically 15–25% of enrolled debt). Pennie Financial's primary focus is connecting borrowers with personal loans, including guidance on consolidation loan options.

Here's a side-by-side look at how a Pennie Financial personal loan compares with traditional debt consolidation services:

| Personal Loan (via Pennie Financial) | Debt Consolidation Service | |

|---|---|---|

| What you repay | Full amount borrowed + interest | Potentially reduced balance (not guaranteed) |

| Credit impact | Minimal if payments are on time | Significant negative impact during the process |

| Program fees | Standard loan origination fee | 15–25% of enrolled debt |

| Structure | Fixed loan — borrow, repay, done | Negotiation-based — outcome not guaranteed |

| Best for | Borrowers who can sustain full repayment | Severe hardship; full repayment not realistic |

When borrowers meet the requirements for a personal loan, using a lending marketplace to combine high-interest debts often costs less than enrolling in a fee-based program and provides a repayment process. Understanding how personal loans affect your credit score is a useful context before making that decision.

Who Pennie Financial May Be a Good Fit For

Pennie Financial isn't one-size-fits-all — different borrowers benefit in different ways depending on their income, credit profile, and debt situation. The following categories highlight who may find the platform especially useful:

Borrowers With Variable or Non-Traditional Income

Freelancers, contractors, gig workers, and self-employed borrowers often get a harder look from traditional lenders whose systems are calibrated to W-2 income. Lenders in Pennie Financial's network that evaluate income patterns over a trailing period are more equipped to accurately assess these borrowers' repayment capacity.

People Who Don't Meet Traditional Lending Criteria But Have Strong Income

A credit score of 600 reflects credit history — it doesn't automatically reflect current financial stability. Borrowers who have had past credit challenges but are now employed, earning consistently, and maintaining low debt loads represent a different risk profile than their score might suggest to a score-first lender.

Borrowers Who Want to Compare Before Committing

The marketplace model is valuable regardless of credit profile — seeing multiple offers before accepting terms is simply better than accepting the first offer available. The cost differences across lenders for the same borrower profile can be substantial, and a soft-pull prequalification process lets borrowers see those differences.

Those Consolidating Multiple High-Rate Debts Into a Single Payment

Borrowers carrying multiple credit card balances or high-rate personal loan obligations who want to simplify to one payment and potentially reduce their blended interest rate. Consolidation loan options show what's realistically available for each borrower's situation.

Final Thoughts

Pennie Financial is a personal loan marketplace that connects borrowers with a broad network of lenders. Many of these lenders consider income and employment history alongside credit score, making loans accessible to those who might not qualify through traditional channels. The platform shows multiple rates and offers through a single application. Whether the goal is consolidating high-rate debt, covering a large expense, or accessing working capital.

Share

Ready to move forward?Get started

Get loan offers in as little as 60 seconds

You deserve options. So we built an industry leading platform to compete for your business.

Loans up to $250,000

APR starting at 5.99%

Repayment terms up to 10 years

Your info is never sold